Editor's Note: See today's 259k jobless claims print? That's not the bullish harbinger many investors make it out to be. In fact, it might just be the last shoe to drop before a recession sinks in. That's one of the key takeaways from a recent institutional research report written by our Financials analysts Josh Steiner and Jonathan Casteleyn. Below is a brief excerpt. To get full research access email sales@hedgeye.com.

EXCERPT FROM RESEARCH REPORT:

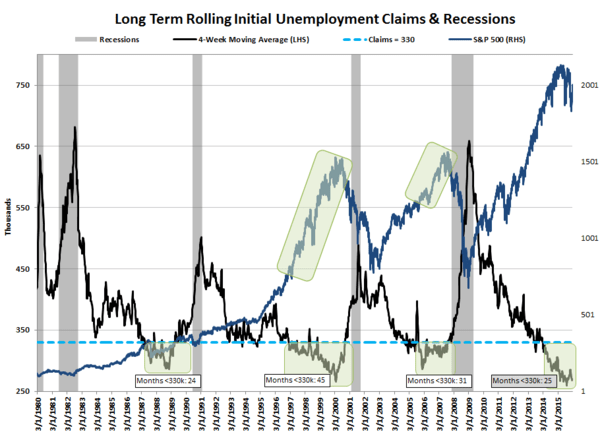

"... While we may sound a bit like a broken record on this point, we still think it bears repeating that the cycle is late stage. The chart below shows that there has historically been a time limit on how long the labor market can run this hot.

The chart shows that in the last three cycles, claims have run below 330k for 24, 45, and 31 months before recession set in. The current sub-330k run just entered month 25. That puts us one month past the minimum, 8 months from the 33-month average, and 20 months from the 1990s record-setting expansion."

CLICK TO ENLARGE