This DKS earnings event was perplexing. On one hand, the company gave every reason for just about any type of investor to never look at owning it again – at least until we emerge from the next economic recession. On the other hand – the stock actually traded up on the print. Yes, up. And we’re not talking a good ‘ol fashioned squeeze on a crowded short that is down and out. This is a name that was already up 28% for the year-to-date heading into the print and had only 7% of its float held short (below 10-yr avg of 9.7%). Now we’re left with a company that has underinvested in any effort to capitalize on the changing way that consumers are incrementally buying product in this corner of retail. Management’s answer? Aggressively buy Sports Authority stores as a key competitor goes bankrupt. NOT a good idea. Based on what we see today, we’d be on the short side of this name.

Here Are Some of Our Concerns

1) The earnings algorithm was horrible. DKS de-leveraged 4% sales growth into a 17% and 13% decline in EBIT and earnings, respectively.

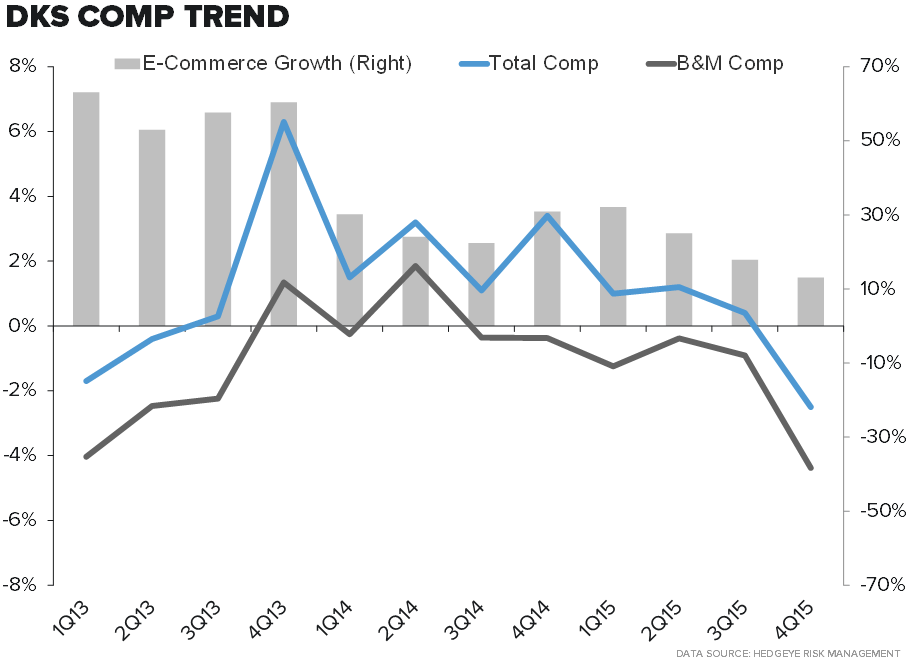

2) Comp missed, and came in at -2.5%, but keep in mind that this INCLUDES e-commerce. On a store-only basis, DKS comped -4.4%, which was the worst performance since 4Q08 – when we were in a significantly more perilous environment.

3) New Store Productivity weakened at a greater rate than we can calculate – ever.

4) DKS SIGMA looks really really bad. Simply put, whenever a company puts up such a bad gross margin reading (-200bp), you want to at least see that its sales/inventory spread improved on the margin. That was not the case with DKS, and the market looked right through it.

5) Store Funk [was Mike Tyson in a ‘funk’ at the end of his career, or did he just get old and tired]

The performance of Dick's B&M stores remains poor. Stores comped down 4.4%, the 6th negative comp in a row, slowing 180 bps on a 2 year basis. For the first time since 2009 we saw a sequential decline in number of stores at -3, the biggest drop ever. New store productivity is trending down as well, yet the company still has plans to open 45 stores this year, and then another 60 stores next year to hit its 2017 target. If the stores are comping negative, new doors coming in at lower productivity, returns are declining rapidly on the incremental store investments. We think at this point the store targets are a pipe dream.

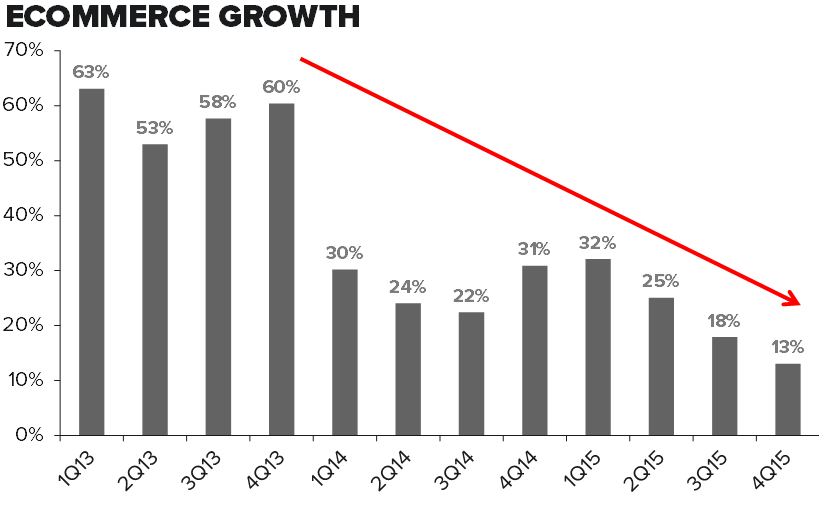

6) What Gives with e-commerce? If there was only one statistic we can look at to gauge the health of a brand, it would be e-comm growth. That’s unfortunate for DKS, as e-comm slowed sequentially for three consecutive quarters, and is growing today at a mere 13%. That level of growth for a company with such an immature e-comm business is simply unacceptable. Interestingly, Dick's online business grew below the rate of online retail as a whole, which grew 14.7% in 4Q15. In fairness, DKS should see an acceleration when it takes full control of its e-comm business in 2017. But unfortunately, hundreds of competitors will have advanced by then.

7) Sports Authority. DKS is aggressively going after TSA stores as its long-time competitor goes under. As backdrop, Sports Authority does about $3.5bn in sales in its ~465 stores. If we academically assume that the stores being closed operate at a 20% productivity discount, we get to $820mm in sales. DKS management indicated 90 to 100 (68%) of the 140 closing stores overlap with their stores, which looks like a fair number given our overlap analysis below shows 75% overlap (less than 15mi apart) for Dick's stores with all of Sports Authority. Therefore the total opportunity for DKS is ~$550mm or 7.5% in growth if they can take ALL of the revenue from closed Sports Authority stores. Claiming a more plausible 20% of sales – which will come at a significant capital cost - would mean a 1.5% growth tailwind.

Let’s be clear about something…in the past when DKS has acquired competitors and then subsequently rebranded them, it’s been at a point when the industry was in its adolescence. Today it is extremely mature – at least in the form that Wall Street knows it. It’s no longer about acquiring Sporting Goods stores, but rather about building a defendable brand that will own the consumer in all channels of distribution. That does not appear to be what DKS has in mind, which is unfortunate, as that would be a story worth getting behind.