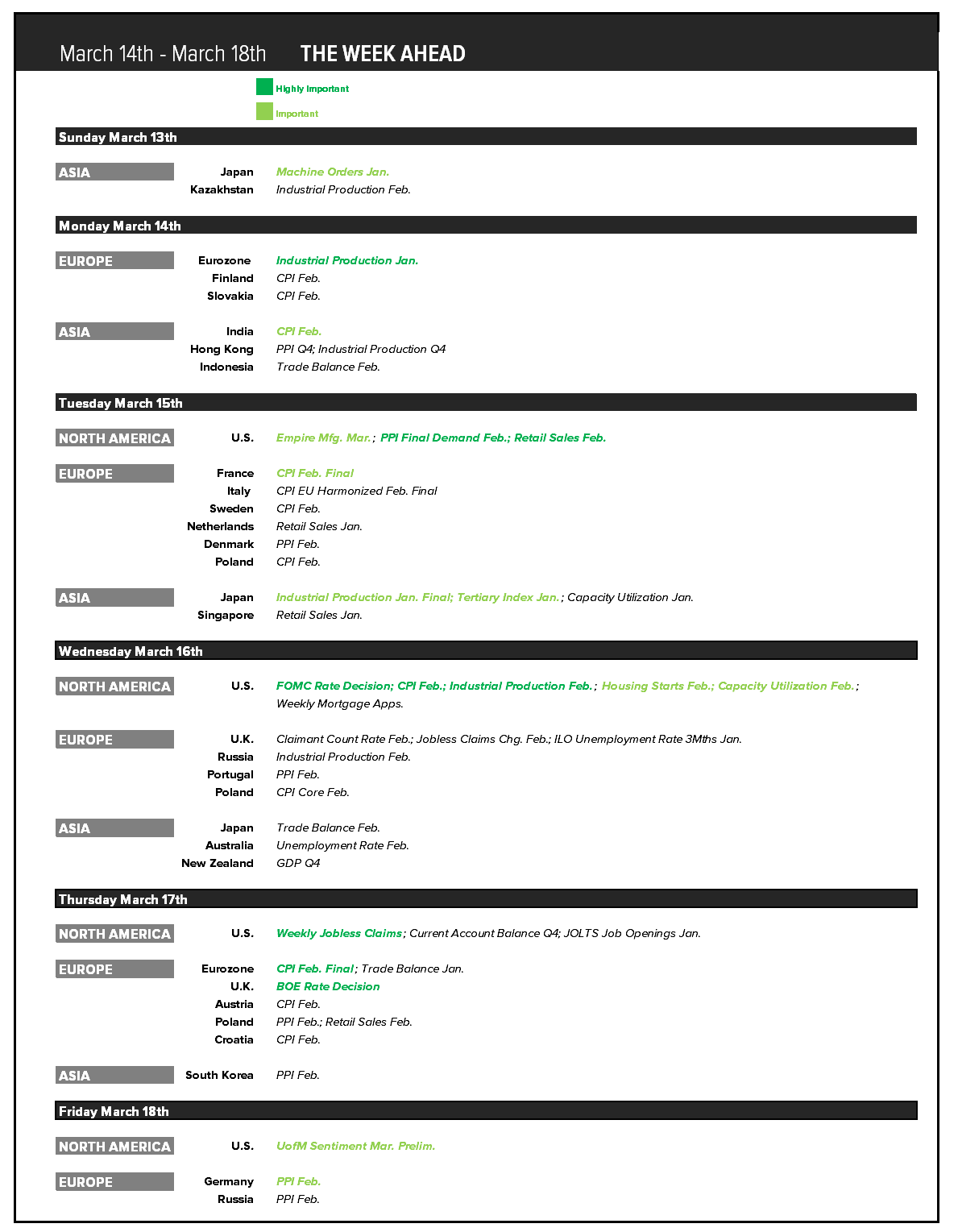

The Economic Data calendar for the week of the 14th of March through the 18th of March is full of critical releases and events. Here is a snapshot of some of the headline numbers that we will be focused on.

CLICK IMAGE TO ENLARGE.

The Economic Data calendar for the week of the 14th of March through the 18th of March is full of critical releases and events. Here is a snapshot of some of the headline numbers that we will be focused on.

By joining our email marketing list you agree to receive marketing emails from Hedgeye. You may unsubscribe at any time by clicking the unsubscribe link in one of the emails.