Key Takeaway:

Ten days ago our Washington Policy Group, Potomac Research, hosted a call with former Energy Secretary Spencer Abraham called OPEC Cuts = Mirage. The point of the call was that investors should expect, but shouldn't be headfaked by, comments from various OPEC countries in the weeks/months ahead aimed at shoring up oil prices. Secretary Abraham's message was clear: the Saudis believe their policies are winning and investors should continue to expect energy price weakness over the intermediate term.

We view the recent bounce in oil within that context, and would be sellers of strength.

Current Ideas:

Financial Risk Monitor Summary

• Short-term(WoW): Positive / 5 of 13 improved / 2 out of 13 worsened / 6 of 13 unchanged

• Intermediate-term(WoW): Negative / 4 of 13 improved / 7 out of 13 worsened / 2 of 13 unchanged

• Long-term(WoW): Negative / 1 of 13 improved / 6 out of 13 worsened / 6 of 13 unchanged

1. U.S. Financial CDS – Swaps tightened for 12 out of 27 domestic financial institutions. The median CDS tightened by 17 bps to 126 as fear in the market eased over the short term. However, month over month, CDS spreads remain 39 bps wider.

Tightened the most WoW: MET, PRU, HIG

Widened the most WoW: COF, SLM, ALL

Widened the least WoW: MMC, AON, TRV

Widened the most MoM: AIG, PRU, MET

2. European Financial CDS – Swaps mostly tightened in Europe last week. Following the agreement between Saudi Arabia, Russia, Qatar, and Venezuela not to increase oil production, Russia's Sberbank CDS experienced one of the largest moves in Europe, tightening by -105 bps to 386.

3. Asian Financial CDS – Asian bank swaps mostly tightened last week as global risk perception eased. The median CDS tightened by 27 bps to 147.

