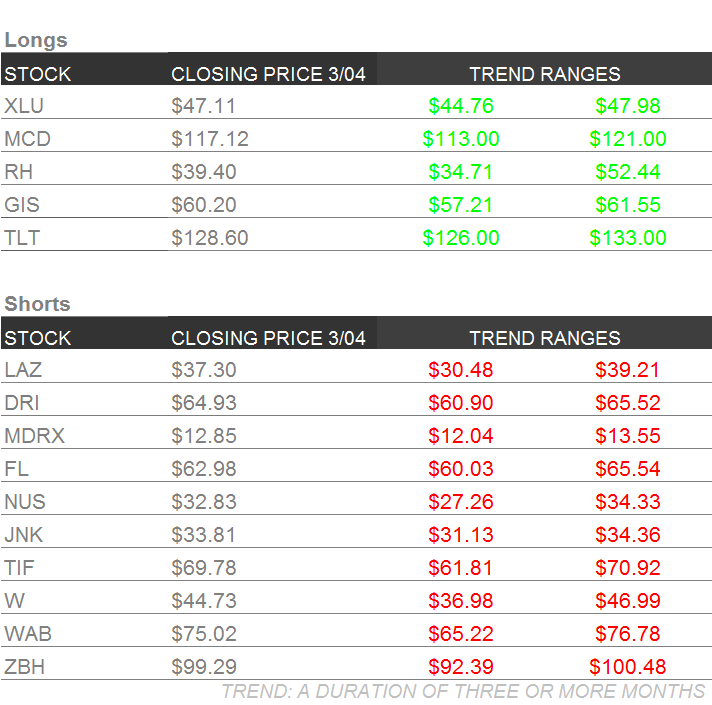

Below are our analysts’ new updates on our fifteen current high conviction long and short ideas. As a reminder, if nothing material has changed in the past week which would affect a particular idea, our analyst has noted this. Hedgeye CEO Keith McCullough’s updated levels for each ticker are below.

LEVELS

Trade :: Trend :: Tail Process - These are three durations over which we analyze investment ideas and themes. Hedgeye has created a process as a way of characterizing our investment ideas and their risk profiles, to fit the investing strategies and preferences of our subscribers.

- "Trade" is a duration of 3 weeks or less

- "Trend" is a duration of 3 months or more

- "Tail" is a duration of 3 years or less

IDEAS UPDATES

TLT | XLU | JNK

To view our analyst's original report on Junk Bonds click here and here for Utilities.

The short-term pain TRADE in the weaker U.S. dollar, and a relief rally in sectors that have gone down for 18-months dominated this week’s performance. For instance, Junk Bond ETF (JNK) +2.2% and Long-Term Treasuries (TLT) -1.5%.

As an Investing Ideas subscriber, you’re more concerned with the TREND and the TAIL. Whether it’s a counter-trend bounce in oil and heavily shorted energy stocks (and the credit tied to inflation expectations) or a sequential bounce in an economic data series with a deteriorating trend, one tick or data point does not make a trend.

If you were long energy over utilities this week, nice trade! Still, we'd remind you that Utilities (XLU) are outperforming the S&P 500 by +10% year-to-date. And that’s with the bounce. By contrast, Energy (XLE) was up 6.5% on the week but is up only 1% year-to-date.

If you called another 53-print on the ISM services number which is technically in “expansionary” territory, that's another nice call! However, if you look at the trend in the series, it is one of clear deterioration. Changes on the margin are most important to our process:

In other words, we can’t emphasize enough the bigger picture from both a data and top-down market signaling perspective.

To contextualize these relief rallies and short squeezes in asset classes and instruments that are counter to our more longer-term view. Here’s what how we think the macro environment plays out from here:

- The market is positioned for more rate hikes into 2016

- The data continues to deteriorate, and market volatility ensues

- The expectation that “all is good” comes off the table and the market increasingly pivots to the view that, throughout 2016, the Fed is going to hike rates in methodical fashion straight into an economic slowdown

- The market takes in the growth slowing pivot in real-time (Treasury rates and the dollar both move lower, and inflation-leveraged assets like gold catch a bid)

Once the policy catalysts are out of the way in the next few weeks, our expectation is a return to outperformance in growth slowing asset classes (TLT and XLU). If you’re in for the TAIL and the TREND call, focus on the data, not the desperate attempts of central planners to arrest economic gravity. A brief reminder: ECB chief Draghi will attempt to walk on water next Thursday.

