Editor's Note: Below is an institutional research note written by Hedgeye Healthcare analysts Tom Tobin and Andrew Freedman. Our Healthcare team describes the key takeaways after attending last week's annual HIMSS Conference on Healthcare IT. This note contains insights on our Allscripts (MDRX) short thesis along with analysis of other companies in their coverage universe, including athenahealth (ATHN), Computer Program & Systems (CPSI) and Cerner (CERN).

#HIMSS16 (ATHN, MDRX, CPSI, CERN) | INTEROPERABILITY, REGULATORY AND VENDOR TAKEAWAYS

HIMMS TAKEAWAYS

We had a great week out in Las Vegas at the HIMSS Conference, where all of Healthcare IT gathers once a year in the largest trade exhibit show of its kind. Not only was it helpful to attend the learning sessions and spend time on the exhibit floor talking to industry people, but it was equally helpful meeting with clients and comparing takeaways. We learned more than can fit here, but below are our biggest takeaways from HIMMS.

- ATHN - Booth activity was high; more positive on inpatient opportunity.

- MDRX - Booth activity was moderate; more confident in short case after product demos.

- CPSI - Booth activity was extremely low; problems are terminal...watchful waiting to get back on the short.

- CERN - Booth activity was high; no change in sentiment with a long bias... a lot of interest in their pop health services.

INTEROPERABILITY AT AN INFLECTION POINT

Interoperability was one of the top buzzwords of the conference. While the ability to share data between disparate EHR systems exists today, seamless interoperability between systems continues to be limited by the lack of workflow standards, a single patient identifier and vendor openness. The ability to aggregate and analyze clinical information in a way that is useful in the increasingly challenged reimbursement landscape remains limited and a very complex process.

However, emerging standards such as FHIR and a mandatory use of APIs to meet MU3 requirements is laying the infrastructure for data exchange beyond the current C-CDA. ONC also announced additional oversight into the EHR certification process this past week to ensure conformity to the criteria and interoperability standards. Lastly, it has quickly become a political nightmare and a business risk for a vendor to be perceived as a 'closed' system (likely a reason why Epic lost the DoD contract to Cerner). In response, vendors have signed pledges, committing to 'no information blocking'. While it remains to be seen what actually comes out of these pledges, such public commitments are a significant step forward from where we were just one year ago.

Let us know if you would like the slides to the 'Interoperability and Health Information Exchange' symposium.

Advances in interoperability is a positive for some vendors, in particular athenahealth, as they expand their addressable market to health systems willing to take a 'best of breed' approach toward vendor selection (e.g., Epic Inpatient / athena Ambulatory). Over the long-term, interoperability between EHR systems poses a major risk to the HIE vendor community whose sole existence is dependent on the lack of interoperability.

regulatory tailwind/headwind

There continues to be a lot concern among providers and vendors regarding the timing and requirements of MU3, PQRS, VBM and MIPS. These programs are complex and awareness within the physician community surprisingly low based on the CIOs we spoke with. For large health systems, the resources and processes needed to merely be able to submit quality metrics and avoid penalty are immense. The ability of a vendor to be able to incorporate quality reporting into the EHR, thus allowing the provider to select quality measures based on eligibility criteria and provide benchmarking services is of critical concern for CIOs.

athenahealth is well positioned because of their PQRS guarantee and ability to leverage their network to provide data and analytics to track performance relative to peers. While Allscripts does provides quality reporting, we are concerned about their ability to support users through the final stages of Meaningful Use and MIPS given they must maintain three different EHR systems.

VENDOR TAKEAWAYS

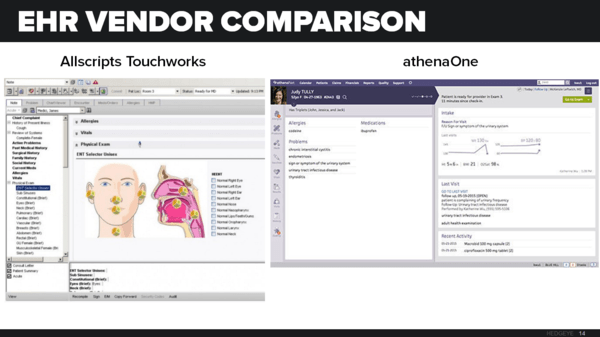

MDRX | We would describe traffic in the Allscripts booth as moderate, with the most buzz around their population health suite of products and not their core EMR and Practice Management solutions. We were very underwhelmed by the graphical user interface (GUI) of all their products compared to their main competitors. From a usability and workflow perspective, the technology was more reminiscent of early 2000s than what you would expect from a company that spends $200+ mill annually in R&D. Overall, there was a lack of common workflow and design between product offerings, which is consistent with a portfolio of acquired and not internally developed solutions.