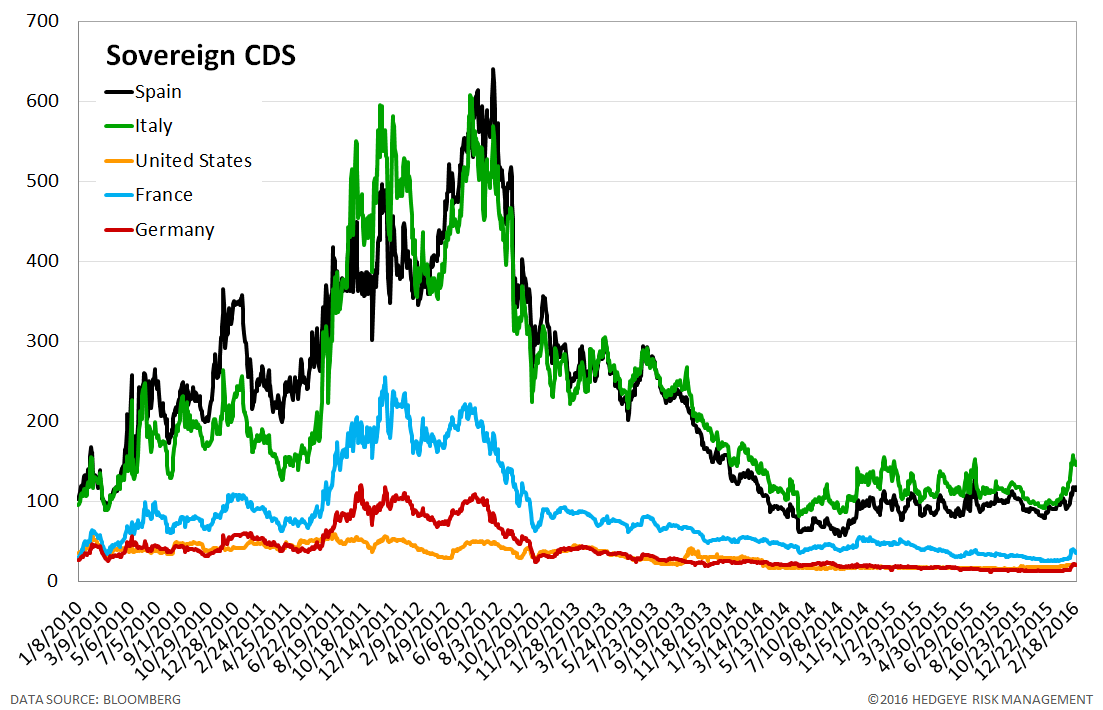

4. Sovereign CDS – Sovereign Swaps mostly tightened over last week. Italian swaps tightened the most, by 6 bps to 149.

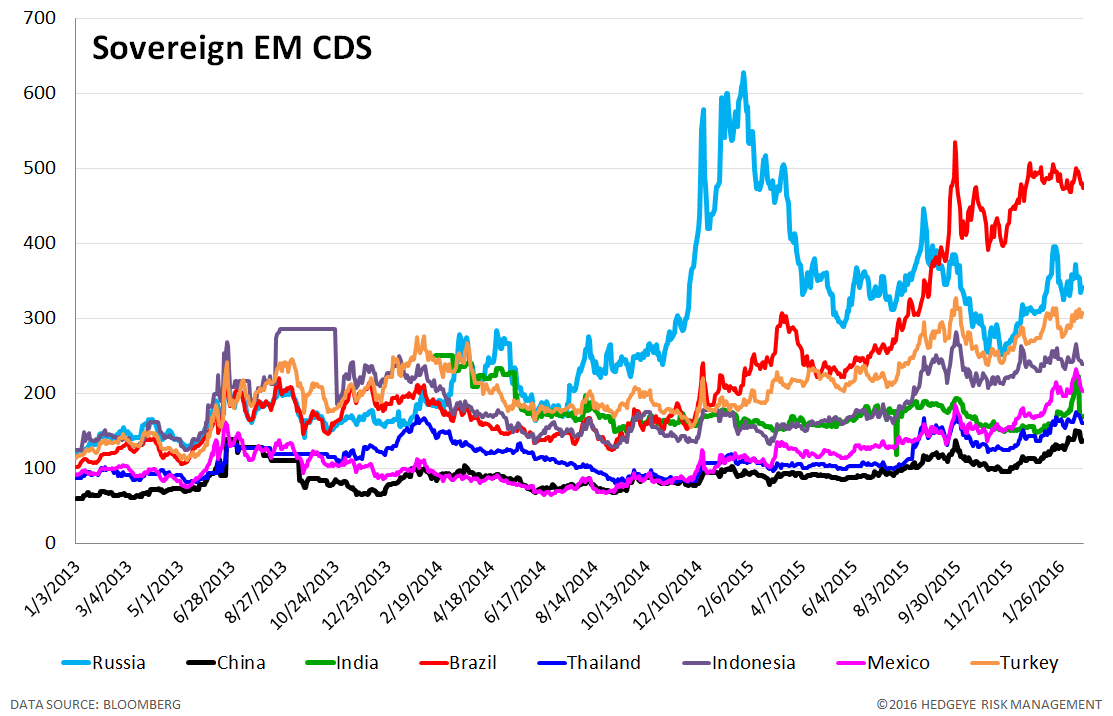

5. Emerging Market Sovereign CDS – Emerging market swaps mostly tightened last week. Indian swaps tightened the most, by -53 bps to 169.