MDRX

To view our analyst's original report on Allscripts click here. Below is an update from our Healthcare analysts Tom Tobin and Andrew Freedman from Las Vegas:

We are at the HIMSS conference this week in Las Vegas, where all of Healthcare IT gathers for the largest trade exhibit show of its kind. We will have a more detailed report with key takeaways next week.

For now, one item worth mentioning is that Epic and Cerner are saying that Allscripts (MDRX) has been "giving away" Sunrise (acute care EHR) in order to win business. Competing on price would explain why software delivery bookings only grew 12% YoY in 4Q15 on such an easy comp, despite what appeared to be strongest sales activity the company has seen in some time.

NUS

To view our analyst's original report on Nu Skin click here.

No material updated in Nu Skin (NUS) this week. We would like to note the stock has run up approximately 5% this week. We view any short term pop in the stock as a great time to get in short or increase your position.

WAB

To view our analyst's original report on Wabtec click here.

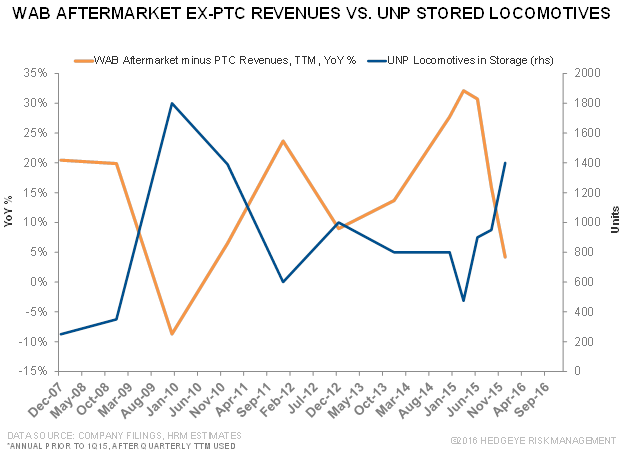

Wabtec (WAB) often talks up its aftermarket business as a stable source of income. However, as railroad equipment moves to storage, WAB’s aftermarket revenues fall as exhibited in the first chart below.

Railroad equipment moves into storage as speeds pick up. One can think of it as turning existing assets more quickly. NSC illustrates the relationship in the second chart. More speed results in less equipment in service. If speeds continue higher, freight railroads may find themselves with ample excess equipment and reduced aftermarket needs amid slow volume growth – a negative combination for WAB.

TIF

To view our analyst's original report on Tiffany click here.

No new update on Tiffany (TIF) this week, but Hedgeye Retail analyst Brian McGough reiterates his short call. Here are the key takeaways from the original thesis:

- "If you’re looking for a U.S. Equity to play our macro team’s #LateCycle #SlowerForLonger bearish themes, here’s a name wrapped in a "Little Blue Box" just for you."

- "The reality is that there are no obvious margin levers to offset the declining growth profile in the business, especially amidst increased late cycle risks."

LAZ

We added Lazard (LAZ) to the short side of Investing Ideas this past week. Click here to read our Financials analyst Jonathan Casteleyn's full stock report.

W

To view our analyst's original report on Wayfair click here.

In this latest quarter, we started to see customer acquisition costs go up on the margin, and advertising efficacy go down. At the same time, Wayfair continues to build an enormous infrastructure of people (employee growth accelerated to +17% sequentially vs 14% in 3Q) for a Total Addressable Market that does not exist.

Our research contends that the TAM for W is $27bn today, compared to management’s assertion that it’s market is $90bn. That is absolutely unrealistic. We continue to believe that this company will never run a truly profitable business. All the signs are there.

RH

To view our analyst's original report on Restoration Hardware click here.

No new update on Restoration Hardware this week. Hedgeye Retail analyst Brian McGough reiterated his long call last week in a detailed updated for Investing Ideas subscribers. Click here to read that research note.

ZBH

To view our analyst's original report on Zimmer Biomet click here.

We’ve been fielding many more questions than normal on our short calls in recent weeks as we spent time in the great cities of Boston, Chicago, and San Francisco meeting healthcare investors and PMs. It isn't very often that the questions and comments coming from the other side of the table fit a consistent pattern, and at times repeat verbatim the same thought.

