Investors bullish on U.S. housing are setting themselves up for disappointment.

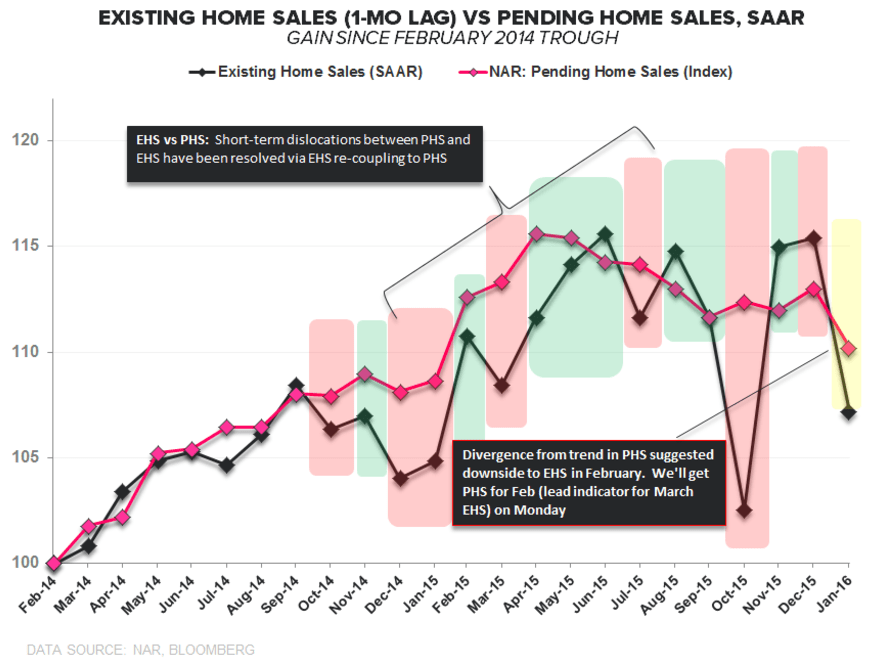

"Existing Home Sales were down -7.1% sequentially and decelerated to +2.2% YoY in February. We’ve known for over a month that February was going to be soft as EHS recoupled to PHS so the print was of little surprise," Hedgeye Housing analysts Josh Steiner and Christian Drake wrote in a recent institutional research note.

Click to enlarge.

Steiner and Drake point out that sales grew +2.2% year over year in February but the extra day in the period provided a +3.5% benefit. Net of the extra leap day, EHS were actually down -1.4% Y/Y.

Even Lawrence Yun (NAR’s chief economist) had a sober assessment: “[The February decline] was meaningful...”

* * *

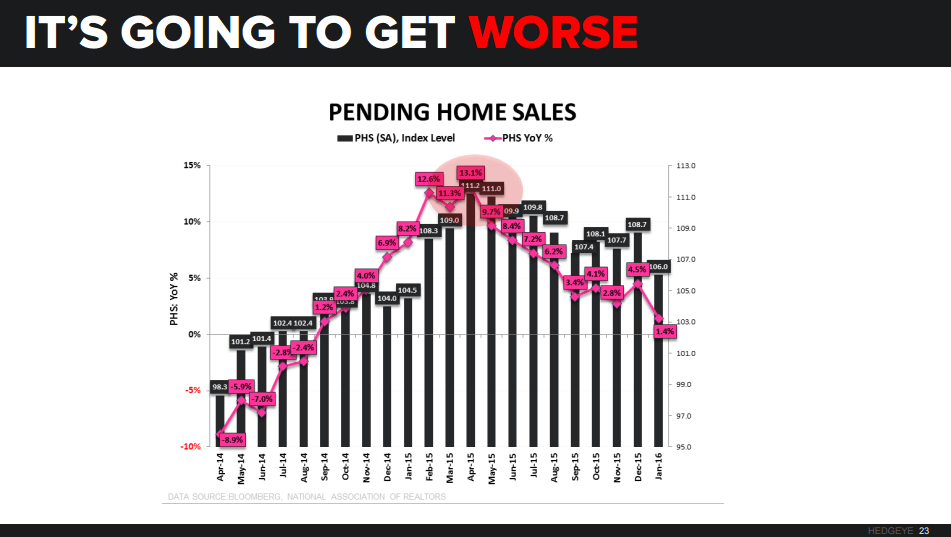

On The Macro Show this morning, Drake added that housing trends don't get easier from here. The Pending Home Sales data is up against some steep comps from last April and May:

Home prices lag the volume of sales so bottom line, with volume declining, Steiner and Drake conclude, "We expect HPI trends to flat-line and begin to roll as we move through 1H16, representing an addition fundamental headwind for housing related equities."

In case you haven't seen it yet, here's our recent 2-minute video explaining, "Why We're Bearish On Housing."

***To access Steiner and Drake's institutional Housing research ping sales@hedgeye.com.