Key Takeaway:

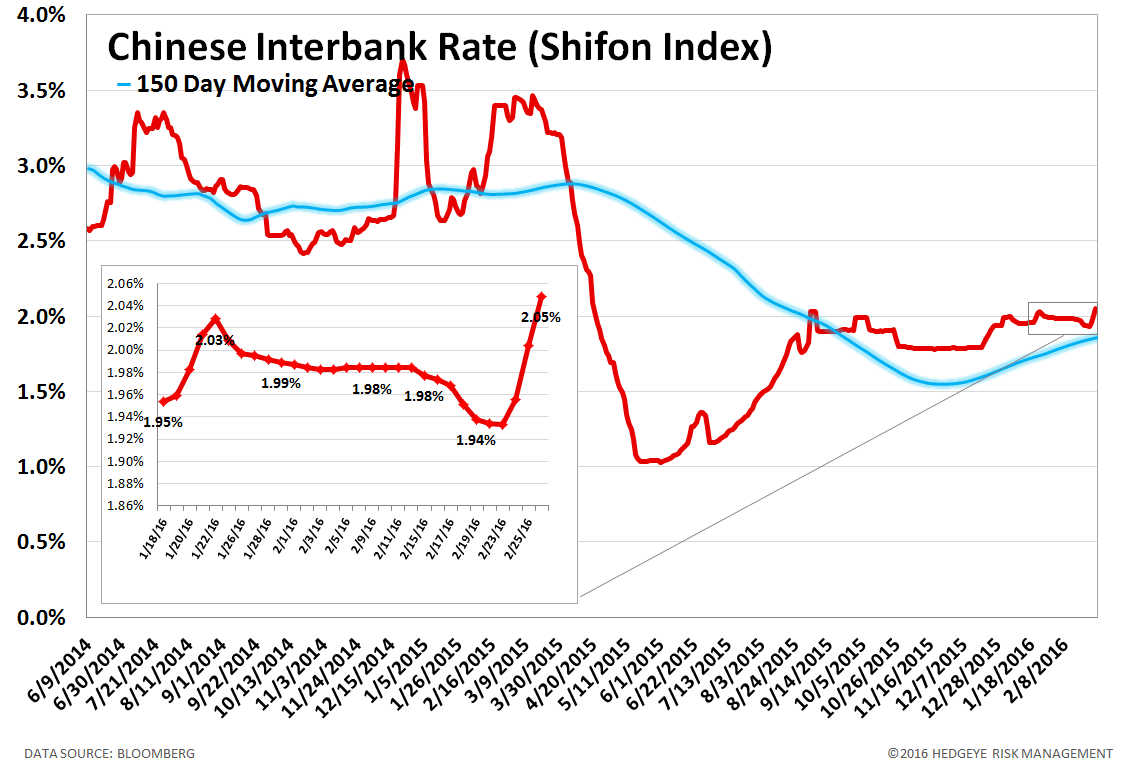

Risk has been in modest retreat for the last two weeks alongside an emergent stabilization in oil in the low $30s and the less bad than feared +1.0% GDP print on Friday. We wouldn't take too much comfort from that as risk in Asia continues to creep higher. The Chinese Interbank Rate, a gauge of systematic stress in the Chinese banking system, notched up by 11 bps week over week to 2.05%, its highest level since April 2015. Additionally, the median CDS spread in Asia widened by 5 bps last week, bringing the M/M change to 11 bps.

Current Ideas:

Financial Risk Monitor Summary

• Short-term(WoW): Positive / 4 of 13 improved / 3 out of 13 worsened / 6 of 13 unchanged

• Intermediate-term(WoW): Negative / 4 of 13 improved / 7 out of 13 worsened / 2 of 13 unchanged

• Long-term(WoW): Negative / 1 of 13 improved / 6 out of 13 worsened / 6 of 13 unchanged

1. U.S. Financial CDS – Swaps tightened almost across the board for US Financials as 4Q15 GDP came in better than expected. The median contract tightened by -9 bps to 100 last week.

Tightened the most WoW: JPM, C, HIG

Widened the most WoW: MMC, CB, XL

Widened the least/ tightened the most WoW: JPM, TRV, LNC

Widened the most MoM: AIG, MMC, PRU

2. European Financial CDS – Swaps were mixed across European banks last week with essentially no W/W change in the median.

