Below are our analysts’ new updates on our sixteen current high conviction long and short ideas. As a reminder, if nothing material has changed in the past week which would affect a particular idea, our analyst has noted this. Hedgeye CEO Keith McCullough’s updated levels for each ticker are below.

Please note that we added Pimco 25+ Year Zero Coupon US Treasury ETF (ZROZ) to the long side of Investing Ideas this week.

LEVELS

Trade :: Trend :: Tail Process - These are three durations over which we analyze investment ideas and themes. Hedgeye has created a process as a way of characterizing our investment ideas and their risk profiles, to fit the investing strategies and preferences of our subscribers.

- "Trade" is a duration of 3 weeks or less

- "Trend" is a duration of 3 months or more

- "Tail" is a duration of 3 years or less

IDEAS UPDATES

TLT | XLU | ZROZ | JNK

To view our analyst's original report on Junk Bonds click here and here for Utilities.

If you need evidence that the markets are losing faith in the grand central planning experiment, Thursday’s ECB event was a good indication that there is little cushion-add to easier policy on the margin.

The ECB cut the Main Refinancing Rate 5bps to 0.00%, cut the Deposit Rate 10bps to -0.40%, and cut the Marginal Lending Facility by 5bps to 0.30%. It also increased the “drug” dosage through its asset purchasing program (QE), now delivering €80 billion/month of purchases (from €60 billion prior) and expanded its purchasing mandate to bonds of non-bank corporations (specifically investment grade financial companies).

The market’s response yesterday basically said, “Draghi, we knew you were going to do it, and it doesn’t work.” The Euro strengthened and European equity indices closed on the low of the day. Draghi talked “helicopter money” at the press conference (literally printing money and dropping it out of helicopters for the people), but the market was unfazed.

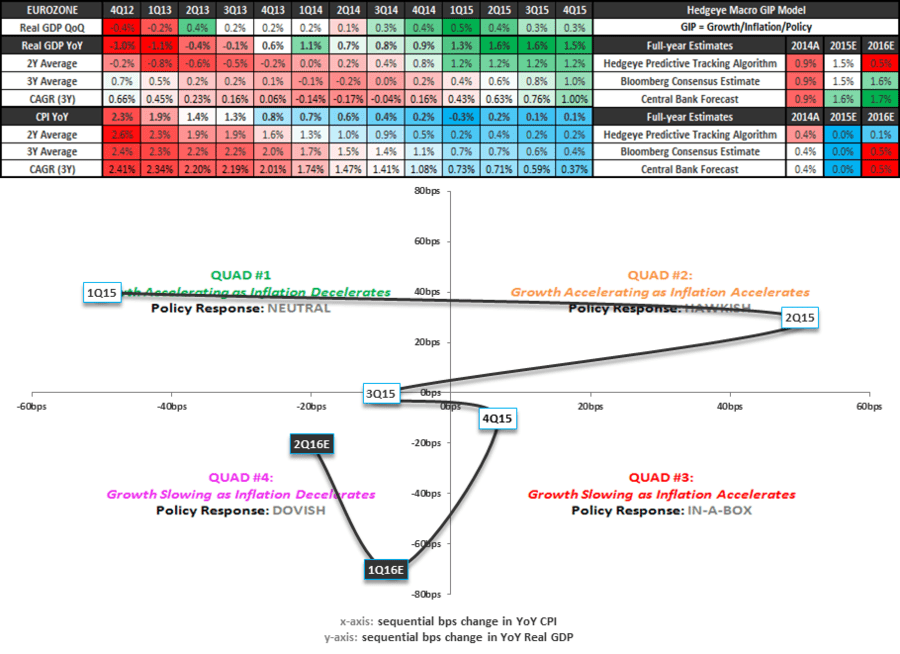

The bottom line is that growth and inflation continue to decelerate in the Eurozone and globally (see our proprietary GROWTH, INFLATION, POLICY model below for a visual). In other words, there is very little central planners can do to stop the cycle and the inevitable deleveraging that must take place in credit (i.e. Junk Bond ETF [JNK]).

