This Nike quarter was fairly predictable. EPS was spot on with our model, and the company’s guidance was consistantly bullish. The top line miss, however, is not something any 30x multiple stock can afford. We actually thought the weakness would come on the futures line, but that metric remains bullet proof for now. Keep in mind that historically, futures orders almost never roll over a quarter in advance of shipping product for the Olympics. Importantly, the evolution – and acceleration – of the company’s Direct-to-Consumer model served as a punch in the jaw to bulls of the traditional athletic brick & mortar model. We outline these points below – seemingly ignoring some of the astounding call outs we’re seeing in Nike’s Global model. But this one is a game-changer if there ever was one. We’re actually taking up our Gross Margin estimate to 52% by May20 – mind you that is leagues above what this company has ever tested before (on an apples-to-apples accounting basis to peers, this is closer to 58%). Our resulting EPS number is $4.73, which is nearly 30% above the consensus. Again, that’s huge for a company with the dominance, size, scale, cap and stability of Nike. What’s that worth? We hate picking multiples out of the air – so we won’t. Let’s simply use a 1.0 PEG, which is below what it’s trading at today. That’s a 25x p/e, a $120 stock – or $90 in 12-18 months. Nike remains one of our top picks.

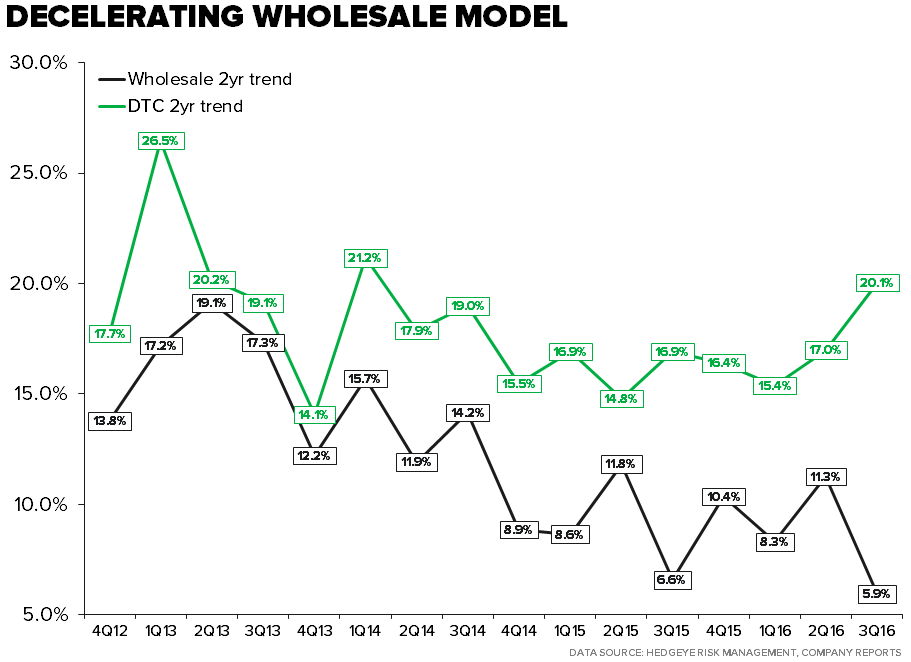

1) Lower Lows at Wholesale, Higher Highs for DTC. NKE NA biz grew 13% during the quarter. The incremental $429mm in revenue was essential evenly split between wholesale and retail, with DTC growing 25% fueled by e-comm and wholesale up 9% against the easiest comp in the past 5 years (3% wholesale growth in 3Q15). If we look at it on a 2yr basis, eliminating all of the quarterly noise, we’ve seen a meaningful bifurcation in the underlying growth trend – not over the past three quarters, but past three years. If we hold the 2yr growth rate constant into 4Q16 we’re looking at negative growth for NA wholesale at -2%. A far cry from the 12% average we’ve seen over the past 20 quarters. But, that came at a time when Nike was taking its penetration inside its key wholesale partners to all-time highs – Nike sales inside of Foot Locker went from 60%-80% over that time period.

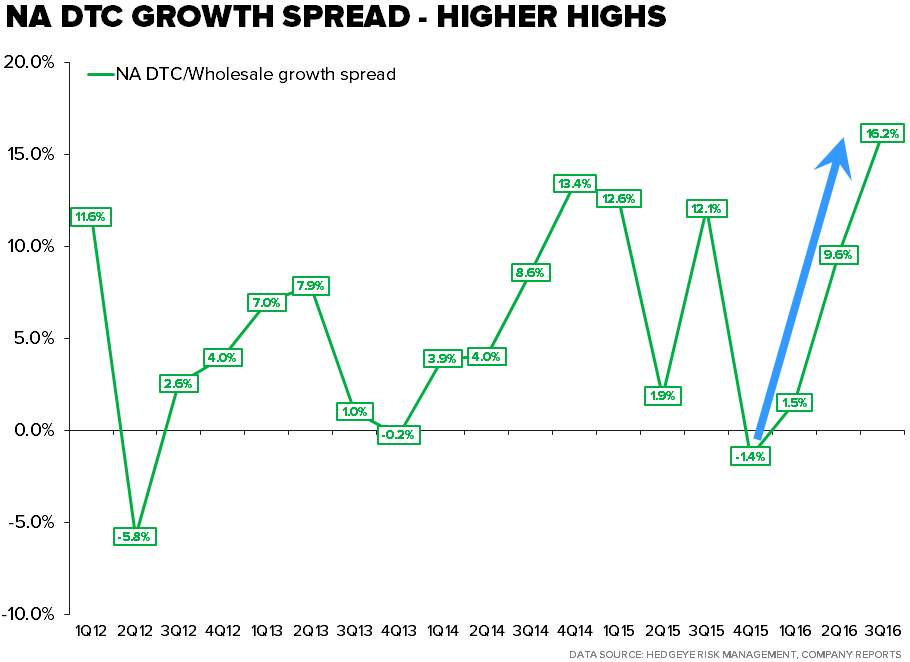

2) Channel Growth Spread at New Peak. The growth spread (calculated by taking DTC growth minus Wholesale growth) accelerated to 16% in the quarter Nike reported last night. The chart itself paints a pretty clear picture on how Nike is turning the distribution paradigm on its head, but what we think is most important to point out is that we are seeing higher highs in the DTC growth rates as the business approaches $4bn in sales. Over the course of the next five years we expect Nike to blow away its $7bn e-commerce target with the majority of that growth coming in its home market. That means an incremental $5bn-$6bn in NA e-commerce off a base of ~$750mm today. That translates to a continued widening in the growth spread over the near and long term.

3) DTC Penetration is Accelerating – Off a Higher Base. DTC Penetration as a % of total sales accelerated meaningfully in the quarter on a TTM basis, up 75bps representing the largest growth rate we’ve ever seen sequentially at Nike NA. To add a little context, over the past five years NKE NA DTC has grown its penetration by 450bps. This one quarter amounted for nearly 20% of that growth. If we look at where Nike direct competes online, its at the top end of the distribution chain. Put another way its at the product level which drives ASP and traffic to the likes of Foot Locker, Finish Line, and Dick’s Sporting Goods. As Nike continues to push its DTC agenda, those dollars come directly from that tier of the market, while the mid-tier channel stays more or less isolated.

HERE IS THE LINK TO OUR (SLIGHTLY DATED, BUT STILL RELEVANT) 85-PAGE NIKE BLACKBOOK - CLICK HERE

Here’s our note from yesterday, specifically outlining some of the reasons why we like NKE long-term.

NKE | CHANGE

Takeaway: NKE might be the best long-term idea we can find, but there are some serious short-term factors that will cause big buying opportunities

Conclusion: We think that Nike is perhaps the best idea in retail as EPS more than doubles to nearly $5/shr, which is huge for a large cap name that is already operating at peak margins. The company should add $10bn in revenue over 4-years from e-commerce alone, which should take gross margins at least 5-points higher, past the 50% mark (a level most never thought achievable). But this transformation will also make its Futures model obsolete, and we think it’s a matter of time before it’s no longer reported to the Street. That won’t happen today. But we’ll inch closer as each quarter passes and earnings surprises on the upside, while the order book goes the other way. That’s going to create some fantastic buying opportunities. Though the Olympics and slightly better FX should help order levels and the company’s outlook, we’d rather wait for a point where there is some critical misunderstanding of the company’s growth and financials to make a ‘step in and buy before the event’ call. That does not exist today.

DETAILS

We like a lot more about Nike than we don’t, and the story is arguably more investable than ever. This company and story have become extremely complex, but the basic building blocks of what we like can be placed in the following buckets

a) Investing at a greater rate than ever in its product engine resulting in an arsenal that even its strongest competitors can’t replicate

b) Changing up the manufacturing paradigm for the first time in 40 years (initially what most of us know as FlyKnit – but this will change soon), which not only creates margin and working capital opportunities, but also gets Nike even closer to market (i.e. it will get 2-3 months out in an industry that is locked into a 5-6 month order window).

c) Dropping its attitude of deference and respect for the traditional footwear retailing channel, and getting the right product into the hands of the right consumers regardless of the poor growth and real estate decisions made by Nike’s traditional wholesale channel over the past 20 years.

Put these together, and we think that you’re looking at an incremental $10bn in sales at a 70% gross margin (vs $31bn in sales at a 47% margin today). When all is said and done, we think that gets you to almost $5 in EPS in four years versus the $1.85 it earned last year. Yes, earnings should more than double in 4-years for a large cap name with stable growth, a bullet proof balance sheet ($3/sh in cash), 75%+ share in some of its core businesses, dominant positioning in a global duopoly, and a structural advantage that could potentially never be overcome (i.e. what Google has over Yahoo). Does it make sense to us that Nike is trading at an all time high price and multiple? Of course it does. But that doesn’t mean it’s expensive – at least for someone that follows our train of thought.

Now, please allow me to talk out of the risk management side of my mouth. This name might look ridiculously expensive for a person with a very short (TRADE) duration, who is only looking in the rear-view. They’ll see peak margins, a peak 30x multiple, and a futures growth rate (THE key stock driver) that has been running at a double digit rate for the past 10 quarters with a risk to reversion to a longer-term mean of 7-9%. Tack on short interest that is running at just 1.1% of the float (basically nonexistent), and the simplest roll in futures could send this name tumbling.

Two considerations

- The first is that the Olympics this summer will definitely boost Nike’s order book. Now…if the futures rate STILL rolls over despite the Olympics, then Houston has a problem. Unlikely. But a strong consideration.

- Second is that if we’re right, which we obviously think we are, then we’re going to see more than half of growth come from DTC channels – as we saw last quarter when Nike proved to be its own biggest growth engine for the first time in history. But think about it…If we see a $50 wholesale order that used to show up on the order book (futures) all of a sudden turn into a $100 fully consolidated sale through Nike DTC (online, retail), then we’ll have sales, margins and earnings going higher, but futures going lower. This is critical, as when this trend hits critical mass, we’re likely to see Nike start to consistently beat earnings and cash flow, but miss on an increasingly arbitrary statistic known as Futures.

The question then is when will PWC recommend to Nike that they stop reporting futures altogether. We think that is a near mathematical certainty. But, will Nike do so during a quarter when they are crushing it on every metric – including futures? Or will it happen in response to an otherwise ugly futures number that is the result of the wholesalers (like FL) tapping out on their ability to order more product because that part of the business is in a decline? Nike always talks about playing offense. Let’s see if they do it right this time. We’re not worried about a change happening with tonight’s print. But a change should definitely be in the works.

Until then, this is a name for long term investors to buy on red as futures numbers revert.