Two earnings reports caught our eye this morning – ULTA, one of the most defendable growth stories in retail today, and its polar opposite on the quality spectrum – Hibbett Sports. ULTA is one of those names we’ll buy on the down days, and this certainly won’t be one of them. Hibbett, however, is uninvestable to us at any price starting with a $2 – which is 50% below current levels. We thought it was a short at $49, and perhaps even a better one at $36.

As for the quarter…

The company beat expectations by 3 pennies, but that hardly matters. The growth algorithm was simply horrendous. A -0.6% comp, +2.7% growth in revenue, and a 14% EBIT erosion.

HIBB threw Wall Street a bone by talking about investing in ‘omnichannel’ business platform. Mind you, HIBB is the ONLY retailer out there that does not have a dot.com platform. I’m pretty sure that the reason that HIBB does not have a dot.com platform is because Nike does not want them to. We might call that a conspiracy theory if it didn’t have so much truth to it. As for the ‘omnichannel’ platform, isn’t that a retail buzzword that real companies stopped using about three years ago? No matter…HIBB is severely low-balling the cost of a dot.com business. Having the ability to ship from store to home does not make up for a 10-year deficit in spending on a general growth driver.

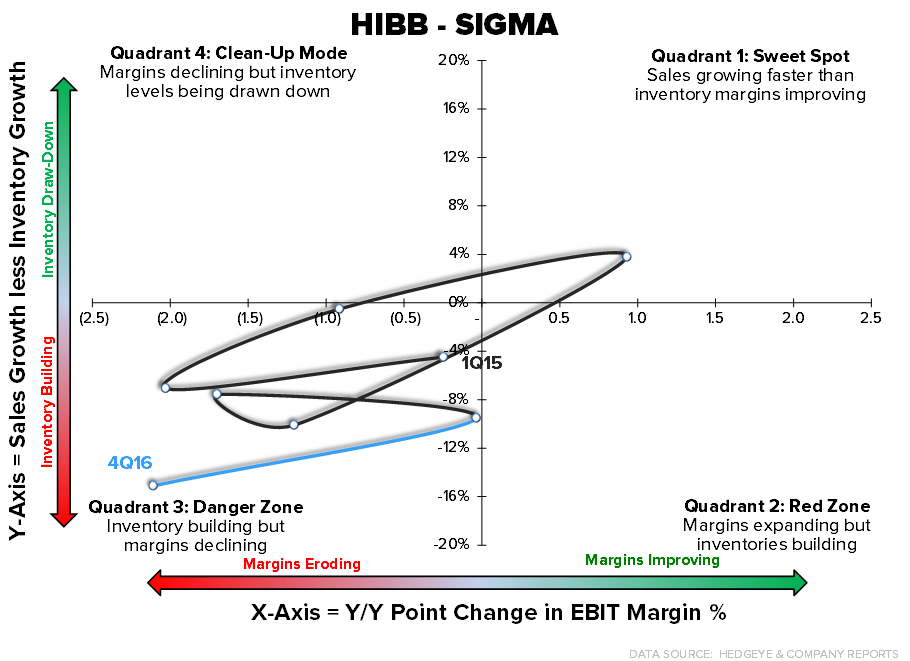

The funny thing is that the omnichannel comments weren’t even the most notable part of the print… it was the fact that inventories were up 18% on a -0.6% comp and 2.7% revenue increase. This couldn’t be spelled out better than in our HIBB SIGMA below. The company took its worst turn to the lower left quadrant this entire economic cycle. So inventories are too high, sales are too weak, margins have already eroded, and capital spending is picking up (too little too late) to try to tap into e-comm.

HIBB just reported $2.87 a share. We think it’s more likely that it earns below $2.00 next year than over $3.00 (i.e. 32%+ downside is more likely than 3% upside).

All in, margins should get cut in half by 2018 at HIBB, and the stock along with it.