Editor's Note: Below is a brief excerpt and chart from today's Early Look written by Hedgeye U.S. Macro analyst Christian Drake. Click here to learn more.

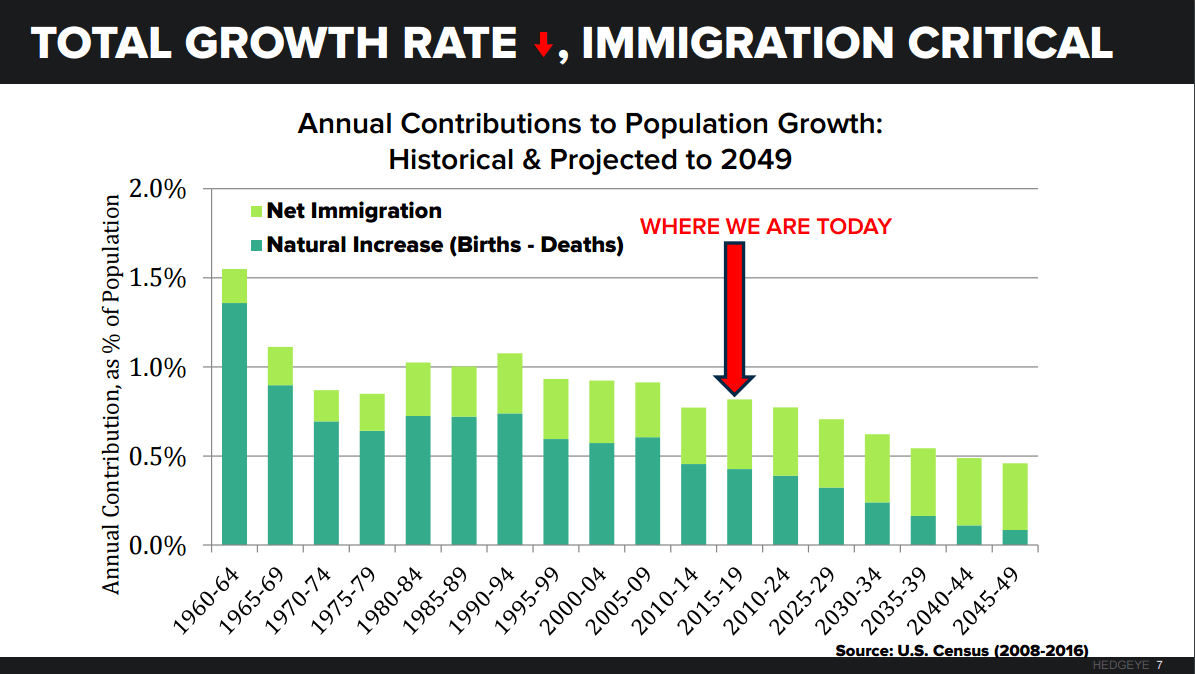

"... Big Picture | Fertility & Immigration: Fertility rates in both North and South America (a key driver of domestic immigration trends) are falling with significant consequences for domestic population growth. As the Chart of the Day below illustrates, Natural population growth is expected to trend toward 0% over the next 30 years with net immigration becoming an increasingly important growth driver. Declining fertility rates across Mexico and key source countries in Central/South American broadly suggest the past will not be prologue for the long-term forward trend in immigration."