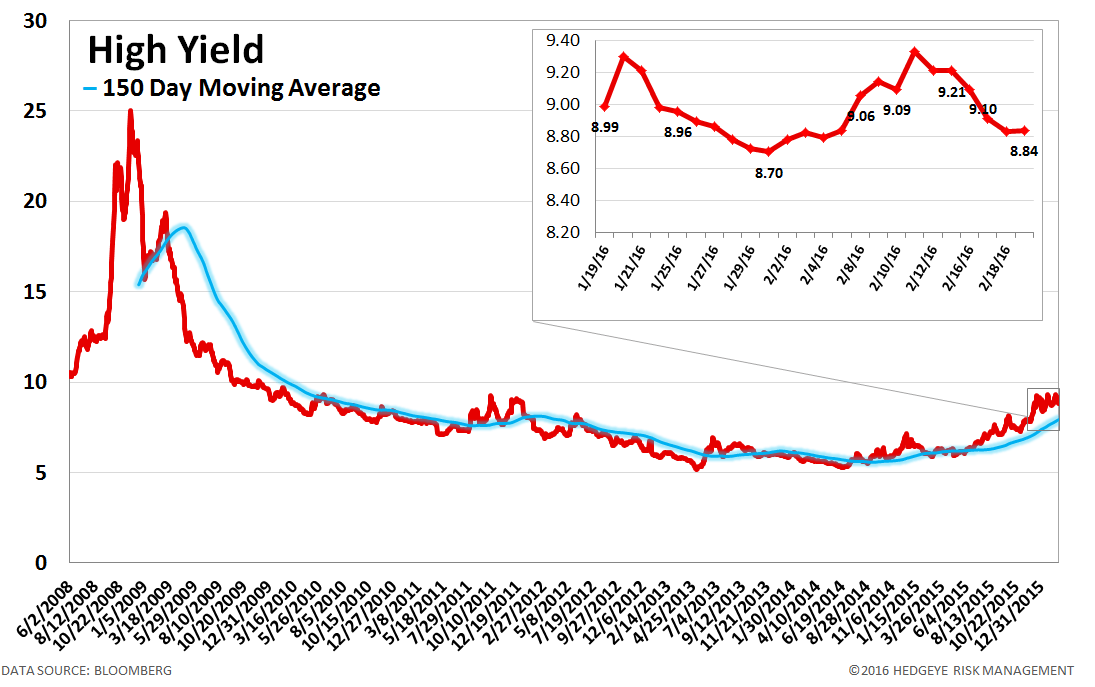

6. High Yield (YTM) Monitor – High Yield rates fell 37 bps last week, ending the week at 8.84% versus 9.21% the prior week.

7. Leveraged Loan Index Monitor – The Leveraged Loan Index rose 4.0 points last week, ending at 1782.

8. TED Spread Monitor – The TED spread fell 1 basis point last week, ending the week at 33 bps this week versus last week’s print of 34 bps.

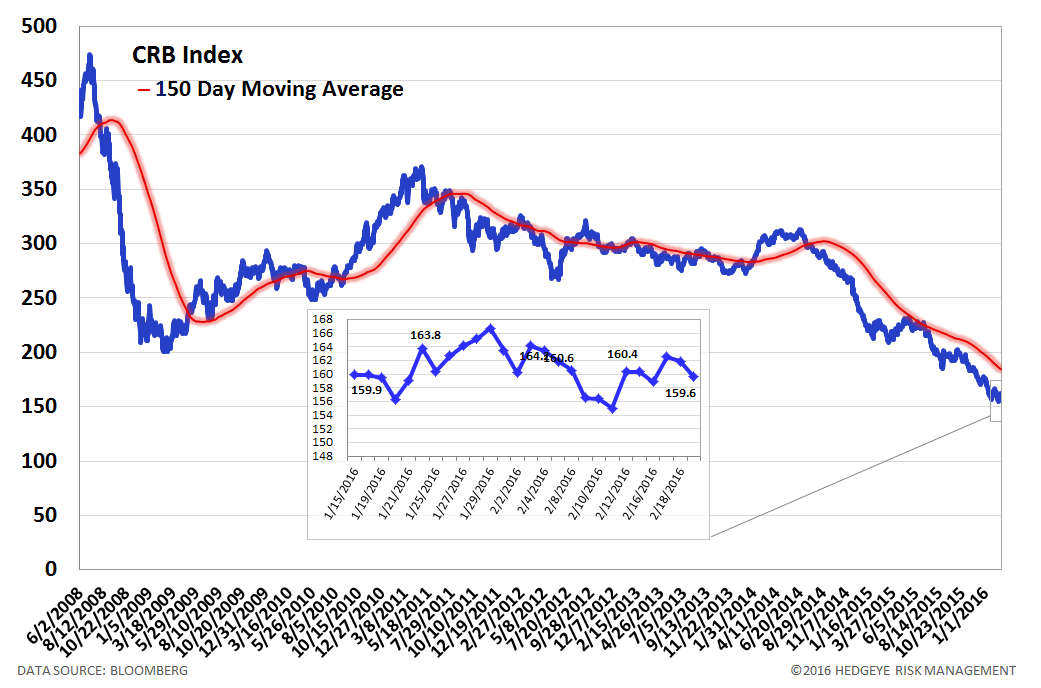

9. CRB Commodity Price Index – The CRB index rose 2.1%, ending the week at 160 versus 156 the prior week. As compared with the prior month, commodity prices have decreased -2.5%. We generally regard changes in commodity prices on the margin as having meaningful consumption implications.

10. Euribor-OIS Spread – The Euribor-OIS spread (the difference between the euro interbank lending rate and overnight indexed swaps) measures bank counterparty risk in the Eurozone. The OIS is analogous to the effective Fed Funds rate in the United States. Banks lending at the OIS do not swap principal, so counterparty risk in the OIS is minimal. By contrast, the Euribor rate is the rate offered for unsecured interbank lending. Thus, the spread between the two isolates counterparty risk. The Euribor-OIS spread widened by 1 bps to 15 bps.

11. Chinese Interbank Rate (Shifon Index) – The Shifon Index fell 5 basis points last week, ending the week at 1.94% versus last week’s print of 1.98%. The Shifon Index measures banks’ overnight lending rates to one another, a gauge of systemic stress in the Chinese banking system.

