The ECB popped its latest Viagra pill this morning in a desperate attempt to stimulate Europe's flacid economy. Markets didn't buy it and did the exact opposite of what central planners intended.

In other words...

The euro soared and equity markets are falling.

A brief recap of the ECB announcement:

- The ECB cut its main interest rate to 0% from 0.05%

- The deposit rate was trimmed from -0.3% to -0.4%

- Quantitative easing purchases increased to €80 billion per month, from €60 billion, and was expanded to include corporate bonds

- Marginal lending rate is now 0.25% from 0.3%

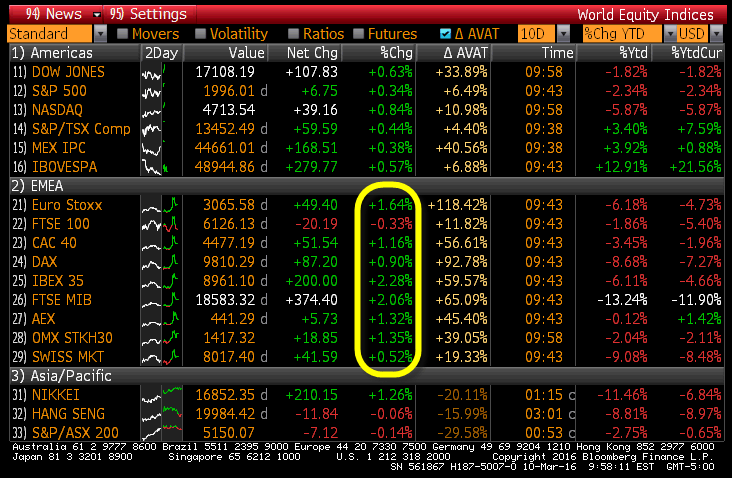

What happened in macro markets following the policy announcement is even more important. European equities rallied, at first, with Italy up as much as 2%, following ECB head Draghi's press conference.

Then, it all came apart and equities fell.

Here's European equities before (10 am ET):

... And after (11:30 AM):

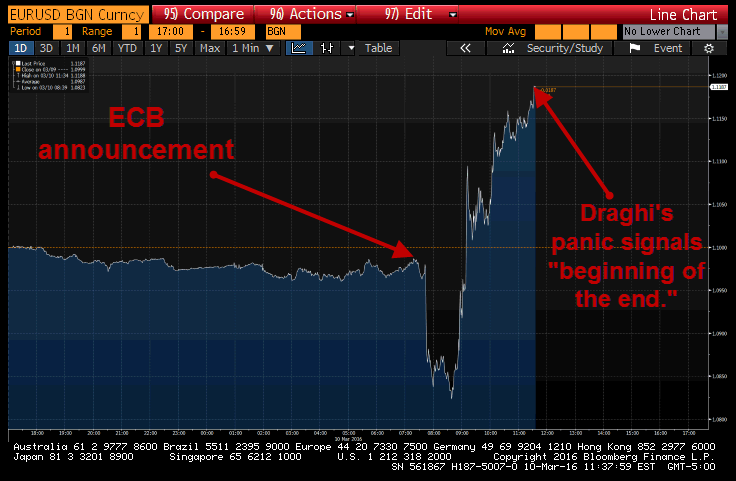

Meanwhile, as Draghi was laying out the ECB stimulus measures, the Euro tumbled 1.4% versus the U.S. dollar (i.e. Draghi's intent) but then completely reversed. As of now, the Euro/USD is up 1.3%.

Here's what that looked like this morning:

Macro markets are wising up and clearly questioning the potency of central-planning policy tools. Note: The ECB cut its outlook for growth and inflation:

Key takeaways?

"Why not ask yourself if this is the beginning of the end – of the grand central-market-plan," Hedgeye CEO Keith McCullough wrote on 2/23 in a recent Early Look entitled "Big Bank Theory." McCullough continues:

"My Big Bang Theory for the #CurrencyWar (one of the Top 3 Themes in our Macro deck right now) is as follows:

- Japan is no longer able to convince markets that it can burn its currency at the stake on command

- Japan’s Yen starts to rise, and Japanese stocks start to crash

- Europe then fails to convince consensus of the same

- Euro goes up (instead of down) on Draghi’s next central-market-planning day (March 10)

- European and US stocks resume their current crashes and go straight down

I know, I know. It’s just a theory. But it’s what I would call one that has a probability that is rising, not falling, in rate-of-change terms."

So here's what you really need to know: