“Rebalancing represents supremely rational behavior.”

-David Swensen

In reviewing my old college economic-cycle-top notes (there have been 3 since I graduated = 1999, 2007, and 2015), I came across this one from Yale Endowment chief asset allocator, David Swensen.

While I don’t think anyone is “supremely rational” when it comes to investing at economic cycle tops and bottoms, I do find it interesting to observe human behavior as the signs of topping (and bottoming) processes become more obvious.

Swensen wrote that in the year 2000 stating that “disciplined rebalancers need to sell what’s hot and buy what’s not.” If you have a supremely long-term investment horizon, that’s probably going to work more often than it doesn’t. If you’re like > 90% of money managers out there today, chasing monthly and quarterly returns – not so much.

Back to the Global Macro Grind…

If you’ve been rebalancing into anything related to the Federal Reserve’s 2008-2012 (US Dollar all-time lows 2011) Commodity Bubble, you’ve had quite the headache for the last 3 years.

If you just started buying them in 2016, you’re feeling like you might have called the bottom. If you were long commodities vs. short Long-term Treasuries, you’ve had a rough year – but you killed it last week!

I obviously got killed last week. It happens and it sucks. While I’ve been much more bearish on both rates and the Financials (XLF) in 2016 than I have been on commodities and/or their related equities, the only thing that really worked for me last week was long Utilities (XLU). While the “YTD” is pretty short-term in the context of Swensen’s time-horizon, the YTD score still matters:

- US Dollar -1.2% on the week to -2.5% YTD

- Euro (vs. USD) +1.3% on the week to +2.7% YTD

- Canadian Dollar (vs. USD) +0.7% on the week to +4.6% YTD

- Commodities (CRB Index) +3.0% on the week to -1.5% YTD

- Oil (WTI) +7.3% on the week to -1.5% YTD

- Gold -1.5% on the week to +17.9% YTD

- SP500 +1.1% on the week to -1.1% YTD

- EuroStoxx600 +0.1% on the week to -6.4% YTD

- Canadian Stock Market (TSE) +2.3% on the week to +3.9% YTD

- US Treasury (10yr) Yield +10 basis points on the week to -29 basis points YTD

In other words, the closer you were (last week) to being long what hasn’t worked for 3 years, the better you’d have done. That’s why longer-term investors who have been right on longer-term growth and inflation expectations had a supremely bad week!

What is a “longer-term investor”?

- Someone who just buys, averages down, and holds, forever?

- Someone who gets the longer-term fundamentals right?

- Or neither? (I’m not marketing a fund here, so happy to consider other definitions)

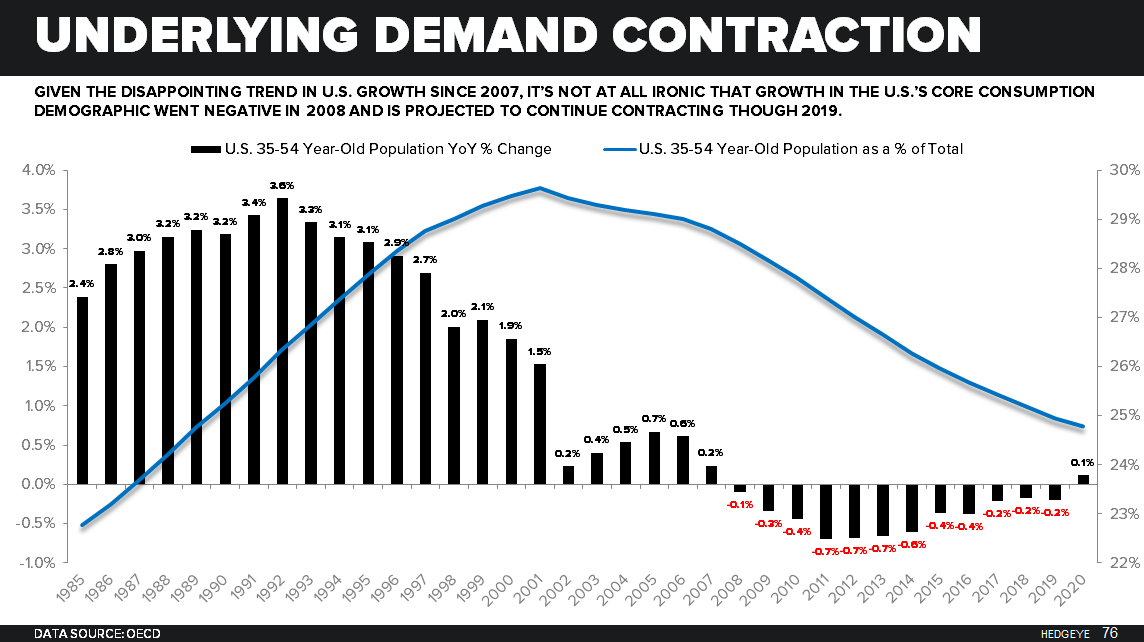

Since the Supremely Long-Term TAIL risk wagging the economic dog here remains a demographic (aging – see Chart of The Day) one, I’m most impressed with long-term investor returns that have nailed that. Slower (growth) for longer has equated to supreme alpha for buy-and-hold investors in long-term sovereign bonds.

Great Keith – you still sucked last week.

Yep. And I’ll suck even more this week if I’m wrong on the economic cycle. But that’s been my “catalyst” since telling you to “rebalance” out of Small Cap, High Leverage, High Beta stocks, 8 months ago.

That’s right. Tell your boss (in my case, my wife) that there’s a guy in Stamford, CT whose research team keeps reiterating that the catalyst to be long:

- Long-term US Treasuries (TLT) = +5.6% YTD (ex the yield)

- Utilities (XLU) = +11.3% YTD (ex the yield)

- Gold (GLD) = +17.9% YTD (there is no yield!)

Has been, and continues to be, The Cycle.

Especially on #LateCycle consumption, employment, and profit metrics (isn’t it sad that Consensus Macro isn’t talking about those?), we’re actually at the YTD lows (see SP500 Earnings, Pending Home Sales, and ISM Services for details).

But, but, but…

On cyclical stuff that has been crashing for 1-3 years, we’re “off the lows”, bros! And the Fed is going to be hawkish about that on Wednesday because:

- Deflation In Commodities has had another short-term “reflation” (isn’t that “transitory” btw?)

- Late Cycle Employment reports (while slowing in rate of change terms) are still “good”

So, they’ll stay tight into an economic slow-down (like they did in raising rates in December). Wouldn’t it be a shocker if the US Dollar goes up on that this week and that we go back to what’s been right since July (selling all reflation rallies)?

I know. That’s supremely short-term. Hopefully my sucking wind is too.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 1.75-1.99%

SPX 1

RUT 1036-1099

USD 95.83-97.38

Oil (WTI) 32.21-39.92

Gold 1

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer