It was inevitable. But it's finally happening. The belief system that central bankers can bend and smooth economic gravity ... it's breaking down.

In case you missed it, back in February, Hedgeye CEO Keith McCullough wrote an Early Look entitled, "The Big Bang Theory" (we unlocked it). He posited that the entire central-market-planning belief system/edifice could implode. What would happen if macro markets no longer believed in the potency of central planners at the Fed, BOJ and ECB? What if currencies actually went up ... and stocks went down in response to central bank easing?

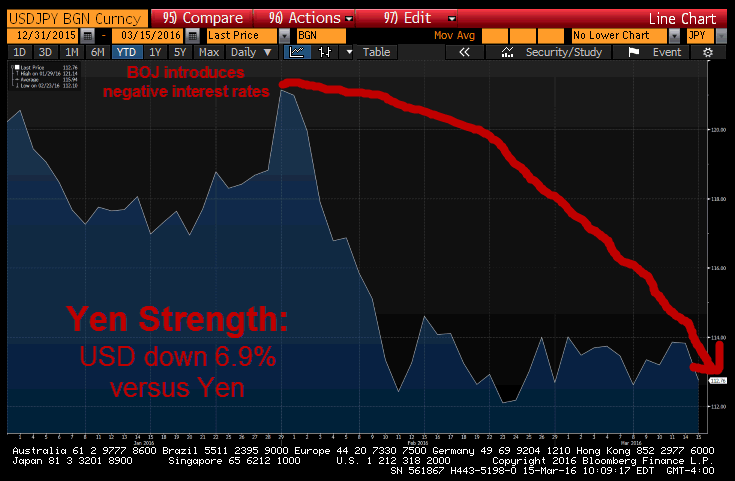

Well, that's what's happening in Japan right now. Look at the chart of the USD/Yen since the BOJ pursued negative interest rates in January.

This morning, the BOJ downgraded its view of the economy, but held interest rates at minus 0.1% and kept asset purchases at a pace of Y80tn a year. Here's analysis from McCullough in a note sent to subscribers:

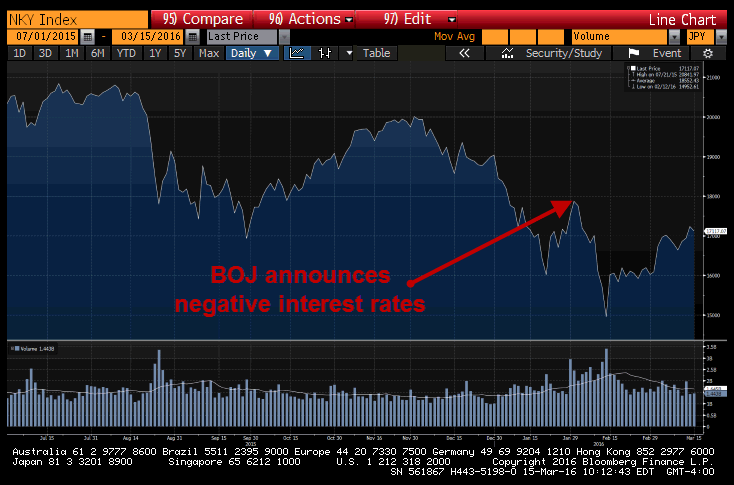

"If you’ve been bearish on the #BeliefSystem (central-market-planning) breaking down in Japan alongside us, congrats – Japanese stocks failed @Hedgeye TREND resistance overnight as the Yen popped (again) on a BOJ statement day. The Nikkei is down -0.7% to -10% for the year-to-date. It is not clear how the bulls could be trumpeting losing money year-to-date."

The Nikkei is down -2.3% since the BOJ announced NIRP.

So where do we go from here?

We'll say it again. The biggest market risk is believing central banks' economic forecasts.