The S&P 500 might be back to “flat," but being Long the Long Bond, Gold, and Utilities continues to dominate in the absolute return space.

The recent "back to flat" rally is starting to look precarious. Here's analysis from Hedgeye CEO Keith McCullough in a note sent to subscribers this morning:

"While being right on all of my macro longs in 2016 (and having covered SPY in FEB, then coming back to the short side too early here in March SPY short -3.65% against me currently), I’m as committed to the bear side of SPX and Russell as I have been every time VIX has been in this 12-14 range since JUL (when I initially went bearish on SPY)"

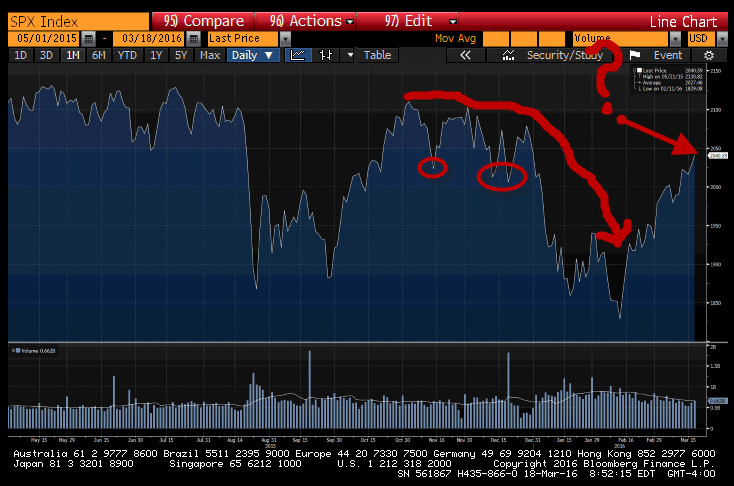

Check out the corresponding chart of the S&P 500.