Here’s the simple version of the coming deleveraging in credit markets. (Note: this is bad for leveraged corporates – JNK):

- Interest rate cycles have led to lower lows in rates since the early 1980s. The most recent policy measures post crisis (QE, operation twist, and money printing), suceeded in taking interest rates and volatility to historically low levels.

- Capitalizing on the boom in asset prices, corporations financed at the low in spreads in 2013-14 to pursue seemingly profitable business ventures.

- Now those spreads are moving the other way on an epic level of corporate credit.

- So now energy company A needs financing to salvage cash flows at much lower oil prices, but the incremental financing is at higher rates (wider spreads).

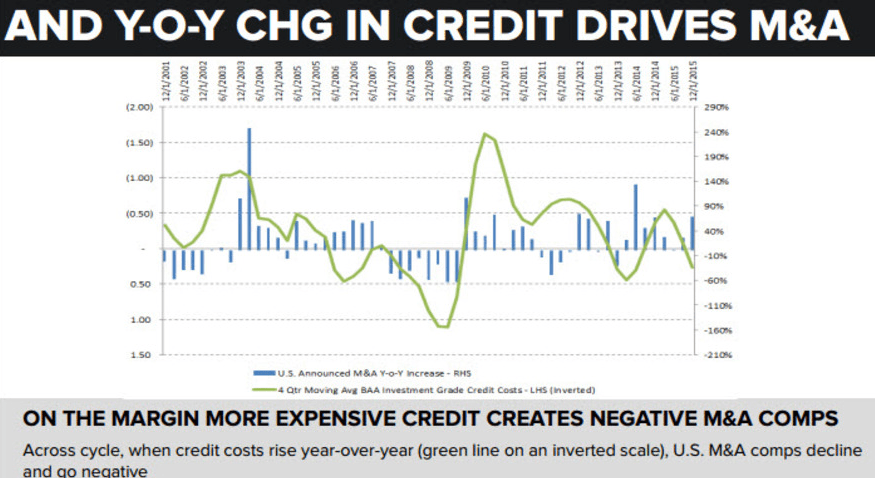

Traditionally, the Federal Reserve could intervene in the market by lowering interest rates and enticing refinancing at lower rates (incremental easing allowing more leveraging). That can't happen this time around. The chart below is the best illustration with long-term context of the Fed’s ability to cushion credit markets currently (it’s virtually zero because rates are already virtually zero). Higher financing costs crush the leveraged debtor (short JNK!).

A final note. Stick with us. The market gets #GrowthSlowing. That's why Utilities (XLU) and Long-Term Treasuries (TLT) remain the alpha generating trades in equities and fixed income this year. (Year-to-date XLU and TLT are up 11.3% and 5.6% respectively versus -1.1% for the S&P 500.)

MDRX

To view our analyst's original report on Allscripts click here. Earlier this week, we sent Investing Ideas subscribers an institutional research note from our Healthcare analysts Tom Tobin and Andrew Freedman. Click here to read the note with insights on our Allscripts (MDRX) short thesis along with analysis of other companies in their coverage universe, including athenahealth (ATHN), Computer Program & Systems (CPSI) and Cerner (CERN).

NUS

To view our analyst's original report on Nu Skin click here.

Nu Skin (NUS) shares jumped almost 4% Friday on the news that CFO Ritch N. Wood purchased 7,500 shares of the company's stock. No change to Consumer Staples analyst Howard Penney short thesis. Even with the three-week rally, NUS shares are down -7.2% year-to-date versus down -1.1% for the S&P 500.

Penney continues to argue that NUS operates a "broken business model" and, due to the ongoing SEC investigation and the questionable sales of VitaMeal, NUS could be exposed to additional regulatory scrutiny. Additional catalysts for the stock's decline?

"If we are wrong we still predict a precipitous deterioration of the company fundamentals. As the company continues to burn through cash, it will be hard to maintain their share buybacks to prop up the stock, especially while under immense pressure from regulators. Additionally, the allegations of the DOJ against USPlabs, among others, specifically called out anti-aging regimens as a focus for current and future investigations. The dietary supplement industry is under enormous pressure from regulators, and MLM’s add an additional layer of risk to the equation."

WAB

To view our analyst's original report on Wabtec click here.