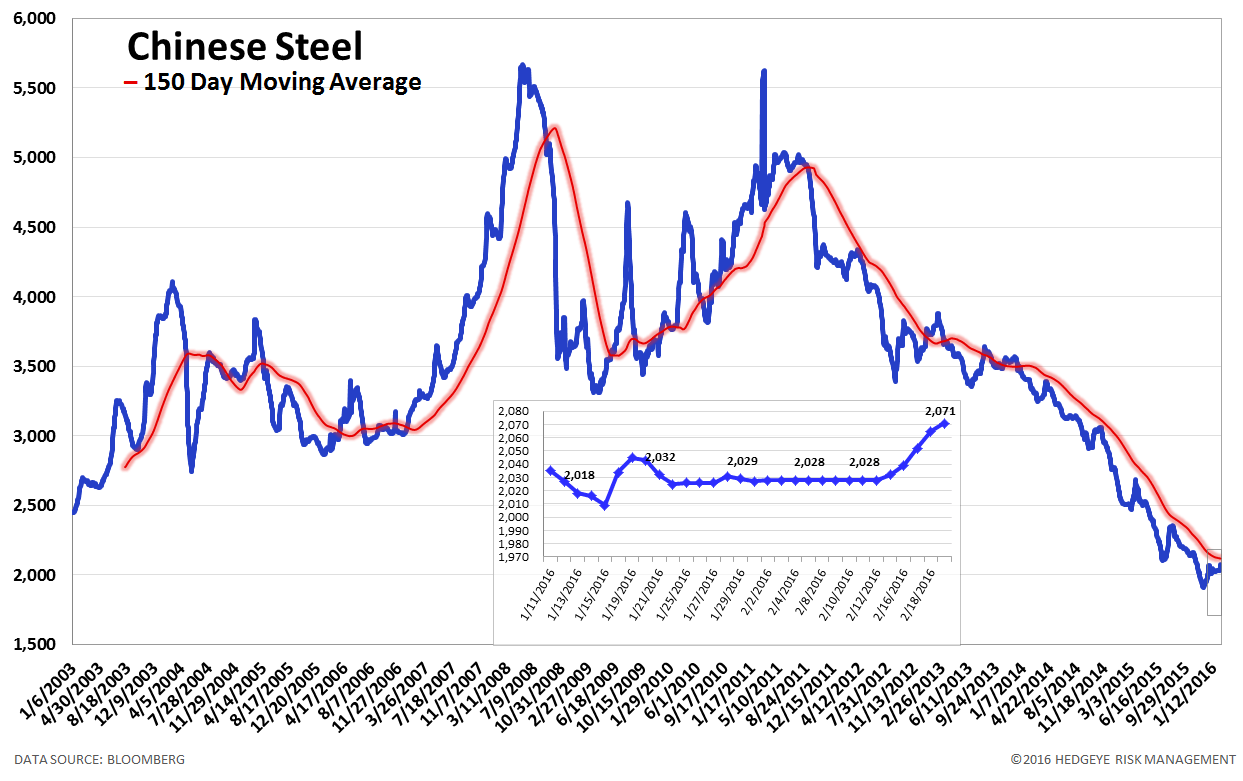

12. Chinese Steel – Steel prices in China rose 2.1% last week, or 43 yuan/ton, to 2071 yuan/ton. We use Chinese steel rebar prices to gauge Chinese construction activity and, by extension, the health of the Chinese economy.

13. 2-10 Spread – Last week the 2-10 spread was flat at 104 bps. We track the 2-10 spread as an indicator of bank margin pressure.

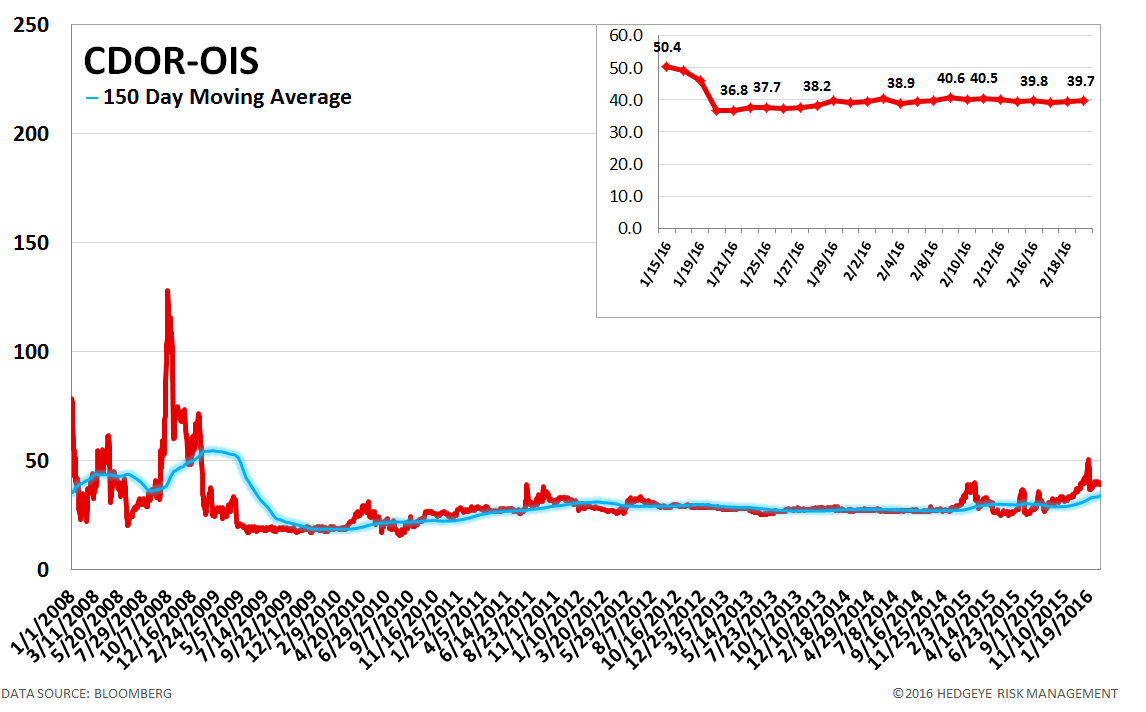

14. CDOR-OIS Spread – The CDOR-OIS spread is the Canadian equivalent of the Euribor-OIS spread. It is the difference between the Canadian interbank lending rate and overnight indexed swaps, and it measures bank counterparty risk in Canada. The CDOR-OIS spread was unchanged at 40 bps.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT