"When you expect things to happen...strangely enough they happen." - J.P. Morgan

Most of the JP Morgan Investor Day this week was backward looking with the bulk of the presentation spent on an annual recap of the Corporate and Investment Bank (CIB) in 2015. The most relevant data however was the simple reference to running 1Q16 activity trends which are down -25% year-over-year. While there was no deconstruction of the drivers of this slack, our data suggests a 30-40% decline in underwriting, with a negative 5-10% start for M&A (described as "holding well" by the CIB Head). JP Morgan matters with top 3 share across the board in capital markets.

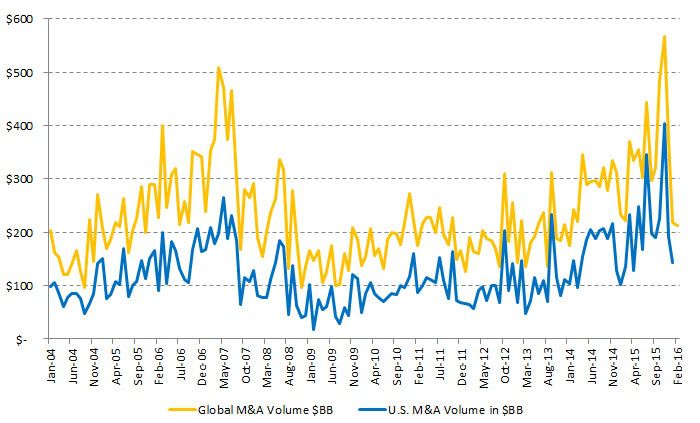

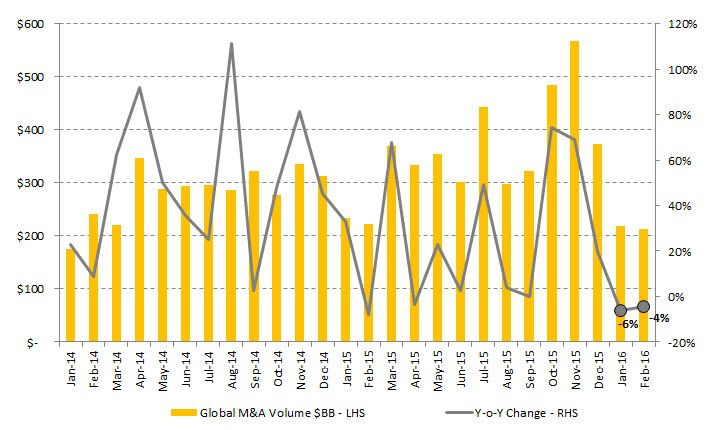

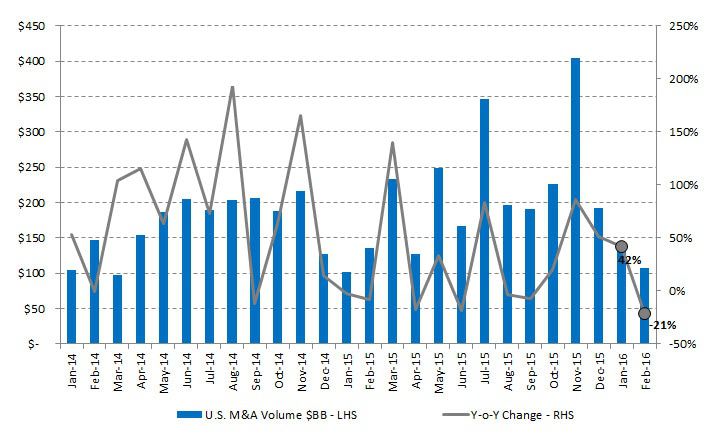

Global M&A announcements have started down mid-single digits in January and February with U.S. announcements more volatile having putting up a solid January, up 42% year-over-year, with a forming -20% decline for February. The across cycle look at merger activity shows the new 2015 zenith having taken out the '07 highs, with even the slight decline to start 2016 looking like a massive slough off. We think this slow start to the year turns into an intermediate term trend and that the M&A advisory group will be comping negatively throughout 2016. The main culprit at his juncture is the backup of corporate credit costs which are maintaining levels, some 100 basis points higher across Moody's most widely referenced indices. Historically, M&A has comped down by -20% with a 100 basis point back up in credit, which implies an M&A market just starting a more substantial decline.

On the asset management side, headwinds persist with a stubbornly high U.S. dollar and risk aversion for EM assets. The Chinese Yuan devaluation now appears to be driving the depreciation in the MSCI Emerging Markets index and with the outlook for the Chinese currency weak at best considering capital flight and slowing growth, the situation warrants caution.

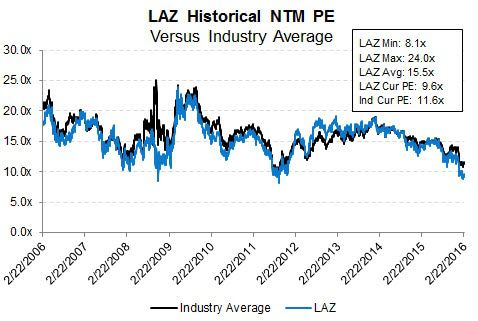

Like most cyclical stocks, Lazard "looks" cheapest at market tops as its earning downturn is just getting started versus at market bottoms when the company is underearning and shares "look" expensive (but they are actually great early cycle longs). We have earnings flat at $2.80 for 2016 and 2017 which we capitalize at 8-9x for a fair value of $25. However in a 1 Emerging Market type downcycle, Lazard asset management with ~50% of its asset-under-managments in EM credit and equity will cause LAZ stock to overcorrect and spit off more downside (substituting current day China for Thailand in '97 in running out of FX reserves to support its currency and plugging in Venezuela or the Ukranine for Russia's '98 default).

The update on 1Q16 trends from JP Morgan matters as a top 3 player in most business lines in capital markets:

The flattish start to global M&A for 2016 looks like a massive decline being that M&A activity put in its high water mark in the middle of last year. In addition to "comping the comp" as we move further into the year, M&A activity will be battling volatility and the fundamental change in corporate credit costs:

U.S. activity had a solid January but is putting in a slump in February. Historically, U.S. activity is 60% of global announcements.:

The inflection in corporate credit costs hasn't normalized which pressures funding costs and M&A synergies:

And the year-over-year change in credit costs (inverted - left scale) does drive the growth or decay of M&A volume:

Every 100 bps of credit cost expansion has historically depressed M&A by -20%. Currently, the four quarter moving average of corporate credit has backed up by 25 bps, essentially confirming the -4-6% start for global M&A:

And although the firm will have a strong 1Q16 report (the company advised on 6 of the 10 largest deals in 2015 but only closed 1 of them during the year), the stock discounts the revenue environment 3 quarters ahead of time:

Lazard stock is a great early cycle performer but kicks off decidedly negative returns at the end of cycle:

The rising volatility environment is not good for cyclicals as the VIX (inverted right scale) historically pushes the stock down:

On the asset management side, non-local Lazard Asset Management strategies regress closely to EM markets which means their exposure is understated:

And the debasement of the Chinese Yuan (inverted scale) is down driving EM market returns:

The last EM down cycle created redemption rates of between ~ negative 2-5% in 2002-2004 versus the +2% organic growth in LAZ asset management to finish 2016:

We hear alot from investors that the stock "is as cheap as its ever been" however like a true cyclical, the best time to buy shares is when it is underearning early in the cycle (note 20x LAZ earnings multiple in 2009-2010). LAZ is overearning currently coming out of the M&A boom of 2014-2015:

LAZ - Hiring in Restructuring, Chairman Bullish From Davos

LAZ - Value Trap - Best Ideas BlackBook

Please let us know of questions,

Jonathan Casteleyn, CFA, CMT

Joshua Steiner, CFA