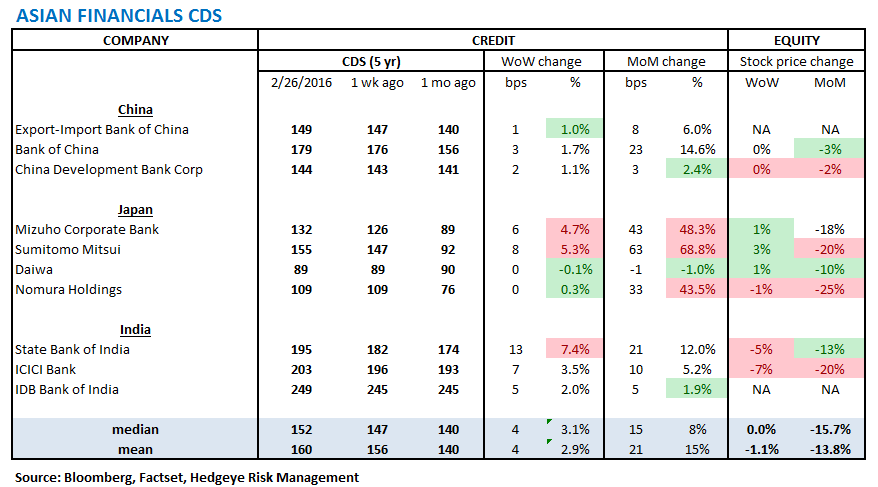

3. Asian Financial CDS – Swaps on Asian banks were flat to wider last week, led by the increase at State Bank of India which widened by +13 bps to 195.