In the case of Zimmer Biomet (ZBH) the question was on the CCJR and the possibility that the new bundled payment system may in fact slow procedure growth in 2016. Part of what made this interesting was that this was something we’ve been commenting on since last summer.

What made it interesting as well was that it was brought up so many times and so consistently phrased. Under a bundled payment system, hospitals receive a single payment for each patient. If the patient costs more, the hospital makes less money on that patient, and can even lose a considerable amount of money. However, these patients are only 10-15% of the total and can be reasonably identified by their co-morbidities like heart disease, obesity, and uncontrolled diabetes.

Now that the CCJR is in place and compels participation among hospitals covering 25% of all patients, there is a strong likelihood that surgeons under the new bundle payment will avoid sicker patients. This could be a big deal if the US Medical Economy slows in 2016, as we expect. So far, we see trends as stable but good in 2016.

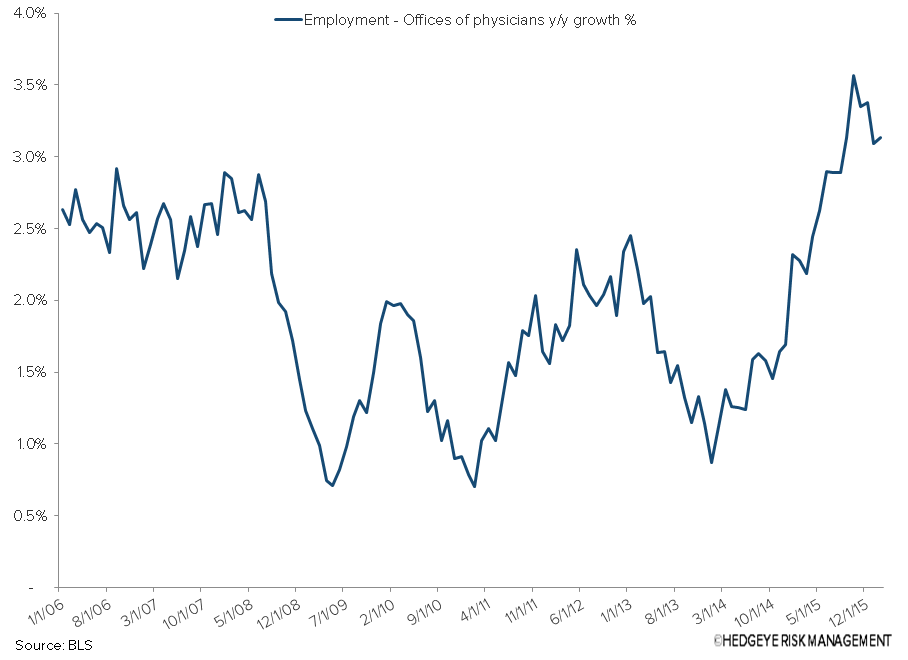

The Labor Department released the monthly jobs report which showed employment at hospitals and other healthcare areas continues to grow at a high rate, although the pace appears to have reached its peak a few months ago. For hospitals, when they are busy, they are hiring. But as the tailwind from the ACA eases, we believe we’ll see a host of procedure types decelerate, including orthopedics, and the pace of hiring will decelerate as well.

Thus far in 2016, we are seeing physician office employment slow faster, but that may be an early sign for things to come for hospitals and ZBH, with the CCJR merely making things worse.

MCD

To view our analyst's original report on McDonald's click here.

Public prosecutors in Brazil have opened a criminal investigation into McDonald's (MCD) in response to complaints from the country’s largest unions. The prosecutors are claiming MCD violated tax and labor laws in the country. In addition to the probe on MCD, prosecutors have also opened an investigation looking into Arcos Dorados, MCD’s biggest franchisee in Brazil.

Although the allegations are serious, we do not expect this to have a meaningful impact on the business. When it does come to a conclusion that will be far down the road as the legal battle will assuredly be dragged out.

MCD remains a top idea long for us in the Restaurants sector. We see them having strong tailwinds behind them with all-day breakfast for the next three quarters. As they refine their value messaging, that will propel the next leg of growth. Additionally, MCD boasts the style factors that we love in tough markets; low beta, big cap, and liquidity.