In our view, Allscripts needs to make major investments in the design and integration of their current systems to be more competitive today and in the future. We left HIMSS more confident in our short thesis.

POPULATION HEALTH

While Allscripts markets their population health products under the 'CareInMotion' umbrella, the four main systems (dbMotion, Care Management, Analytics and ePSi) are siloed from a workflow perspective. It was also difficult to understand which products were necessary in order to make other products work. For example, their core analytics solution really required the purchase of dbMotion in order to get the data needed to run the analytics, although it was also being sold as a standalone solution. This compares unfavorably to competing solutions we did demos with, where the analytics and data aggregation were all part of a single platform with one user interface. While Allscripts promotes the flexibility of a modular design, the market is clearly trending in the opposite direction toward complete solutions.

ePSi

We were impressed with the functionality of ePSi, which is Allscripts business intelligence tool that allows a hospital to do cost based accounting and drill down into the P&L on a case by case basis. A significant problem is the lack of a direct data feed or HL7 capability, which means that data must be batch uploaded from a separate database system or .csv file. The system is also not integrated with their other pop health solutions.

SUNRISE

When compared to competing acute care EHR solutions from Cerner, MEDITECH, Epic and athenahealth, the biggest disappointment to us was Sunrise. Maybe we had too high of expectations going in after all the good things we heard about it, but there was nothing we saw that was competitively differentiated from any of its peers. The primary advantage we saw was in its simplicity, with an easy workflow design that is consistent with anecdotes we have gathered from consultants and customers. Sunrise is Allscripts only integrated EHR solution across inpatient and ambulatory that does not require the purchase of dbMotion.

TOUCHWORKS

Allscripts began rolling out Touchworks 15.1 this year, and per their website is "Designed with the physician in mind, TouchWorks EHR 15.1 features a significant improvement to the existing user interface,user experience, and overall system architecture." However, we did a demo of Touchworks and found that there were only minor design changes:

- Billing Integration

- Order Submission

- Macros (shortcuts)

We would note that these are all features that are currently considered industry standards and have been offered by all major competitors for some time. Touchworks continues to be the Allscripts Achilles Heel, and nothing that we saw makes us believe attrition issues will change course. In fact, another Touchworks loss was announced last week with Dignity Health extending Cerner's PowerChart EHR across its physician enterprise for +400 docs.

In an ideal situation, management would sunset Touchworks and migrate the users over to Sunrise ambulatory. However, given the financial commitment to Touchworks by Allscripts largest clients, and the disruption of migrating, this is an unlikely scenario. Therefore, management will be forced to continue to allocate resources to a non-competitive product that is losing share.

PRO EHR & PRACTICE MANAGEMENT

When we spoke with sales reps at Practice Fusion and eClinicalWorks, the top vendor they were winning new business from is Allscripts. Similar to Touchworks and Sunrise, there was no reason why an educated purchaser would select Allscripts over competing ambulatory solutions (absent price). We observed a current Allscripts Pro customer asking questions about the workflow, specifically that they couldn't figure out what insurance number to enter in a field. There were five Allscripts reps in attendance and not one of them were able to answer the question.

ATHN | The level of activity at the athenahealth booth was high throughout the conference. During the first two exhibit days, they were the only vendor we observed with a packed demo booth all the way through closing. We spoke with an ambulatory sales rep who said that activity was about the same as last year, but the lead quality was higher. On the inpatient side, we followed up with a sales rep after closing on Thursday who said they were booked solid with 40 demos in the first day, and had to actually turn people away. For the entire week, they did about 100 demos, of which 90 were hard leads with most using McKesson, MEDITECH, CPSI and Healthland. This compares to ATHN's current customer base of ~50 athenaOne hospitals with ~25 of those added in 2015. Sales reps described several situations where larger hospitals ( > 75 bed) were anxiously asking about availability in 2017.

We left HIMSS more confident in athenhealth's ability to successfully penetrate the inpatient market.

CPSI | The level of activity at the Evident booth was extremely low, and many times we passed by throughout the day to find it empty. We tried scheduling a demo late in the afternoon on Thursday (last day exhibit floor is open), but they were already packing up. It also goes without saying that the level of activity at athenahealth does not mean good things for CPSI.

We left HIMSS more bearish on CPSI over the intermediate term, and seriously question the future viability of the company amid intensifying competition.

CERN | The level of activity at the Cerner booth was high throughout the conference. Based on discussions with sales reps, most of the customer interest was around their HealtheIntent population health platform. At its core, HealtheIntent integrates clinical data from disparate EHR systems into Cerner's PowerChart EHR workflow. We asked about EHR replacement activity and were told that they are seeing "decent activity", but is "less widespread" than in prior years.

Our sentiment on Cerner remains unchanged after HIMSS. It is clear they are well positioned as the #2 vendor in the space, with a competitive and comprehensive product offering.