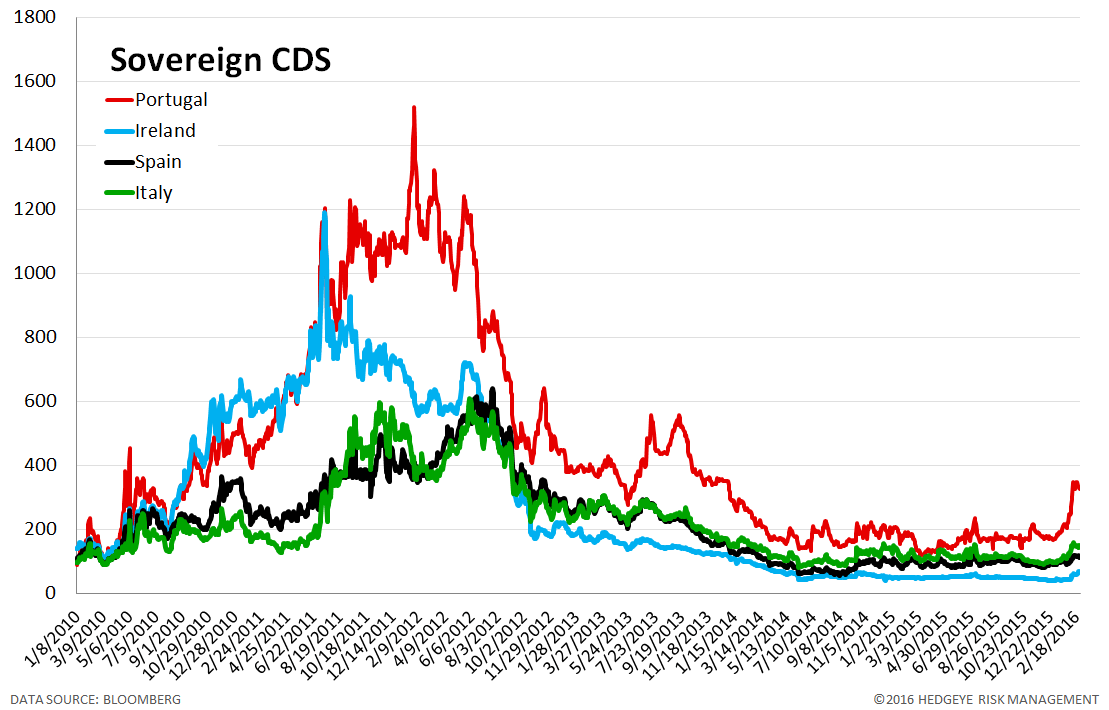

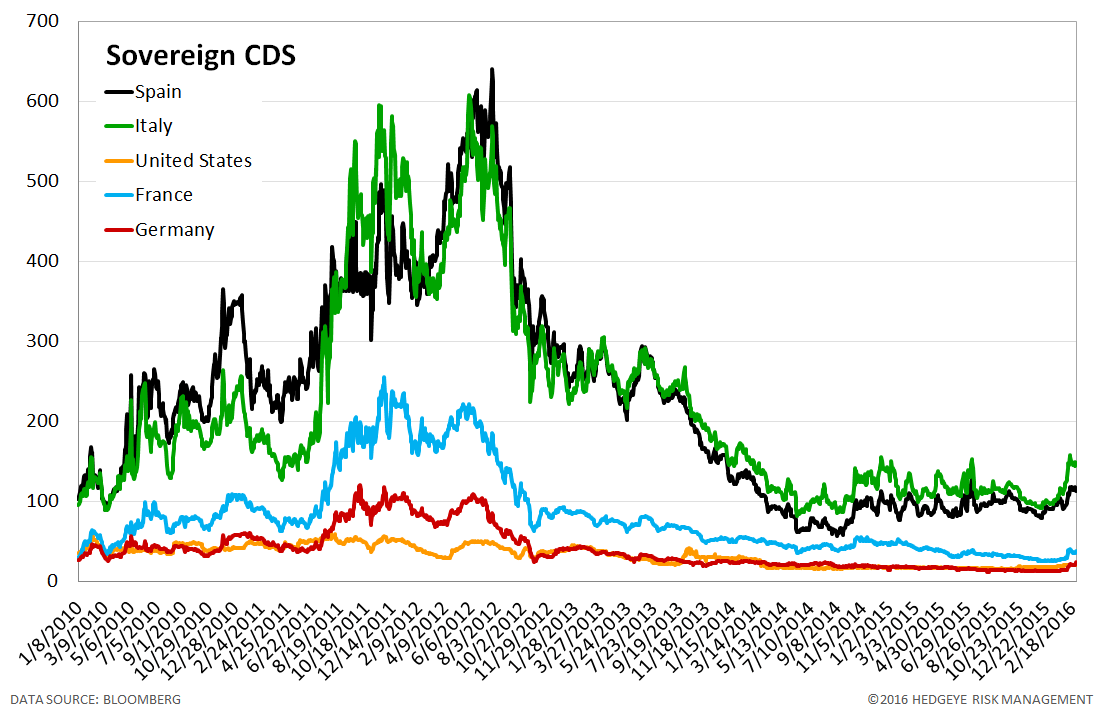

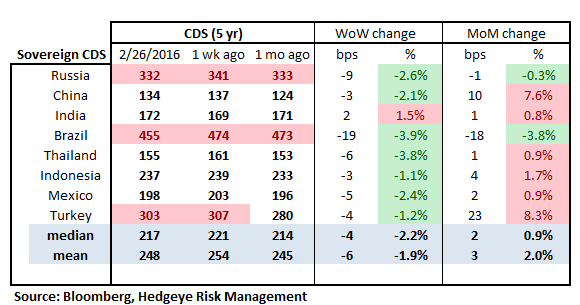

4. Sovereign CDS – Sovereign swaps were mixed last week. On the positive side, Portuguese sovereign swaps tightened the most, by -20 bps to 326. On the negative, Irish swaps widened by +7 bps to 66.

5. Emerging Market Sovereign CDS – Emerging market swaps mostly tightened last week. Brazilian CDS tightened the most, by 19 bps to 455, as the country's central bank reported that Brazil's budget deficit narrowed in January, although the improvement came from one-time revenue sources.

