Earlier today, maverick Hedgeye Energy analyst Kevin Kaiser hosted a short call on Summit Midstream Partners (SMLP).

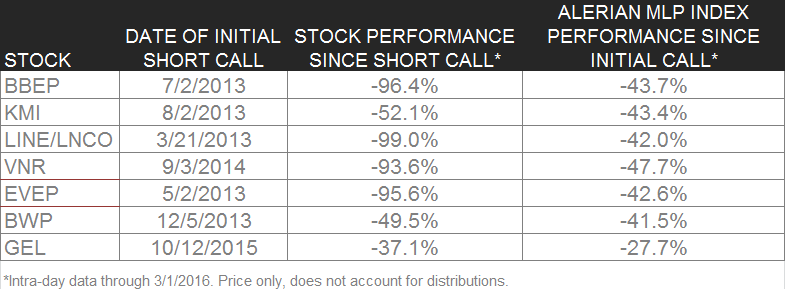

Kaiser was the original bear on MLP stocks, like Kinder Morgan (KMI) and Linn Energy (LINE), while virtually all of the conflicted, sell-side analysts on Wall Street remained bullish. Below is an update from a post of Kaiser's short calls from our original post, "A Cautionary Tale: Energy Analyst Kevin Kaiser's MLP Warning and 8 Short Calls."

As you can see, he nailed it.

Editor's Note: To access Kevin Kaiser's research email sales@hedgeye.com.