“Family quarrels are bitter things. They don't go according to any rules. They're not like aches or wounds, they're more like splits in the skin that won't heal because there's not enough material.”

-F. Scott Fitzgerald

The quote from Fitzgerald above seems an apt way to describe the current state of the Republican Party. No doubt with Donald Trump’s wins last night in the Michigan and Mississippi, the fissures in the “family” are only widening.

In Michigan, Trump took 39% of the vote and in Mississippi he took 50% of the vote to strengthen his delegate count to 458, which is a 99 delegate lead over second place Senator Ted Cruz. Despite this lead, Trump still only has 45% of the delegates and is a long way from locking down the 1,237 delegates he will need to claim the Republican nomination.

So, what happens from here?

The next two major catalysts are the Ohio and Florida primaries in six days. Ohio is a must win for Governor John Kasich and Florida is a must win for Senator Marco Rubio. Currently, Trump has a wide lead in the most recent poll aggregates with a 16 point lead in Florida and a 4 point lead in Ohio.

For the Republican family elders, though, there is probably some solace in the volatility and unpredictability of these state level polls as exemplified in the Michigan primary on the Democratic side. Going into last night, Secretary Clinton was up by some +21 points and lost. So much for all that money spent on polling!

The Florida and Ohio primaries on March 15th are critical because they are likely to decide the fates of Kasich and Rubio, but they are also the beginning of the winner takes all primaries. On March 15th, there are 367 delegates up for grabs across 5 states and 1 territory and they are all in winner take all primaries.

At a minimum, if Trump wins Florida and Ohio, the math becomes very difficult for anyone else to get the nomination. If he doesn't, then it is very likely a contested convention is in play. In this scenario, the nominee will be decided on the convention floor by rules set by the RNC’s Rules Committee. Those rules, like most rules in family feuds, can be changed and will be set shortly before the convention. In this scenario, the proverbial family feud is likely only just beginning!

Back to the Global Macro Grind…

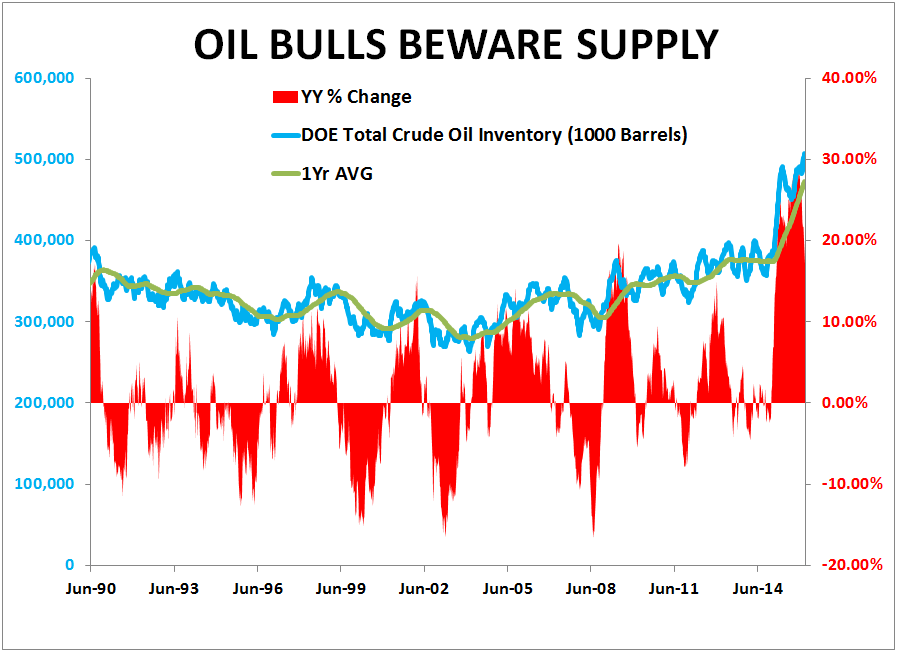

Back in the real world of data and asset prices, there is far less drama and intrigue. (Or is there?) On the oil front, the EIA indicated that it expects oil supply to grow more than previously expected due to production staying at high levels. Meanwhile, API is expecting a crude oil build of some 4MM barrels. Certainly, while oil and oil related assets (like the Loonie) have had a nice rally over the last few weeks, the data continues to fall solidly on the side of oversupply.

The next major catalyst for oil from a policy perspective is likely to be a proposed OPEC meeting in Russia on March 20th to discuss an output freeze. As our colleague Joe McMonigle at Potomac Research has noted, next to nothing will come out of this meeting (if it even occurs) and really the major harbinger for those that are bullish on the price of oil is the fact that Iran’s sole focus is to ramp product and take back share. We think Iran will continue to beat expectations on its ability to increase production and is likely to get to 700,000+ barrels a day of exports this year.

So while traders may continue to chase the “wabbit” on the long side of oil, the data tells a different story. In fact, as highlighted in the Chart of the Day, oil supply continues to reach new highs in the U.S. at an accelerated rate. Currently, supply in the U.S. is running up +20% y-o-y!

The broader issue with oil and natural gas staying at low levels for extended periods is the financial deleveraging that will have to occur in the sector. According to Moody’s, in the year-to-date there have been 18 defaults with half in the energy sector. Last year at this point, there were 11 defaults with 1 in the energy sector. So as year-over-year change goes...

Setting the volatility of oil aside, the most significant event on the macro horizon is tomorrow’s ECB rate decision. Our expectation, which isn’t necessarily out of consensus, is that Draghi and the ECB are going further into unchartered waters (see carton above for the analogy) to fight the shark that is deflation. The key reasons we see the ECB easing further:

- CPI has held below +0.5% for the last 20 months and is currently in negative territory

- PPI was reported in January at -2.9%; and

- Growth by almost any measure in Europe is anemic, which was highlighted this morning by the Bank of France taking its growth estimate to +0.3% on the back of manufacturing confidence falling to 3-year lows.

So with their likely move to more negative rates and a possible -0.4% on overnight deposits, the ECB continues to re-write the rules on monetary policy. Who knows though, perhaps after more than 600+ interest rate globally this will be the one that does the trick.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 1.67-1.94%

SPX 1

VIX 16.11-23.82

USD 96.66-98.78

YEN 111.71-114.51

Oil (WTI) 30.65-38.18

Keep your head up and stick on the ice,

Daryl G. Jones

Director of Research