Darius asked this question in passing yesterday when talking about the day’s earnings reports. My answer to that question is ‘No’, but I’m a cynical, crotchety retail analyst with opinions that might not speak for main street America. DD is hardly ‘main street’, but we think that more and more people will ask that question as time goes on – and they’ll probably come to a similar answer. We have that answer represented in our earnings estimates, which – as outlined in the table below – are significantly below consensus. While we’re only looking for a $0.50 miss this year, as our annual numbers march forward, we get to $2.30 by 2019 vs the Street over $6.00. We think KSS will miss again, and again and again – and we think they’ll be a dividend cut along the way. Case in point, it’s cash flow literally got cut by 25% this year, and cash balance was halved. We often get the ‘there’s so much cash’ argument against a short. But never forget that a great cash flow profile in this business could deteriorate faster than a Presidential candidate’s credibility.

In this note, we give out take on KSS’ guidance, and then there’s an overview of our ‘3-Steps to Failure’ thesis on KSS.

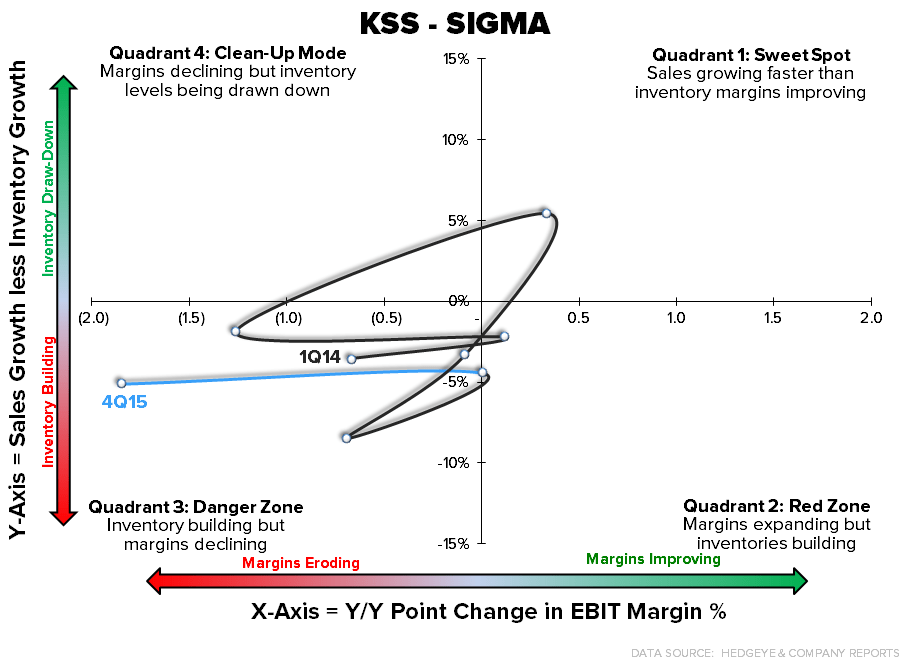

GUIDANCE: Management set more realistic expectations for 2016 then it did last year, which resulted in the 8% annual miss reported yesterday. Our thoughts on the line items KSS guided…

1) Comp, 0-1% - Doable for KSS. The company just comped the comp in the 4th quarter, which is a big feat for KSS. But, comps stay tough from here as KSS goes up against the longest stretch of comparable store sales increases since 2010-11. We’re at the high end of guidance for comps this year (i.e. a whopping 1%) assuming negative LSD in store comps at 20%+ e-comm growth – but that ‘strength’ will come at the expense of GM.

2) Gross margin, +0-20bps – Not going to happen. With guidance for -150bps for 1Q as KSS tries to clean up its inventory position, we have to assume that gross margins in quarters two through four are up 70bps. Inventory is a priority, as it has been for the past couple of years and we aren’t willing to give the company the benefit of the doubt on its ability to control inventory growth AND comp positive. One or the other with KSS, at best. National brand penetration was up 200bps over 2014 and 400bps since ’13 and that comes at an incrementally lower margin. Management talked about a stabilization in the mix shift, but National brands (i.e. Nike, Nike and Nike) have driven the comp over the past year plus. Add on to that e-commerce growth of 20%+ and that equates to a 35-40bps hit in gross margin even assuming a 75bps increase in e-comm profitability.

3) SG&A, 1-2% - Looks low. Key drivers of SG&A growth: wage inflation, credit revenue no longer an incremental offset, and IT spending. All in we get to ~3% growth for the year. Might not seem like much, but this is a company that struggles to comp 1% on its best day.

4) EPS, $4.05-$4.25. To get to the mid-point of guidance we need to see no erosion in the net income base which hasn’t grown in a year since 2011. With a $600mm buyback, at the tail end of an economic cycle. We’re at $3.65.