While it is often a challenge to attribute share price moves to events, it seems that several commodity related capital equipment providers have rallied in the last few weeks with the comparatively small bounce in oil and other commodities. We expect rail capital spending to turn down given fleet demographics and customer volume trends, with commodity prices a comparatively minor consideration.

We would look to use the recent squeeze as an entry opportunity, although we acknowledge the risks of adding to a position that has moved against us of late. We still expect Wabtec (WAB) to earn well less than $4 per share in 2016, with weak 2H15 implied order rates as one several supporting data points for that view.

TIF

To view our analyst's original report on Tiffany click here.

Tiffany (TIF) will report its 4th quarter and fiscal year 2015 on Friday the 18th. The company guided 2015 EPS to come in at -10% in its holiday update back in January.

The important incremental information will be updated 2016 guidance. In the holiday update TIF management guided to "minimal" EPS growth in 2016. On the 4Q print, management should refresh their viewpoint and give some more specificity as to how they see 2016 playing out. Last year at this time, management was overly optimistic with their outlook. The guidance was also for minimal EPS growth in 2015, which is now tracking to a 10% decline.

The stock has rallied, along with the whole retail sector, since last month's retail sales beat. February retail sales (Tuesday) will be out before TIF's earnings which could influence the stock, even though that release does not include jewelry store specific details.

We still see street expectations as too high in the upcoming fiscal year.

LAZ

To view our analyst's original report on Lazard click here.

On Friday from Europe, Deutsche Bank joined the trifecta of investment banks now warning about a significant revenue slowdown in the sector (JP Morgan and Citigroup already mentioned that capital market trends are down -25% and -15% year-over-year respectively in recent first quarter investor presentations). While DB wasn’t overly forthcoming on details, the largest investment bank in Europe outlined that industry revenues are receding as clients are pulling back from trading fixed-income securities. In addition, the German bank outlined a vacuum in deal making as corporate sponsors are refraining from the M&A market.

Lazard (LAZ) is especially impacted by this warning, with over 35% of its merger revenues in the Eurozone. Furthermore, stateside we see the over 100 basis point increase in corporate credit costs being a big deterrent to new merger announcements as historically a move higher of that magnitude in funding costs has impacted M&A by -20%. We think this soft start for all the capital market businesses will metastasize into a bigger decline as we get further along into 2016.

MCD

To view our analyst's original report on McDonald's click here.

Restaurants analyst Howard Penney reiterates his long call on McDonald's (MCD). He has no new update this week.

W

To view our analyst's original report on Wayfair click here.

Insider sales are hitting new highs for Wayfair (W) in March. The chart below shows insider sale volume relative to the stock price. Insiders have now sold nearly $110mm in Wayfair stock since the lockup expiration.

We view management's overall appetite to unload shares as a negative for the W business model long term. We think this online-only business model is one that will never be profitable in the home furnishings space in the long run. Management’s presentations may be bullish on the business model, but their trading activity points to the opposite.

RH

To view our analyst's original report on Restoration Hardware click here.

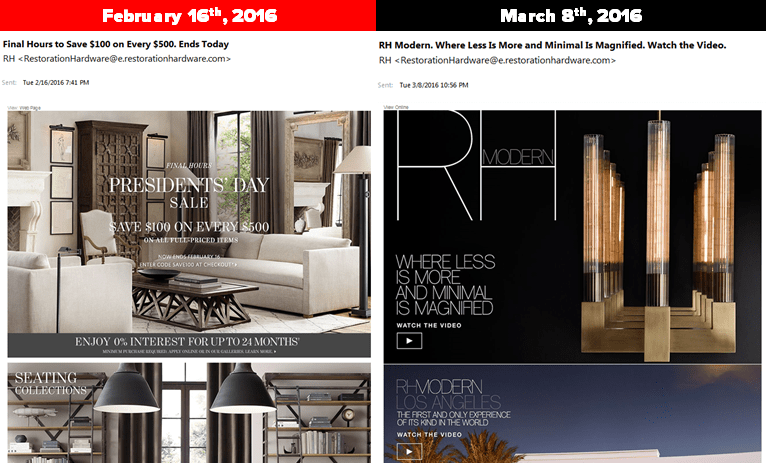

Restoration Hardware (RH) noted with its 2/24 preannouncement that it would be moving away from promotions towards a membership model. But what happened just prior to the 2/24 announcement was the elimination of any and all promotional emails.

In fact, the last one was sent out on 2/16, and was arguably just as ‘Brand Destructive’ as the ones that came before it. In 3-years covering RH (the RH as it exists today), we’ve grown used to investors routinely talking about the latest promotional email from the company, and questioning why they exist for a brand that is supposedly high-end. Those emails were sent not only every day, but multiple times each day to tens of millions of consumers – most of whom will likely never spend a dime at RH.

The punchline is that RH is changing the way it markets its product not just because business is weak and it had a problem delivering on Modern. But because it’s what the company needs to do in order to double in size. The m.o. of the past economic cycle will certainly not take it through the next one. In fairness, RH was ready to roll this new strategy out roughly 18 months ago, but our sense is that it had such great momentum that it did not want to risk being disruptive.

Now, the time is right. It might be painful. In fact, it will almost certainly be painful. But do you think that, just maybe, a $38 stock and 25% downward earnings revision already knows this?

ZBH

To view our analyst's original report on Zimmer Biomet click here.

No update on Healthcare analyst Tom Tobin's Zimmer Biomet (ZBH) short call this week but Hedgeye CEO Keith McCullough issued this ZBH sell signal in Real-Time Alerts Friday:

"While it's interesting to dream up permabull market narratives about CNBC's "Dimon bottom" or how the ECB is going to save the world from a credit cycle, it's easier (on a Friday, on no volume) to deal with reality.

Reality is that stocks like Zimmer got hammered to the FEB lows because fundamental growth and earnings are #slowing. That reality has not changed (see ISM Services report hitting a new lows last week).

As a reminder, our team's long-term view calls for slowing/declining unit volume and deteriorating pricing. The impact to gross margins should be significant with very little spending flexibility within the organization.

Short Green,

KM"

FL

To view our analyst's original report on Foot Locker click here.

Hedgeye Retail analyst Alec Richards explained why the expansion of Nike’s (NKE) direct-to-consumer business is bearish Foot Locker (FL) in a recent video on HedgeyeTV.

Click here to watch.

GIS

This stock is not likely going to go up 20% in the next year, but we do believe it will fare better than most in the consumer staples sector, especially as we head into an economic slowdown. That's why GIS is up 5.5% year-to-date versus down -1.4% for the S&P 500.

In the past few newsletters we've noted the effect Walmart is having on GIS, how its Yogurt business is faring against competitors, and how the company is broadening the distribution of its top 450 SKUs. On the M&A front, barring any screaming deals in the market place we don’t see General Mills (GIS) buying anything over roughly $1 billion in sales, just given the added complexity it would cause. So they will most likely continue the string of pearls approach in the Natural & Organic/Snacking categories. This does not rule out the possibility of GIS being bought, 3G & Kraft Heinz could be getting back in the mix as well, although it seems too soon for another deal this big.

DRI

To view our analyst's original report on Darden Restaurants click here.

This week we learned that Darden Restaurants (DRI) CFO Jeffrey Davis resigned. Davis joined the company in July 2015 and was replaced by Ricardo Cardenas, who served as the company’s chief strategy officer since July 2015. For what it's worth, Cardenas was originally passed over for the CFO job. That didn't stop DRI shares from rising 4% this week as the company posted healthy expected same-restaurant-sales growth for its just-completed quarter.

Still, Hedgeye Restaurants analyst Howard Penney is unpersuaded. We've noted the significant issues facing DRI's Olive Garden chain, including remodeling 400 older RevItalia restaurants. Note: Olive Garden makes up roughly 56% of sales.

In a recent institutional research note, Penney notes:

"Olive Garden is now lapping positive same-store sales figures with the biggest hurdles coming over the next three quarters. Please see below, the first chart displays same-store sales going back to 1Q12, with four quarters of consensus estimates. In 3Q16, Olive Garden will be comping against 2.2% sames-store sales growth. The second chart shows monthly traffic trends at Olive Garden. As you can see positive traffic is a rare occurrence, with just three positive months of traffic in the LTM November 2015 period."