“Cut short your losses… and let your profits run.”

-David Ricardo

Ricardo didn’t run a quant fund (or a CTA), but he certainly inspired many. He was one of the popular 18th century British economists that professors call “classical.” One of his most important teachings was Trend Following.

In his chapter titled “Managed Futures”, Lasse Heje Pedersen cites the aforementioned Ricardo quote and links it to “traders who are most directly focused on trend-following” (managed futures hedge funds and commodity trading advisors, or CTAs). “Such funds have existed at least since Richard Donchian started his fund in 1949, and they have proliferated since the 1970s.” (Efficiently Inefficient, pg 208)

“Time series momentum is a simple trend-following strategy that goes long on a market that has experienced a positive excess return over a certain look-back horizon and goes short otherwise. We consider 1-month, 3-month, and 12-month look-backs…” And I’m calling this out this morning as it’s one of the main factors whipping people around these days in macro markets.

Back to the Global Macro Grind…

It’s as obvious that CTAs are popular in commodity bull markets as it is that modern day quant funds chasing price momentum kill it on the way up. The thing about chasing price (or charts that “look good”) is that the look-back periods keep getting shorter.

Why are the look-back periods getting shorter?

- We have an oversupply of money managers trying to beat the same performance bogeys at the same time

- We have massive short-term performance pressures (weekly, monthly, and quarterly) due to lack of performance

- We have machines that simply make all of this happen faster and faster

Those are some very basic reasons for short-term performance (and chart) chasing. There are, of course, many more. But my point here is that A) this is part of playing today’s game and B) there have been massive intermediate-term risks associated with it.

Note that I wrote intermediate-term risks. In other words, there are huge TREND and TAIL duration risks associated with immediate-term (TRADE) trend-following! And that’s really the point – 1, 2, and 4 week chart chasing aren’t TRENDs – they’re TRADEs.

If you use our multi-duration and multi-factor macro model, you’ll recall the big buckets of duration we use are:

- TRADE = 3 weeks or less

- TREND = 3 months or more

- TAIL = 3 years or less

That’s why all of our Macro Themes live in the 3 month to 3 year space. Getting the big stuff (Macro TRENDs and TAIL risks) right over longer-term time horizons (vs. where our industry’s performance anxieties reside) has really helped put Hedgeye on the map.

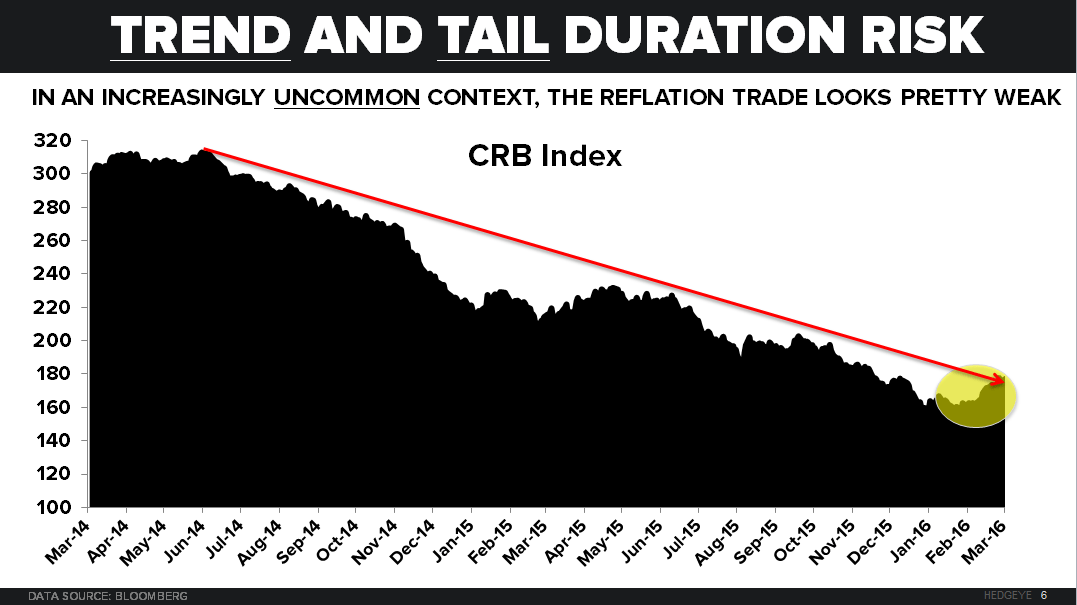

Let’s review an example of something Trump might call you-ge! in Macro for the last 3 years – being The Bear in Commodities:

- CRB Commodities Index (19 commodities) was between 300 and 310 in both Q1 of 2013 and 2014

- After multiple chart chases, the CRB Index got cut in HALF by the low we just saw in Q1 of 2016

- At 155 on February 11th, 2016, the CRB Index hit a 3yr low

Then it “bounced”, for a month… and we’re back in a commodity bull market? #Cool.

Set aside the super-short-term performance pressures of some of your peers and think long and hard about A) what’s happened in the 3-month to 3-year time series vs. B) the 40yr USD Devaluation (Fed) Cycle and C) the last 3-4 weeks:

- CRB Index “bounced” +14% from that FEB low to 177 with the US Dollar Index -3%

- USD Index +0.5% yesterday = Down Day of -2.2% for CRB Index

- CRB Index TAIL risk (resistance) = 201; US Dollar Long-term TAIL support = 92.11

Just to answer the super-short-term question first… where do you think the Commodity “Bull” and/or reflation trade will be if the US Dollar Index ramps another +3% from here? (hint: the 2wk inverse correlation between USD and CRB is -0.96!)

How about the intermediate-term TREND questions?

- What if the Fed raises and/or signals a June rate hike at the April meeting?

- What happened 3 months ago when the Fed tightened (in Dollars) into a US slowdown?

- If the industrial/cyclical/commodity economy really is “back”, why doesn’t the Fed hike 5x this year?

It’s a good thing most people who are invested with fund managers have no idea how all of this works. Can you imagine if the average American actually understood why the Fed is constantly being pressured to reflate assets by devaluing the purchasing power of their hard earned US Dollars? Or are they smarter than the average perma asset inflation bull and getting angry? #Trump

Not only is it crystal clear that both the Industrial #Recession isn’t over but that important #LateCycle components of the US economy are no longer accelerating. Despite fantastic weather on the East Coast in FEB, New Home Sales dropped -6.1% year-over-year. We now have a trifecta for the former Housing Bulls (turned Bears) @Hedgeye – Pending, Existing, and New Homes – all DOWN year-over-year in rate of change terms!

Ah, you get it now. If the US equity bulls were straight up with you about it, what they really need to keep the “reflation” rally going (for more than a month off its 3yr low) is the TREND of a slowing US economy (maybe a #Recession?) and more Fed easing (Dollar Down).

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 1.84-1.97%

SPX 1

RUT 1056-1110

VIX 13.11-20.28

USD 94.68-97.17

Oil (WTI) 36.38-42.97

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer