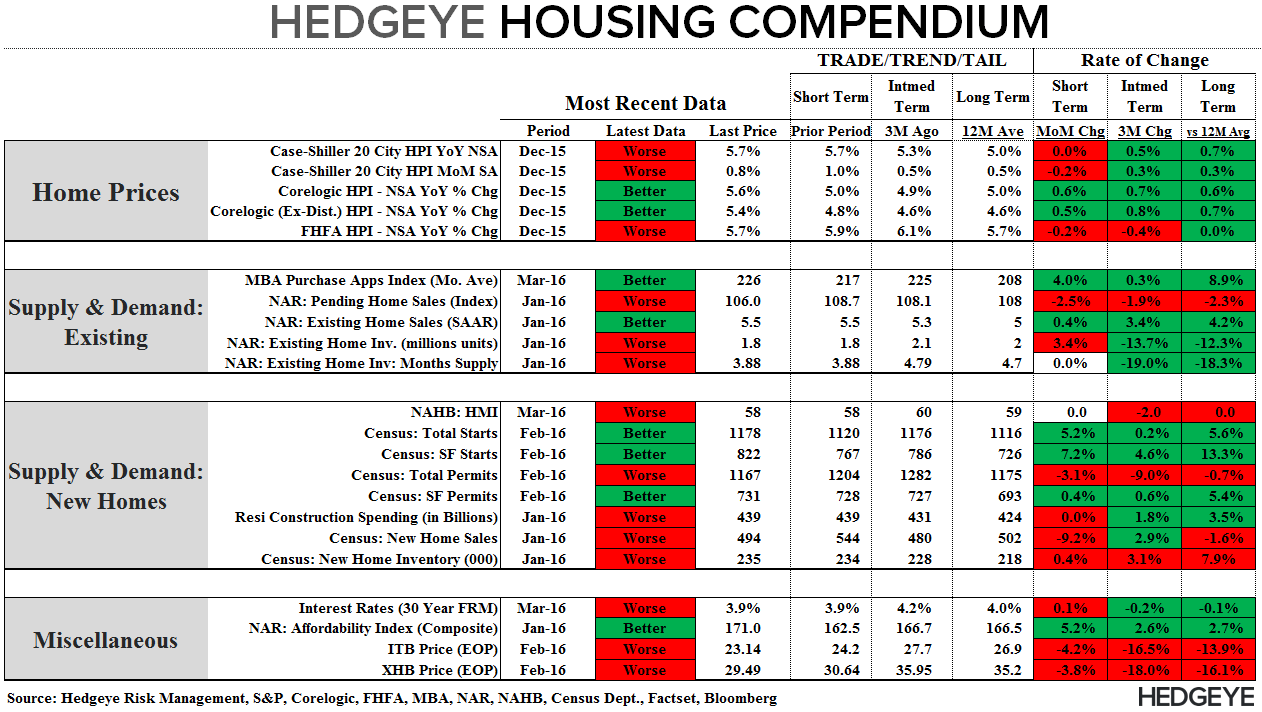

Our Hedgeye Housing Compendium table (below) aspires to present the state of the housing market in a visually-friendly format that takes about 30 seconds to consume.

Today’s Focus: February Housing Starts & Permits

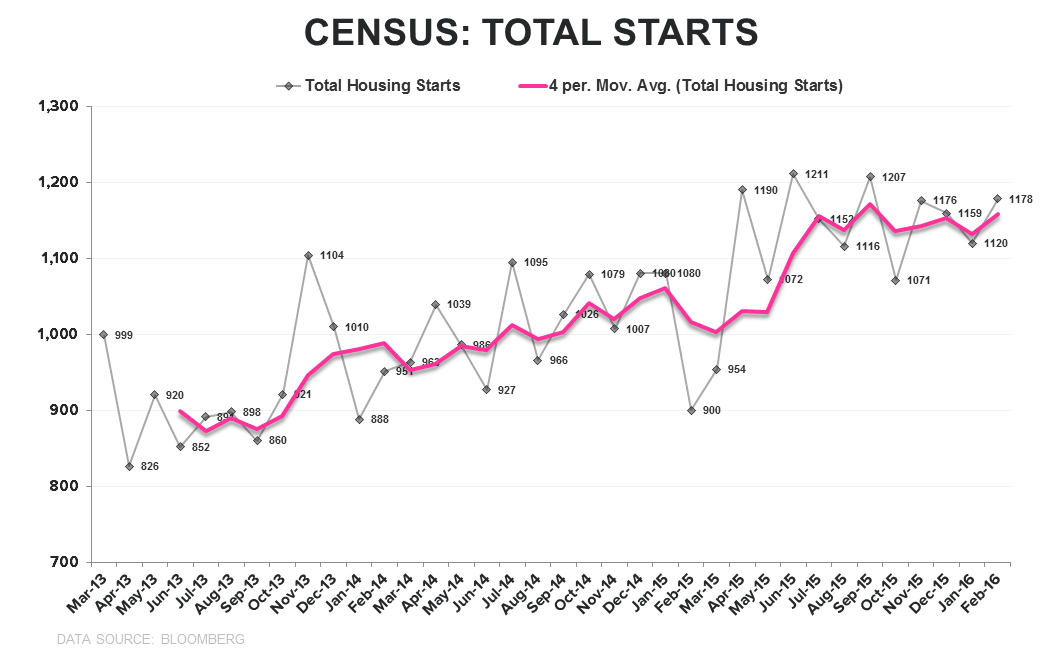

We knew this morning’s Starts data for February was going to be solid; Base effects were exceedingly easy given severe weather last year and seasonals were equally supportive as each of the last two years saw weather depressed Februaries give way to rebound strength in April/May (see 1st chart below). Next month’s March data should benefit from a similar dynamic.

So, we successfully hurdled the easy comp, now what?

The answer carries some duration sensitivity:

- Total Starts | Flat-lining: New construction activity has shown a clear but crawling trend higher since 2010 and the longer-term mean reversion upside to average historical levels of activity remains an opportunity. Inclusive of the sequential improvement in February, however, Total Starts have been flat to down for the last 10-months (see 2nd chart below) and permits, while stable-to-modestly better, aren’t signaling a meaningful acceleration over the nearer-term.

- SF vs MF | Mix Shift: Mix has shifted over the last year as multi-family activity has moderated back towards 2014 levels while SF construction has shown offsetting improvement. Whether funding stress and a higher cost of capital for CRE weighs on multi-family construction remains to be seen. Domestic age and racial demographics will remain supportive of rental demand for the foreseeable future but rental affordability is already stretched and Shelter inflation in this morning’s CPI report made another higher high at +3.28% YoY. A similar pace of rental price inflation could persist further but rental cost burdens are already at historic highs and rent price growth can only run at a steep premium to income growth for so long.

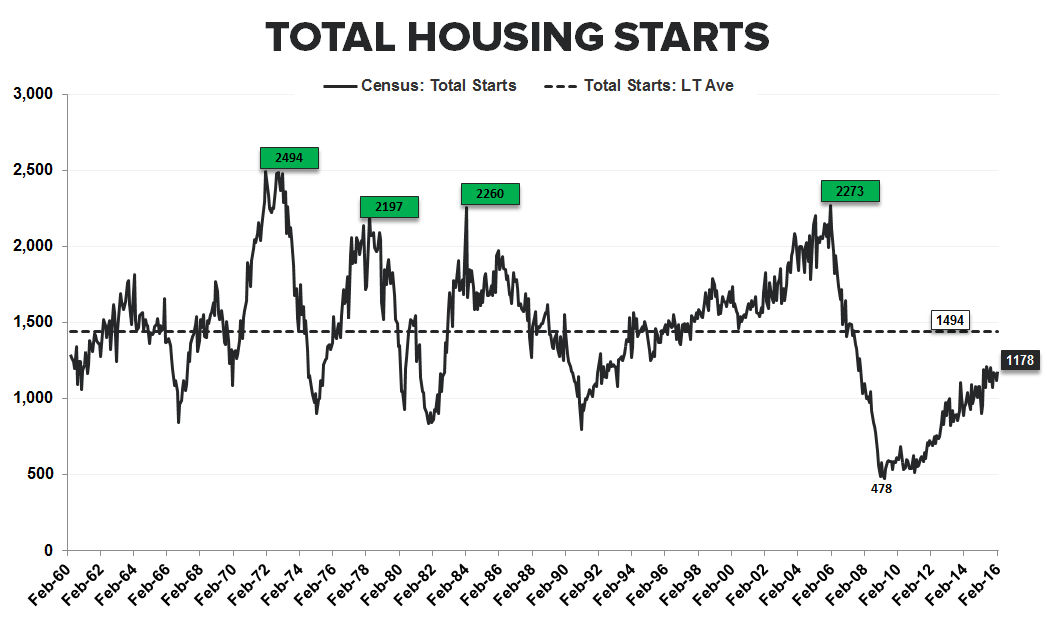

- Starts vs Sales | A Tale of Two Slopes: Builder Confidence sits at a 9-month low and the slope of sales in the New Home Market is negative (3rd chart below). These measures stand in notable contrast to the flat trend in total starts and positive slope in SF construction over the TTM.

On balance, the data mosaic across housing continues to support our negative outlook. As the data stands, we would not view slowing HPI, decelerating volume growth in the existing market, flatlined Starts activity and negative 2nd derivative trends in New Home Sales and Builder Confidence as a particularly bullish fundamental factor constellation, especially heading into the seasonally tough 2Q/3Q equity performance periods (see last 2 charts below).

About Housing Starts & Permits:

The US Census Bureau records the number of new housing units that have obtained permits for construction and those that have begun construction. This data includes new buildings intended primarily as residential units. The US Census Bureau defines a start as, “Start of construction occurs when excavation begins for the footings or foundation of a building.”

Joshua Steiner, CFA

Christian B. Drake