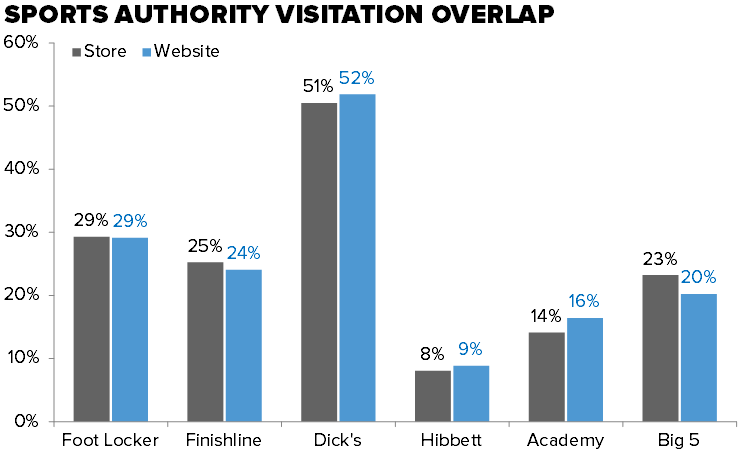

FL

To view our analyst's original report on Foot Locker click here.

After much speculation about the destiny of Sports Authority, this week's chapter 11 filing gives some clarity. Despite rumors of the possibility or closing of all stores, the company will be selling or closing 140 stores out of its current base of about 480. If we assume that these stores operate at a productivity discount to the whole of 80%, we are looking at ~$820mm of the company's $3.5bn in sales up for grabs. Stores closing are expected to take up to three months.

To quantify the upside to Foot Locker (FL), if we assume 35% of Sports Authority sales are in categories customers would purchase at FL (Footwear was 21% back in 2005) and use the customer overlap from our survey of 29%, we are looking at $85mm or just over 1% upside for FL. And that's with all 140 stores no longer selling sporting footwear/apparel.

Bottom line: The Sports Authority bankruptcy is not going to offset challenges facing Foot Locker as it sits at the operational peak of this economic cycle.

GIS

General Mills (GIS) faces some headwinds across their portfolio, and although the 1H of FY16 was a challenge, the company has robust merchandising and consumer plans in the 2H that should improve results.

GIS has embarked on a mission to drive their top 450 SKUs, which represent 75-85% of their volume. Calling it their ‘Power 450’, surprisingly these 450 SKUs aren’t even in all retail locations and formats, broadening the distribution footprint of these top SKUs is priority number one for GIS’s sales team. The organization is also looking at the bottom 450, representing 1-2% of volume and making critical decisions on what products can be discontinued.

We continue to believe GIS is one of the best positioned consumer packaged foods companies due to its strong brands and best-in-class people and organization.

DRI

To view our analyst's original report on Darden Restaurants click here.

Management has not meaningfully invested in the business, to propel growth.

Olive Garden’s last remodel was completed at the end of fiscal year 2001, when Joe Lee held the CEO position and Clarence Otis was the CFO. Management defended the remodels during 2002, although they struggled to increase their alcohol sales, which were supposed to be a benefit of the remodels.

In fiscal 2011, management started early remodeling tests on Olive Garden. Olive Garden has about 400 older RevItalia restaurant models that are in dire need of remodeling. In 2011, they remodeled 35 to test the effectiveness of the prototype. Clarence Otis successfully kicked the remodel can down the road until he met his demise in 2014:

- 2011 Annual Report: “Olive Garden will begin remodeling more than 400 early restaurants to be consistent with the Tuscan Farmhouse design of the restaurants opened in the past six years.”

- 2012 Analyst Meeting 2/23/12: “Olive Garden now testing a remodel program for 430 pre-Tuscan Farmhouse restaurants that were built before March 2000.”

- 3Q13 Earnings call transcript: “Olive Garden is preparing to implement their remodel program in the second half of this fiscal year.”

To date, Olive Garden has done 32 remodels, and is far behind schedule, on a massive remodel project. Clearly, no one wants to remodel the Olive Garden concept because it will be disastrous for earnings.

Management is adamant that an evolutionary approach to remodeling in which they do a smaller number in each stage, while carrying best practices forward is the best approach. We tend to disagree, especially as casual dining is experiencing a slowdown, Olive Garden needs to shock the system and customer perception to drive increased traffic.