Key Takeaway:

The U.S. market reacted positively to the Federal Reserve's dovish announcement last week, especially with high yield YTM coming in -17 bps to 7.67%. However, more risk measures flashed red than green; European CDS widened by 5 bps week over week, retracing some of the prior week's tightening, the TED spread (an indicator of contagion risk) rose by +2 bps to 33, and the price for Chinese steel dropped by -3.8%.

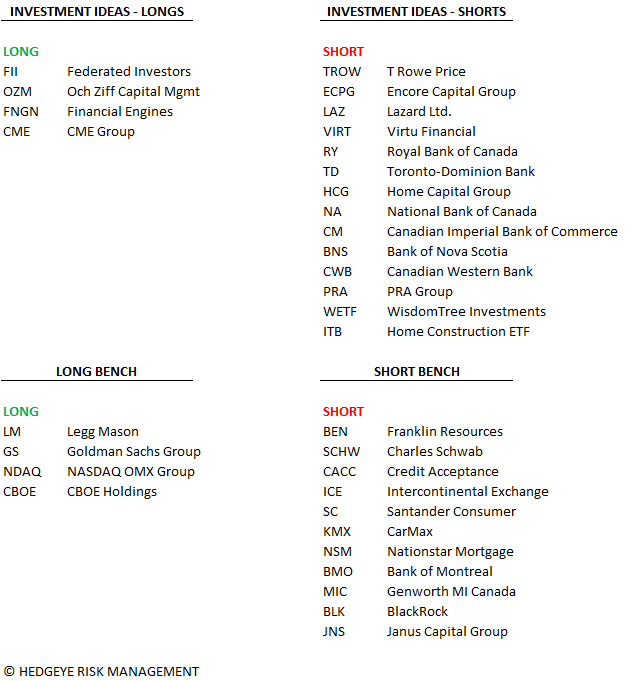

Current Ideas:

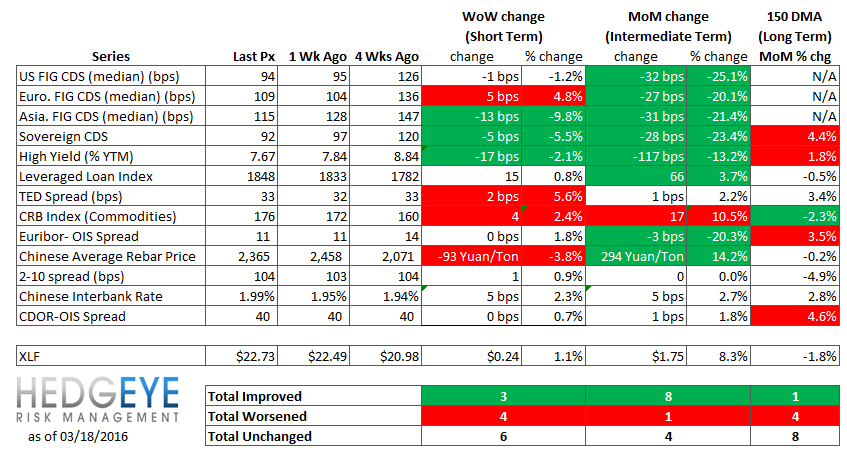

Financial Risk Monitor Summary

• Short-term(WoW): Negative / 3 of 13 improved / 4 out of 13 worsened / 6 of 13 unchanged

• Intermediate-term(WoW): Positive / 8 of 13 improved / 1 out of 13 worsened / 4 of 13 unchanged

• Long-term(WoW): Negative / 1 of 13 improved / 4 out of 13 worsened / 8 of 13 unchanged

1. U.S. Financial CDS – Swaps were mixed among US Financials. The banks specialty lenders saw nominal tightening, while the insurers saw large tightening.

Tightened the most WoW: AIG, LNC, AXP

Widened the most WoW: JPM, WFC, AON

Tightened the most WoW: AIG, LNC, HIG

Widened the most MoM: AGO, RDN, MBI

2. European Financial CDS – Swaps mostly widened across European banks last week. The median spread widened by +5 bps to 109, giving back some of the prior week's 25 bps tightening.

3. Asian Financial CDS – Swaps tightened across Financials in China and Japan last week while Indian bank swaps mostly widened.

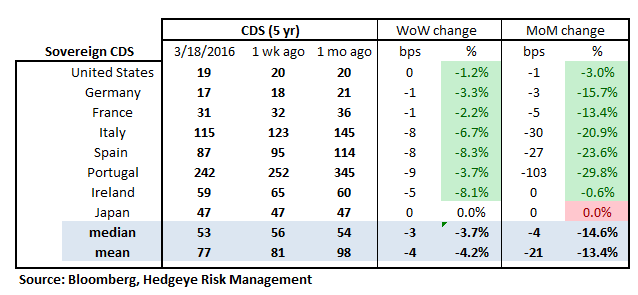

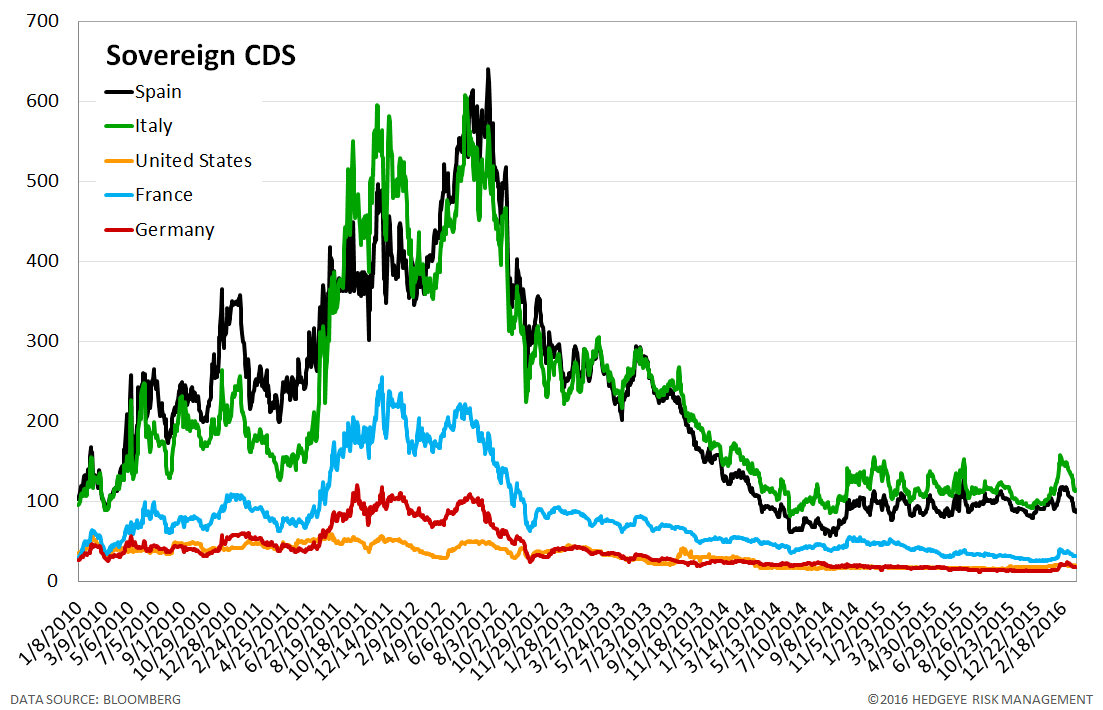

4. Sovereign CDS – Sovereign Swaps mostly tightened over last week. Portuguese sovereign swaps tightened the most, by -9 bps to 242.

5. Emerging Market Sovereign CDS – Emerging markets swaps mostly tightened last week as the dovish Fed announcement allowed for a more positive outlook on EM currencies; a weaker dollar makes it easier for emerging markets to pay back dollar-denominated debt. Brazilian swaps tightened the most, by -25 bps to 366. Meanwhile, on the other end of the spectrum, Indian sovereign swaps widened by 10 bps to 156.

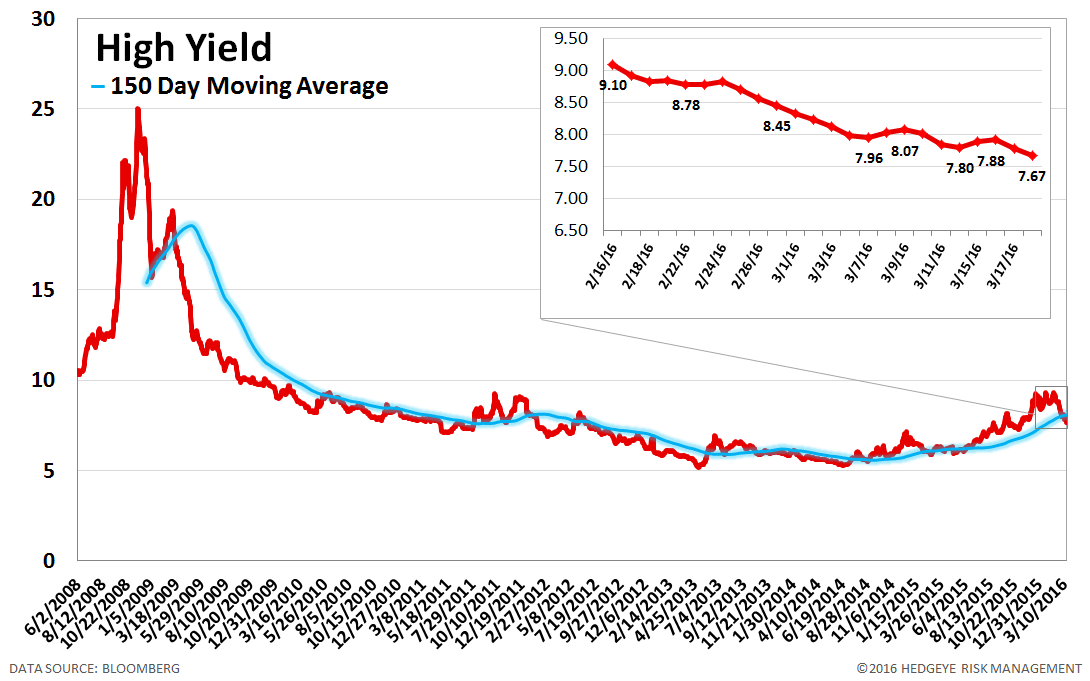

6. High Yield (YTM) Monitor – High Yield rates fell 17 bps last week, ending the week at 7.67% versus 7.84% the prior week.

7. Leveraged Loan Index Monitor – The Leveraged Loan Index rose 15.0 points last week, ending at 1848.

8. TED Spread Monitor – The TED spread rose 2 basis points last week, ending the week at 33 bps this week versus last week’s print of 32 bps.

9. CRB Commodity Price Index – The CRB index rose 2.4%, ending the week at 176 versus 172 the prior week. As compared with the prior month, commodity prices have increased 10.5%. We generally regard changes in commodity prices on the margin as having meaningful consumption implications.

10. Euribor-OIS Spread – The Euribor-OIS spread (the difference between the euro interbank lending rate and overnight indexed swaps) measures bank counterparty risk in the Eurozone. The OIS is analogous to the effective Fed Funds rate in the United States. Banks lending at the OIS do not swap principal, so counterparty risk in the OIS is minimal. By contrast, the Euribor rate is the rate offered for unsecured interbank lending. Thus, the spread between the two isolates counterparty risk. The Euribor-OIS spread was unchanged at 11 bps.

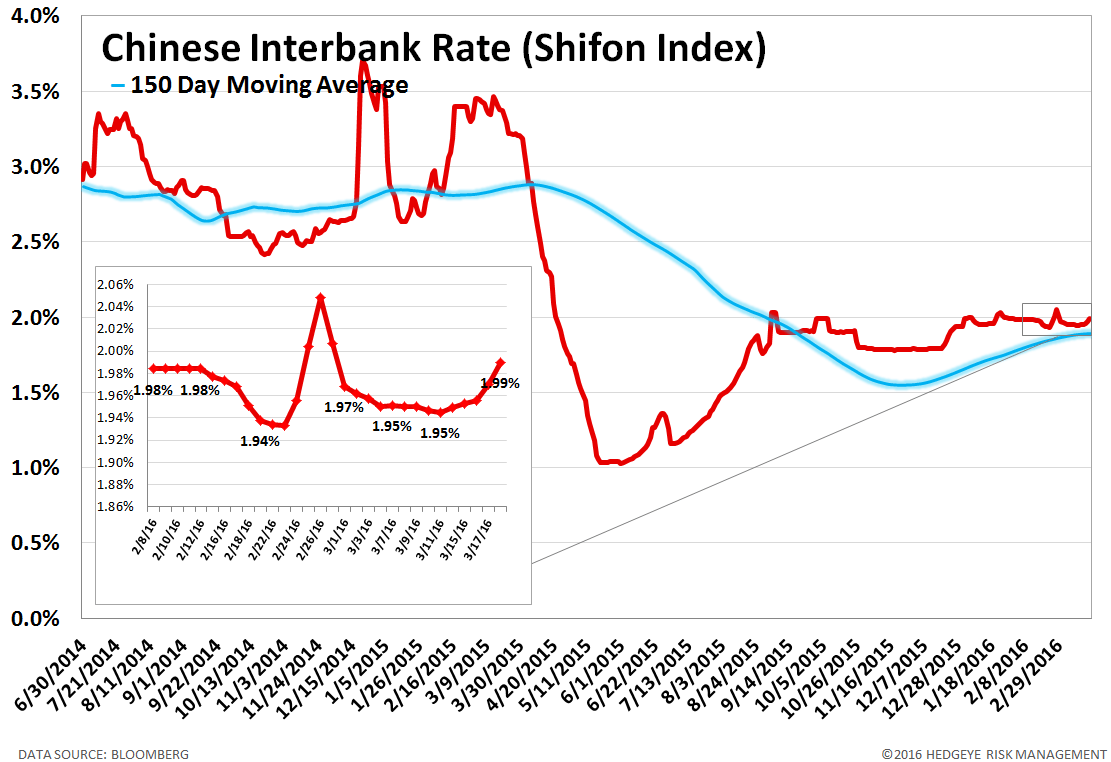

11. Chinese Interbank Rate (Shifon Index) – The Shifon Index rose 4 basis points last week, ending the week at 1.99% versus last week’s print of 1.95%. The Shifon Index measures banks’ overnight lending rates to one another, a gauge of systemic stress in the Chinese banking system.

12. Chinese Steel – Steel prices in China fell 3.8% last week, or 93 yuan/ton, to 2365 yuan/ton. We use Chinese steel rebar prices to gauge Chinese construction activity and, by extension, the health of the Chinese economy.

13. 2-10 Spread – Last week the 2-10 spread widened to 104 bps, 1 bps wider than a week ago. We track the 2-10 spread as an indicator of bank margin pressure.

14. CDOR-OIS Spread – The CDOR-OIS spread is the Canadian equivalent of the Euribor-OIS spread. It is the difference between the Canadian interbank lending rate and overnight indexed swaps, and it measures bank counterparty risk in Canada. The CDOR-OIS spread was unchanged at 40 bps.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT