Editor's Note: Below is a brief excerpt and chart from today's Early Look written by Hedgeye Director of Research Daryl Jones. Click here to learn more.

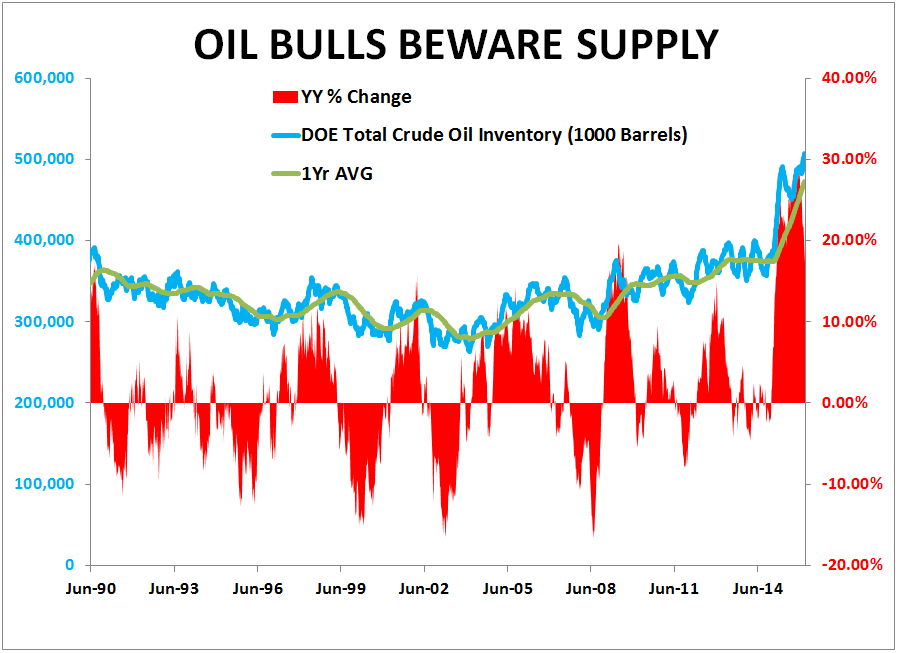

"... So while traders may continue to chase the “wabbit” on the long side of oil, the data tells a different story. In fact, as highlighted in the Chart of the Day, oil supply continues to reach new highs in the U.S. at an accelerated rate. Currently, supply in the U.S. is running up +20% y-o-y!"