Below, we provide rebuttals we have heard this week to our short case. If you missed the call and would like the slides, replay, or EQM model/data set, please ping us back and we can send them along.

Common Rebuttals

Insider Buying Not Positive, 1 For 2 Match Program Perquisite: Every ATU long we spoke to pointed at recent insider share purchases as a bullish signal. It is true that insiders have purchased stunning ~400,000 shares since October, and that the buys attracted media headlines that helped push ATU shares higher. What many seem not to have noticed was that ATU’s proxy included a provision to incentivize insider purchases. The Matching Restricted Stock Grant Program matches insider purchases in October, December, and March with one share of restricted stock for every two shares bought by the senior executives. The program doesn’t appear to extend to all employees, and seems designed to create promotional excitement about insider buying.

Sum Of Parts Wrong Framework: Prior to presenting, we reviewed sell side reports on Enerpac suggesting that such a quality franchise can sell for a mid-teens EBITDA multiple. In those reports, ATU is cheap because Enerpac is worth a good chunk of ATU’s full enterprise value. There are many problems with this rationale. First, Enerpac can’t be sold without violating debt covenants, by our read. Second, a sale of Enerpac would generate significant tax liabilities. Third, as we understand it, Enerpac is not neatly separable from its intercompany relationships inside ATU (e.g. Hydratight). A sum-of-the-parts methodology only has substance insofar as it reflects a potential economic reality. Most critically, we don’t think a buyer would pay such a big multiple for a company with contracting margins and core sales falling at a 9% rate. Many key Enerpac end-markets are collapsing (e.g. mining, shipbuilding, oil & gas). We are pretty sure a buyer would have access to newspapers. In a sense, our thesis is that the valuation of Enerpac and other ATU businesses has declined and will continue to do so. Most peaking cyclicals seem like premium, highly regarded franchises at peak.

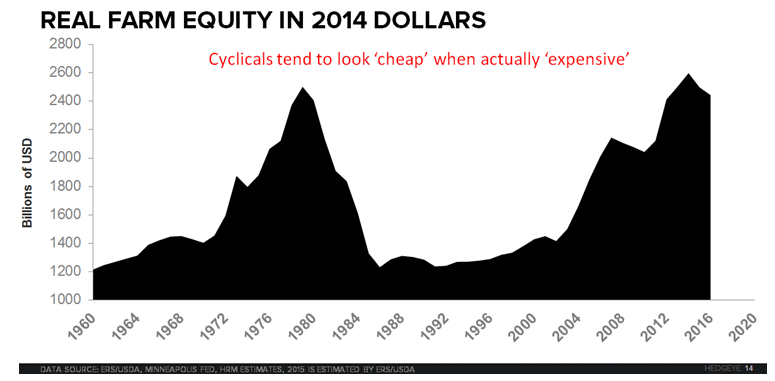

ATU Doesn’t Deserve A High Multiple Of Trough Results: Multiples of earnings, EBITDA, and even sales are a truly horrible valuation approach for cyclicals. Even though we keep writing things like “we are pretty sure that is covered in the CFA materials”, the sell side and investors continue to apply P/Es and EBITDA multiples on “mid-cycle” estimates (or peak or trough). Companies typically spend little time at ‘mid-cycle’ results, and cyclical declines can last for decades in resources capital equipment. See how well P/Es worked for CAT and DE from 1. We typically develop alternative measures in understanding in long cycles, and prefer to use a DCF to make the cycle assumptions explicit. As a current non-ATU example, look at DE’s P/E and decide if it is relevant in the event of a large decline in real farmer equity. ATU and other resource-related capital equipment companies are likely value traps that will look cheap while continually underperforming.

Commodity Capex Bubble Popped, Like Expecting A Dot-Com Recovery In 2001: Many holders think that oil & gas and other commodity markets have been suppressed in the last couple of years, and will recover. We do not think that is accurate. The bubble in commodity-related capital spending peaked out a couple of years ago, and has been deflating toward more normal levels. We don’t think this is the trough. Rather, we believe commodity related capital spending is returning to normal levels, and is not ‘suppressed’ below them.

ATU Is Exposed To Commodity-Related Capital Equipment: A couple of people insisted that infrastructure and general industrial were the ATU exposures that really mattered. We are not sure this point is up for debate, since ATU provides its market exposures. ATU’s relative share price performance tracks CRB and Crude extremely well since the company pivoted to resources. The industrial segment core revenue growth (below) similarly looks like many other resource-related capital equipment companies. We don’t see a reason to doubt what the company itself has provided.

HIGHLIGHTS

- ATU Chose… Poorly: Management shifted portfolio toward resources and repurchased share near the cycle peak. We estimate that well over half of ATU’s sales are exposed to resource-related capital equipment markets (e.g. Oil & Gas, Shipbuilding, Rail, Mining, and Ag).

- Not-So-Light-Assembly, MRO Tools: When looking at operating metrics such as Revenue per Employee and Revenuer per Square Foot, ATU’s metrics suggest it is more of a manufacturer than a light assembly and sourcing company as prominently noted by consensus and management. ATU is likely to get hit on the downside due to their leverage to fixed costs, in our view. We also expect MRO tools to behave like other categories of capital equipment, as investment should be tied to fleet/equipment growth.

- Industrial Segment Won’t See It Coming: Management’s lack of visibility should be a concern for longs. Destocking and slower resource activity may impact this profit driver.

- Energy A Mixed Bag: Interestingly, Energy margins have declined during the boom suggesting their market position may be weakening. In the second half of 2016, comps will get tougher.

- Value Trap: We expect shares of ATU to look ‘cheap’ on multiples as it underperforms.

- Catalysts:

- Estimates to ratchet lower amid a weak demand environment.

- New CEO to lower the bar and drop, what the street calls, a “reachable” FY2018 target.

- Book-to-Bill to drop

- More business impairments like