Credit: Credit leveraged for the year, but we started to see some cracks after year 1 of the Yes2You rewards program. Most notably, credit card applications were down vs. last year. Management chalked that up to an increased emphasis on loyalty, but we think it has more to do with the fact that KSS has already hit 75% of the total customers it could possible attract (see math below). Dipping down the credit ladder is no longer an option, as KSS already did that when it switched its card partner over to Capital One and over the subsequent 5 years took credit as a percent of sales from 50% to 60%+. We see significant risk to this line. To be clear, this one of the major pillars to our short thesis on KSS (see below). KSS could and should see credit income (25% of EBIT) erode without a turn in the credit cycle. Note: even Macy’s is seeing a rise in delinquencies.

Sq. Ft. Growth/Store Closures – These Won’t Be The Last: This is the first meaningful store closures we’ve ever seen at KSS. It makes sense in theory as we’ve seen store productivity (ex-ecomm) fall by 8% over the past 4 years...see chart below. That will continue as e-comm continues to cannibalize the brick and mortar business. At its analyst day, management noted that there were few stores in the portfolio losing money on a cash business, which translates to limited cost savings as more stores are stripped. Though no exact numbers were given on expected sales recapture in neighboring stores and online, we don’t think this is a big opportunity. Macy’s commentary earlier this week on sales recapture wasn’t overly bullish. This is a non-event from where we sit.

(Originally Published on 2/3 After KSS Preannouncement)

KSS | …And This Is Only Stage 1 of 3

This is the 1st Stage of KSS EPS permanently being held below $4.00. Stage 2 goes to $3.25. Stage 3 = $2.50 and dividend cut.

All along we’ve been saying that KSS would never earn $4.00 again. While today’s rather dramatic guide-down will make this premise seem a reality for some doubters, what we find most interesting is that this is only midway through Stage 1 of what we think is a Three Stage process to KSS cutting its dividend. Here’s our thinking…

Stage 1: Weak sales results as a result of the fact that KSS sells less and less of what consumers want to buy. Sounds overly simple – but it’s reality. That flows through to the gross margin line as online sales cannibalize brick and mortar, and come at a gross margin 1000bps below the company average. True SG&A growth becomes apparent as credit income stops going up as newly emphasized non-credit/loyalty shoppers become a bigger mix of the pie due to launch of Yes2You rewards program.

Stage 2: Here’s where credit income (currently about 25% of EBIT) erodes WITHOUT a rollover in the broader credit cycle. The company’s much-touted (but ultimately fatally flawed) Yes2You rewards plan cannibalizes credit income as shoppers can move to a loyalty program that offers similar rewards to the branded credit card but gives the consumers the opportunity to get 2x the points. Once at KSS and once on a National Credit card. That takes SG&A growth, which has been artificially suppressed as credit sales grew from 50% to 60%+ of total sales over a 5 year time period, from a run rate of 1% to 3%-4%. For a company that comps 1% in a good quarter, this is incredibly meaningful.

Stage 3: This is the doomsday scenario, and within the realm of possibility as the credit cycle rolls. On top of the self-inflicted pain we see in Stage 2, we see consumer spending dry up (sales weaken – down 5-10%), gross profit margins are down 2-3 points due to excess inventory, SG&A grows in the high single digits due to credit income (which is booked as an offset to SG&A) eroding, and EPS falls to $2.00-$2.50. Look at any data stream on the credit cycle and you will see that delinquencies and charge-offs are at pre-recession levels. Translate that to KSS, and it means that the credit portfolio is currently at its most profitable rate. Because the company shares in the risk/reward with its partner COF, any weakening in the consumer credit cycle exacerbates the problems brought on by Yes2You cannibalization and puts 25% of EBIT and half of the current FCF at risk. The result, cash flow dries up and by our math, cuts its dividend within 12-months.

Other Notables on The Preannouncement

The comp in this quarter missed, and believe it or not, the comps from here get much more difficult. This pre-announced $0.30 (7%) earnings miss for a fiscal year is monstrous. The last time a company with the cap and sales base that KSS owned (pre-blowup) missed at this magnitude in a fiscal year was back in 2012 at JCP under RonJon. Prior to that, we have to go all the way back to 2003 when TGT and KSS printed a miss of 11% and 8%, respectively.

This is now the 5th straight quarter of positive SSS comps for a company that hasn’t put a string like this together since 3Q10 – 3Q11. By our math, given that e-commerce sales grew at 30%, brick and mortar comps were down 4% in the quarter. Gross margins were down to the magnitude of 100bps+ assuming SG&A growth of 3-4%.