Our FHQ (Friday Housing Quant) tables present the state of the publicly traded Housing complex in a simple, quantitative format that takes ~60 seconds to consume.

Takeaways:

-

Housing Macro | “If someone were to rent your home today, how much do you think it would rent for monthly, unfurnished and without utilities?” Recall, that perfectly subjective question from the BLS - at a ~32% weighting in the Index - anchors the CPI report and the Fed’s view of Inflation’s reality. Shelter inflation made a higher high in the January data released this morning, accelerating to +3.2% YoY and again buttressed muted pricing growth across the balance of services and further negative growth in core goods pricing. Rising rent costs flowing through to both Headline and Core CPI growth are supportive of the Fed’s inflation target and companies directly levered to rent inflation but the gains largely represent excess growth in a key consumer cost center a drag on other discretionary and housing related consumption.

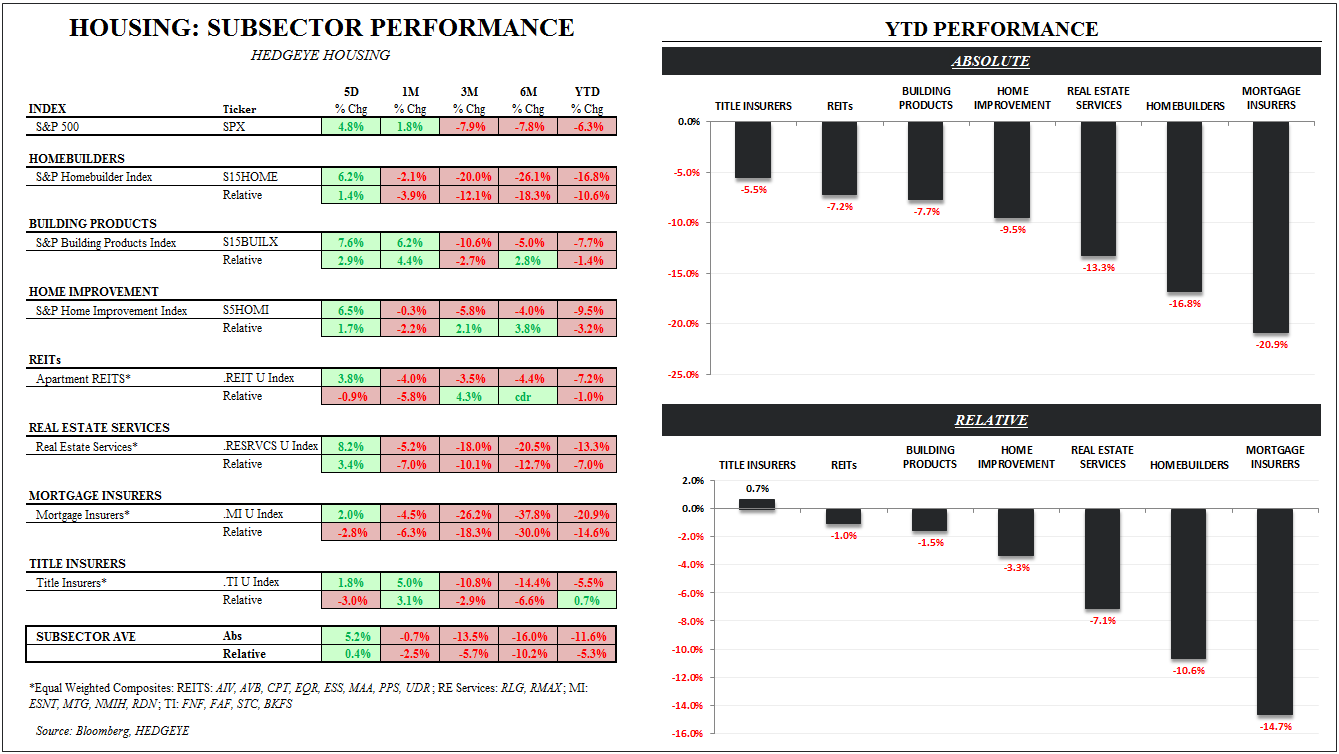

- Performance Roundup: Housing stocks have posted YTD losses roughly double that of the broader market. While the S&P 500 is down 6.3% YTD, the average Housing stock has lost 11.6%: Title Insurance (-5.5%), REITs (-7.2%), Building Products (-7.7%), Home Improvement (-9.5%), RE Services (-13.3%), Homebuilders (-16.8%) and Mortgage Insurance (-20.9%). The only categories to roughly keep pace with the market are Title (+0.7% relative) and REITs (-1.0% relative). Among homebuilders, DR Horton is down 22% YTD, Lennar is down 18%, Toll Brothers is down 24.7%. NVR, the most defensive of the builders, is down 3.9%. Beazer, the worst of the bunch, has shed 40.3% YTD.

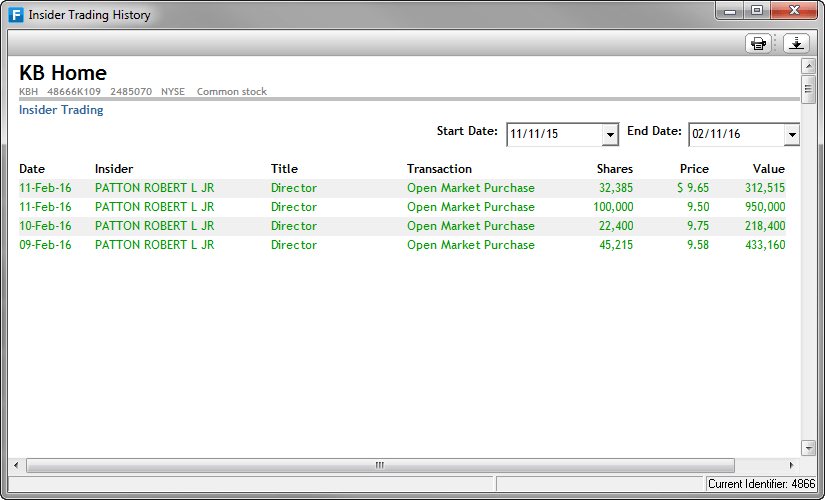

- Insider Buying: Insider buying has been heavy in the last few weeks. As we show in the tables at the end of this note, insiders stepped up to buy shares at BZH, KBH, TMHC, and PHM. Interestingly, while at PHM and KBH there was just a single buyer, at TMHC there were 5 different buyers and at BZH there were 9 different buyers.

- Short Interest: Meanwhile, alongside the most insider buying, the largest increase in short interest in the last two weeks was at KBH (+958 bps), HOV (+415 bps) and CAA (+355 bps). The three companies seeing the largest declines were LEN, NVR and MDC.

Politician Promises / Housing Policy Update:

At least one of the candidates has weighed in with their plan for US Housing reform. Secretary Clinton recently unveiled a plan to help jumpstart housing in economically depressed areas by, among other things, offering up to $10,000 in downpayment matching for select first time homebuyers. While the plan would largely rely on Congress for implementation, here are the provisions as described.

- Match up to $10,000 in down payments for home-buyers earning less than their neighborhood's median income.

- Increase funding and loosen lending requirements for borrowers who go through housing counseling programs.

- Push government agencies to use new ways to assess borrowers' creditworthiness.

- Give agencies 90 days to clarify their requirements for backing loans so that lenders will know how to offer more mortgages without violating new rules.

- Increase the number of affordable rental properties and offer more low-income housing tax credits in neighborhoods where there are shortages.

- Offer more funding to local governments that build affordable housing in neighborhoods with better schools and more jobs.

Joshua Steiner, CFA

Christian B. Drake