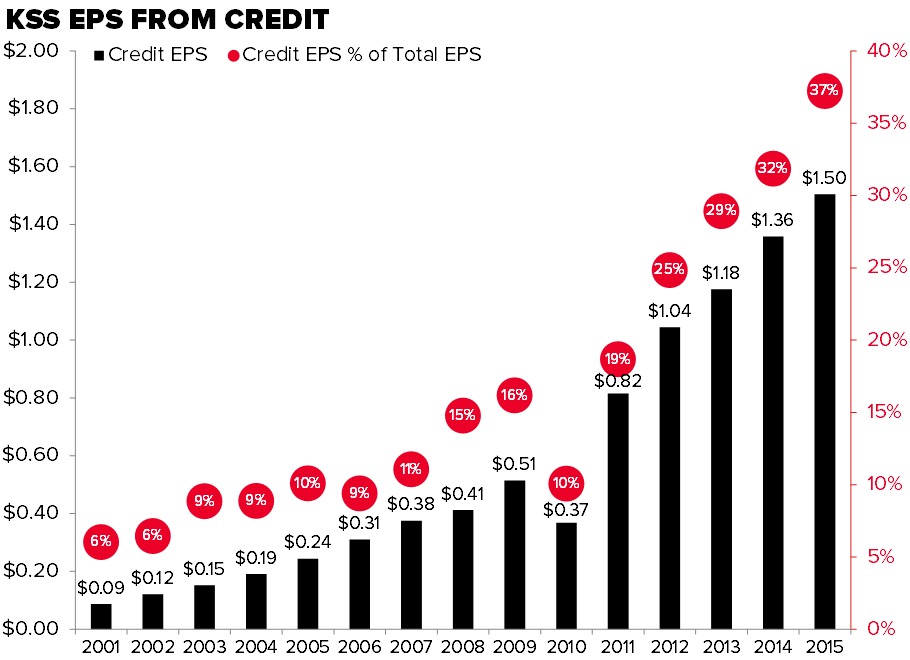

In typical KSS’ fashion, the company released its 10K after the close on a Friday. The biggest item that caught our eye was – you guessed it – credit income. The precise numbers are disclosed once a year, despite the fact that it has grown in to KSS’ single largest profit center. A few points…

1) KSS’ share of income from its partnership with CapitalOne clocked in at $456mm. That’s now 29% of EBIT a level that we think is flat-out unhealthy for a company like KSS at this point in the economic cycle.

2) Consider this…KSS’ EPS was down 5.2% for the year to $4.04 (which includes credit income), but EPS from the operating business was down by 13% -- not good.

3) KSS core business earned $2.54 last year. As a frame of reference, that’s right where earnings came in circa 2008-2009. In other words, right now its earnings are spot-on with where we were in the Great Recession. But…we’re clearly not in such a climate. That begs the question – what if we actually enter a severe downturn (or even a moderate one) again?

4) Note that Macy’s delinquency rate ticked up materially in the fourth quarter. We also see CapitalOne’s charge-off rate ticking steadily higher. We’re not making the call for a collapse in the credit cycle, but it’s pretty irrefutable that it is eroding rather than improving.

We still think that KSS is a 3-Stage Short Call. Stage 1) Starting with the weakness we see today by being such a bad retailer with poor competitive and geographic positioning, then Stage 2) morphing into a story where it jeopardizes its own credit income due to its own cannibalistic rewards program – without a roll in the broader credit cycle, and then Stage 3) a weakening economy having an outsized negative impact on KSS’ consumer, its’ top line, margins, and credit income.