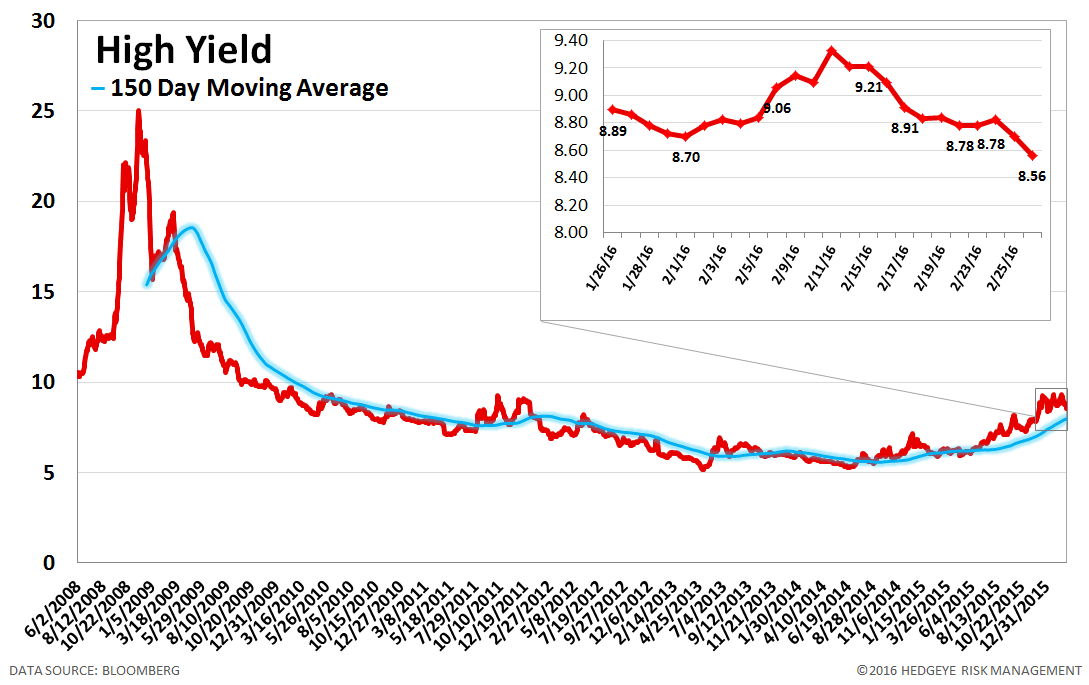

6. High Yield (YTM) Monitor – High Yield rates fell 28 bps last week, ending the week at 8.56% versus 8.84% the prior week.

7. Leveraged Loan Index Monitor – The Leveraged Loan Index rose 7.0 points last week, ending at 1789.

8. TED Spread Monitor – The TED spread was unchanged last week at 32 bps.

9. CRB Commodity Price Index – The CRB index fell -0.5%, ending the week at 162 versus 163 the prior week. As compared with the prior month, commodity prices have decreased -3.0%. We generally regard changes in commodity prices on the margin as having meaningful consumption implications.

10. Euribor-OIS Spread – The Euribor-OIS spread (the difference between the euro interbank lending rate and overnight indexed swaps) measures bank counterparty risk in the Eurozone. The OIS is analogous to the effective Fed Funds rate in the United States. Banks lending at the OIS do not swap principal, so counterparty risk in the OIS is minimal. By contrast, the Euribor rate is the rate offered for unsecured interbank lending. Thus, the spread between the two isolates counterparty risk. The Euribor-OIS spread widened by 1 bps to 15 bps.

11. Chinese Interbank Rate (Shifon Index) – The Shifon Index rose 11 basis points last week, ending the week at 2.05% versus last week’s print of 1.94%. The Shifon Index measures banks’ overnight lending rates to one another, a gauge of systemic stress in the Chinese banking system.

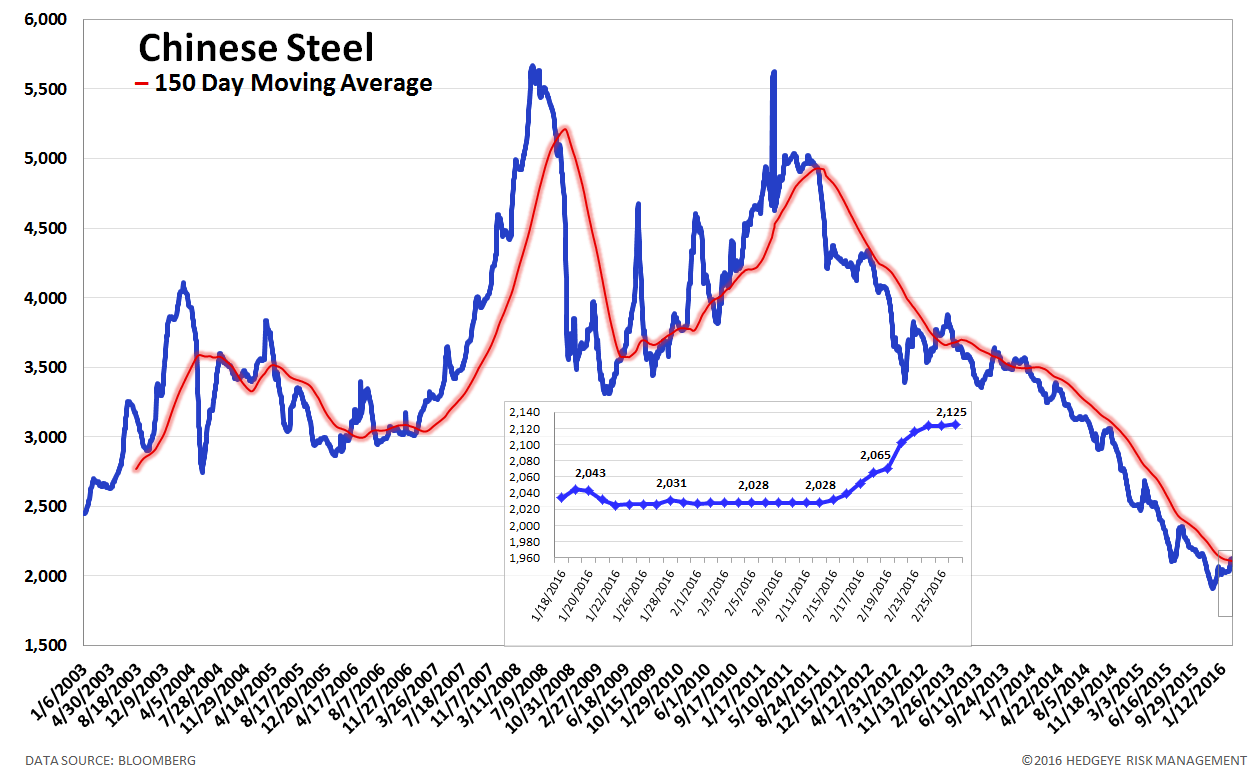

12. Chinese Steel – Steel prices in China rose 2.6% last week, or 54 yuan/ton, to 2125 yuan/ton. We use Chinese steel rebar prices to gauge Chinese construction activity and, by extension, the health of the Chinese economy.

13. 2-10 Spread – Last week the 2-10 spread tightened to 97 bps, -7 bps tighter than a week ago. We track the 2-10 spread as an indicator of bank margin pressure.

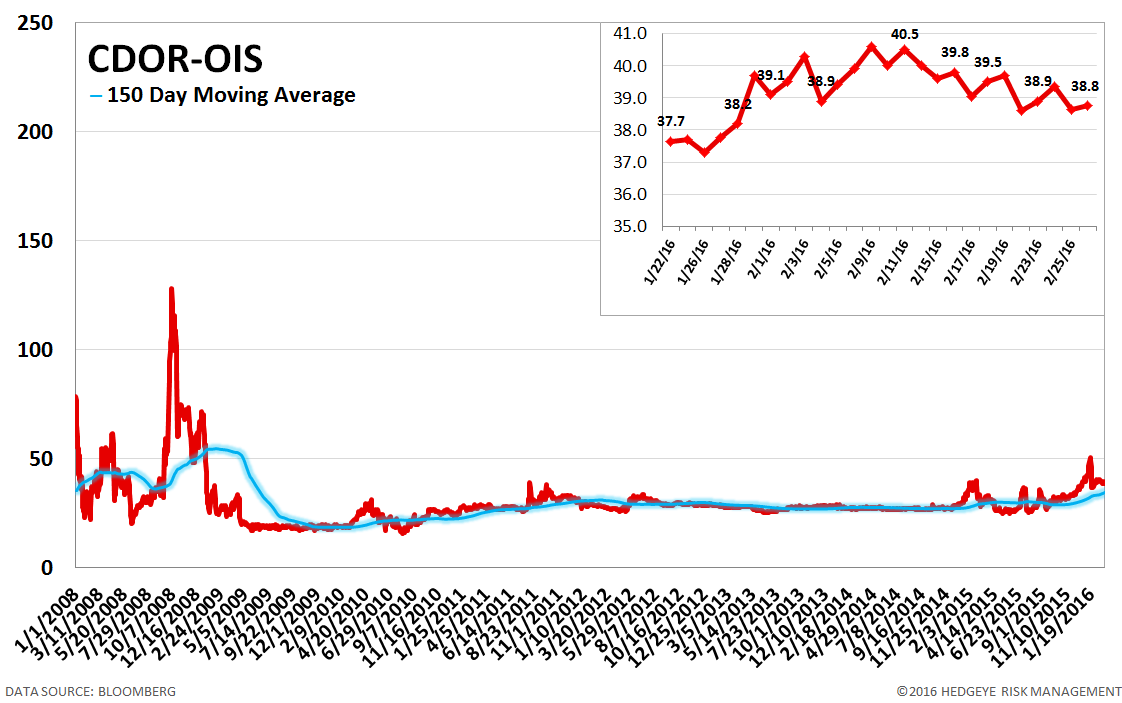

14. CDOR-OIS Spread – The CDOR-OIS spread is the Canadian equivalent of the Euribor-OIS spread. It is the difference between the Canadian interbank lending rate and overnight indexed swaps, and it measures bank counterparty risk in Canada. The CDOR-OIS spread tightened by 1 bps to 39 bps.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT