In short, this morning's claims number appears consistent with YTD trends. In other words, the US Labor market has remained resilient in spite of myriad other signs of slowing. As labor has historically been coincident/lagging we continue to expect to see weakness in the non-services side of the economy bleed through to the economy at large. To date, however, we continue to wait, as we view the setup as still asymmetrically negative.

On the energy side of the house, conditions remain challenging as the basket of 8 energy states we track show an ongoing decoupling from the broader US.

The Data

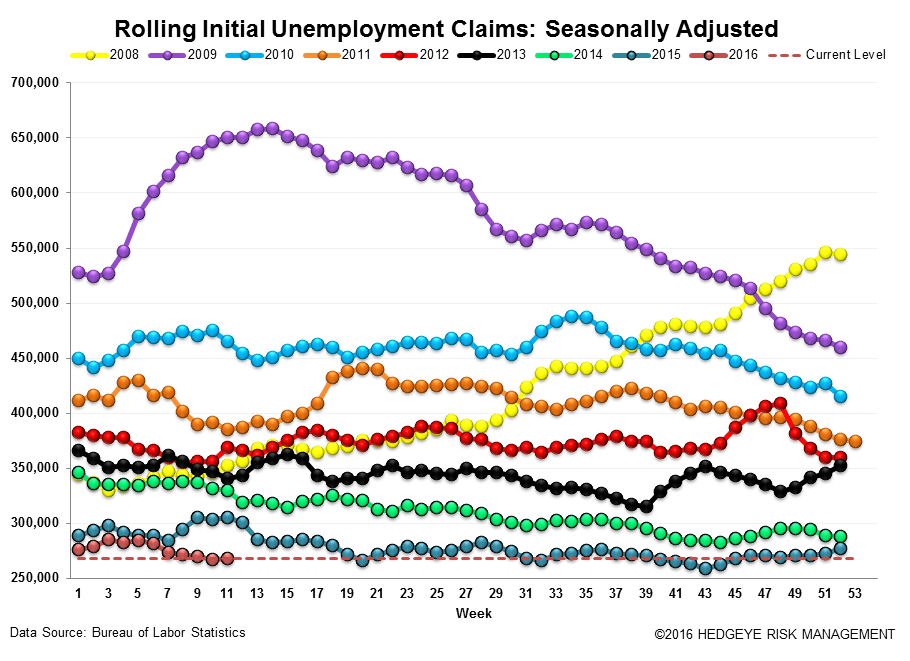

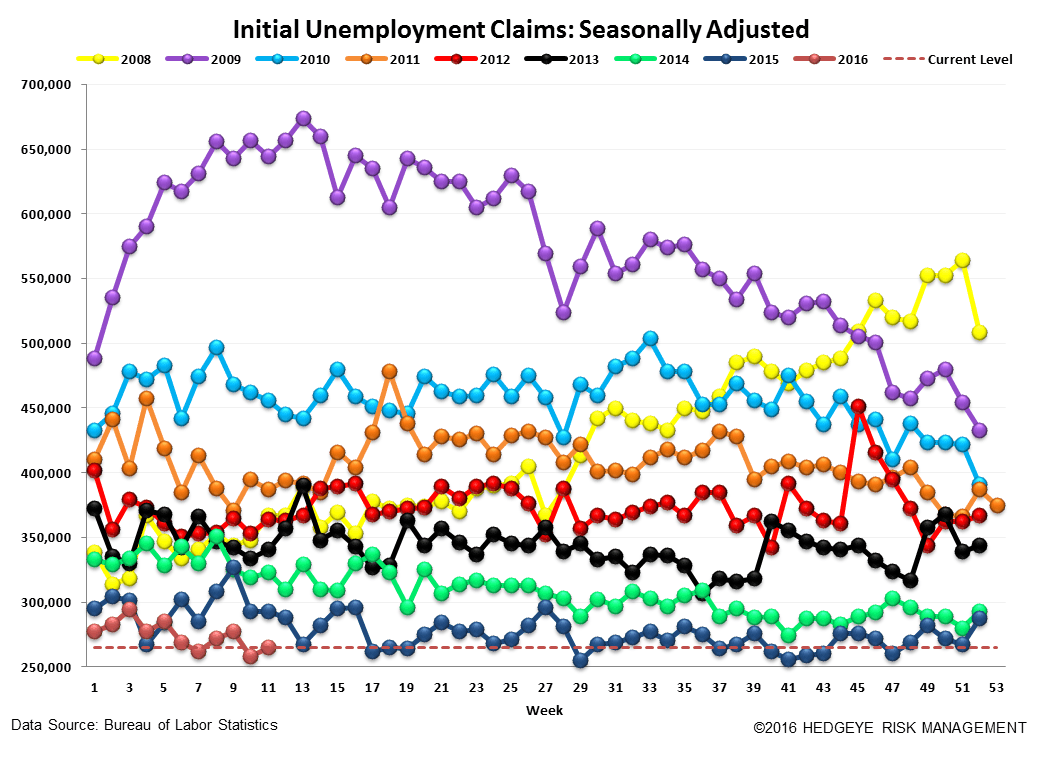

Prior to revision, initial jobless claims rose 6k to 265k from 259k WoW, as the prior week's number was revised down by -1k to 258k.

The headline (unrevised) number shows claims were higher by 7k WoW. Meanwhile, the 4-week rolling average of seasonally-adjusted claims rose 0.75k WoW to 268k.

The 4-week rolling average of NSA claims, another way of evaluating the data, was -11.9% lower YoY, which is a sequential improvement versus the previous week's YoY change of -11.4%

Yield Spreads

The 2-10 spread rose 6 basis points WoW to 105 bps. 1Q16TD, the 2-10 spread is averaging 109 bps, which is lower by -27 bps relative to 4Q15.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT