Our takeaway with respect to the relief in credit spreads, especially in the resource space, is that we believe the tightening is temporary, driven by a shift in policy expectations, and the result of a heavy squeeze in deep cyclicals.

To borrow a line from Drake’s Early Look Tuesday recapping January’s consumer credit data, “with household debt still very much elevated and no rope left on lowering debt service costs, the capacity for debt to support consumption growth over the intermediate and longer term remains constrained.”

We would also echo the “lack of rope” on the corporate investment and financing side of the equation, particularly as it relates to forward looking earnings expectations in the space.

Below we offer a series of charts and tables to support the argument that there is less room for "more rope" from a policy-induced financing perspective. Here are our main conclusions:

- The leverage thrown on at elevated commodity prices and the lower bound in rates has decidedly started moving the other way since 2014, and the recent squeeze in resource-driven sectors, and the move in spreads won’t help cushion the necessary balance sheet flush

- EBIT estimates for the balance of 2016 and 2017 remain optimistic, and we expect the contraction of capital on balance sheet to be an earnings headwind in the resource space for a longer period of time

- There has been a healthy consolidation in consensus short commodity/long USD positioning and rate hike expectations heading into the year, and this consensus expectation has now shifted the other way into the policy catalysts, starting with the ECB this morning

----------

- The most heavily shorted, larger cap cyclicals in the Resource and Materials related space are also the top equity performers on a 1-mth window. When deep cyclicals in oversupplied, mature industries double in less than 2 months, we call that a squeeze:

- With a breather in the USD ascension YTD, The short-term move in iron ore, gold, WTI etc. has helped their respective equities, the equity indices of resource leveraged countries, and the sovereign and corporate resource-leveraged sovereigns:

The takeaway as it relates to credit extension and contraction is that credit has already meaningfully tightened on top of peak leverage in commodity space, and we expect the capital flush will continue to be an earnings headwind in Q2. Spreads in the resource heavy space are meaningfully higher Y/Y despite the temporary pullback:

- Spreads remain +~200-250bps wider Y/Y after widening in 2015 for the balance of the year

- A cyclical trough in rates followed by a meaningful breakout in spreads hasn’t historically reversed in the same cycle

- Resource-related credit (largely mature industries ex. U.S. shale) jumped from 5% to 14% of aggregate corporate credit outstanding in the 10-year period from 2004-2014 (sample of 34 producers)

- Reported interest expense jumped 2.5x for this same group over that 10-year period despite the access to increasingly cheaper financing to the 2014 low in corporate credit spreads. This financing ability has already moved the opposite way for a long time

- EBIT estimates remain too optimistic in our opinion for 2016, and much of the growth is expected in the resource space (the last two charts exemplify the Materials space)

EARNINGS: The backside of cheap leverage at high commodity prices is an extended capital flush that lasts for a long period of time. In reality there is too much capital chasing production that can’t be absorbed

- This balance sheet deleveraging manifests in D&A, write-downs, impairments and even haircuts for some over a long period of time which we expect to offset the lapping of difficult comps (a bull case scenario to the awful Q4 earnings season which is winding down). Judging by Q4 earnings many companies made the choice to avoid the necessary charges for a future time in the hopes of a price rebound

- Capital in play per oz. of production has only began inflecting off historic highs despite production efficiency gains (the backside of an industry-wide capital spending boom)

This balance sheet deleveraging is slowly on the move, but we argue it will get worse throughout the balance of the year as the cycle gets longer in the tooth.

Below we re-worked two slides in our Q1 themes macro deck to paint the cyclical picture of a breakout in credit spreads (credit’s share of GDP) within the longer-term debt cycle of which little policy “rope” remains for another cycle to commence.

Excluding the increasingly limited financing availability on the corporate investment, a number of other metrics suggest a tighter credit environment broadly (which helps elongate consumption and investment).

As our financials team outlined in its re-cap of the Q1 2016 Senior Loan Officer Survey, a tightening in commercial & industrial (C&I) loan standards continued for the second consecutive quarter. And not only did the net percentages of lenders tightening standards for those categories increase, but demand for C&I loans declined. Additionally, the Fed's survey this quarter included special questions regarding forward expectations, and loan officers indicated that they expected a further tightening of standards, increasing of spreads, decreasing volumes, and deteriorating credit quality over the course of 2016.

The risk to being long a deflationary credit unwinding is that the Fed has more RELATIVE room to fight a deflationary burden with easier policy (weaker USD, measures to lower rates, and money printing to help cushion the debt burden) when compared to other central banks, which is why the “Fed Put” still has more credibility with deteriorating data (and the expectation that the dot plot will be revised lower next week). However, the current cushion is non-existent compared to previous peaks in Fed Funds:

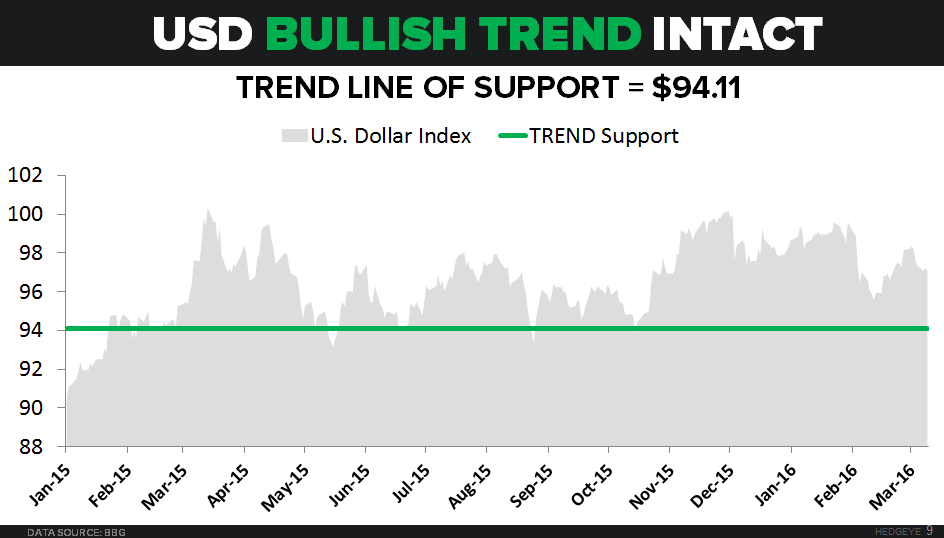

Concluding with behavioral, market-based expectations, the pull-back in Fed Funds expectations YTD, and a healthy rebalancing in net USD long, commodity short positioning (net futures and options positioning), the market is now leaning the other way into the March policy catalysts (long Euros, treasuries, and gold, and short dollars on the other side). This set-up suggests Draghi can’t do enough to outweigh consensus expectations this morning. Overall, both the longer-term fundamental and quantitatively bullish set-up for the USD remains intact. For a walk through in how we see this playing out, we’ve pre-coined the “BIG BANG”

Ben Ryan

Associate