Sorry. Today's updwardly revised Q4 GDP report from 0.7% to 1.0% is not the auspicious economic harbinger many are purporting it to be.

"Hold on a second," Hedgeye Senior Macro analyst Darius Dale wrote following this morning's revision. "Inventories rip because consumers bought less stuff than was initially estimated and this is POSITIVE for GDP?"

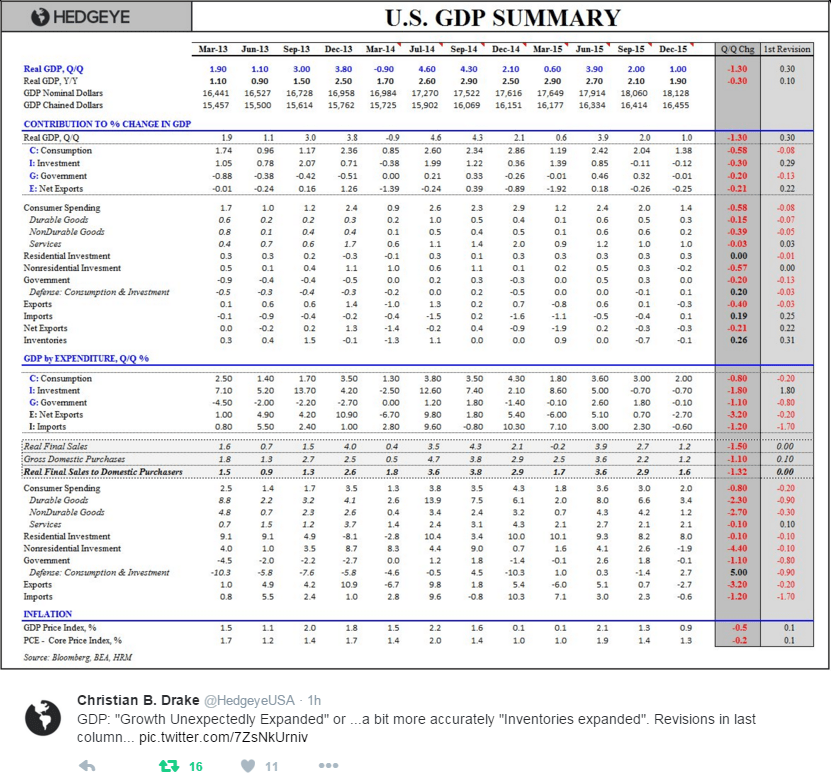

Take a look at the table below from Hedgeye U.S. Macro analyst Christian Drake. As you will see, the modest upward revision to 4th quarter GDP was mostly due to a build in inventories. Also note that consumer spending was revised down.

Not good.

Click image to enlarge.

We're sticking with our U.S. #GrowthSlowing call.