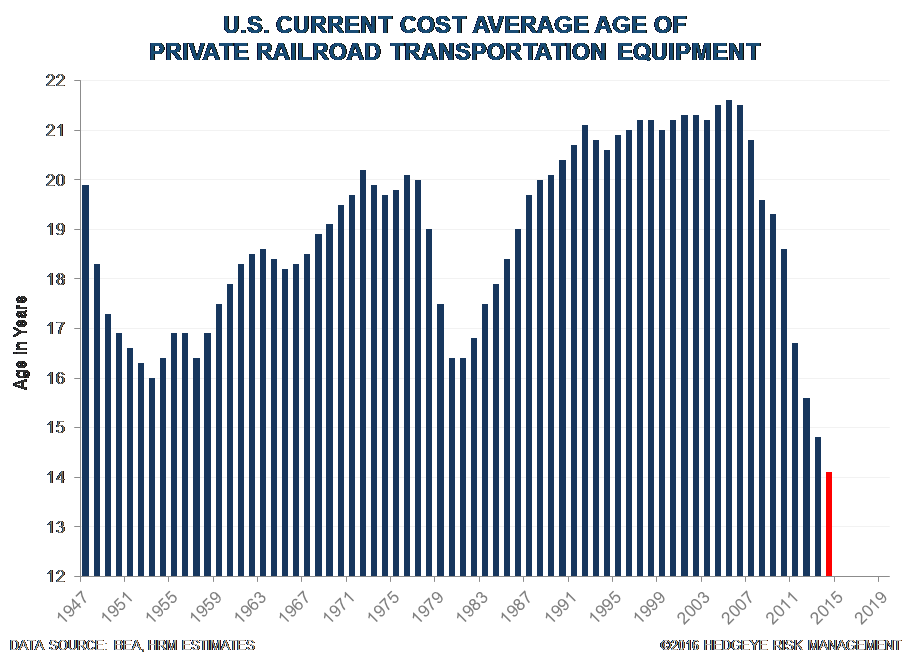

Upshot: The internals of today’s report from WAB continue to point to 2016 EPS well below $4.00. While we need the 10-K for a proper analysis given WAB’s skimpy disclosure, the implied orders, aftermarket sales, and PTC trends look pretty negative to us. The big picture of rail equipment capital spending rolling over from a significant long-term up cycle remains intact.

Overview

We don’t think that the 2016 guide from WAB makes sense, beyond what we expect is management’s desire to see a higher share price to appease a no doubt disgruntled Faiveley family. The internals in the 4Q 2015 report are poor, with deterioration in non-PTC aftermarket sales, a book-to-bill below 1, and a sizeable drop in Freight segment backlog. With NAFTA freight rail traffic down 5% so far this year, 2016 guidance based on “flat” 2016 rail traffic is likely both back end loaded and not credible. The expectation of flat revenue in the Freight segment is also not particularly reasonable given a book-to-bill at around 0.80, peaking PTC sales, weak international markets, and sizeable expected declines in rail car & locomotive deliveries. While it is possible that further draws on backlogged orders, large share repurchases, and incremental acquisitions might get WAB to guidance, markets are unlikely to care. The freight rail market is entering a long downcycle, in our view, and WAB’s changed behavior serves as confirmation for us. Given the skimpy disclosure WAB provides, we will need the 10-K to really understand the results.

Ping us back if you would like to see our updated EQM model/data sets, or recent Black Book.

Backlogs & Book-to-Bill

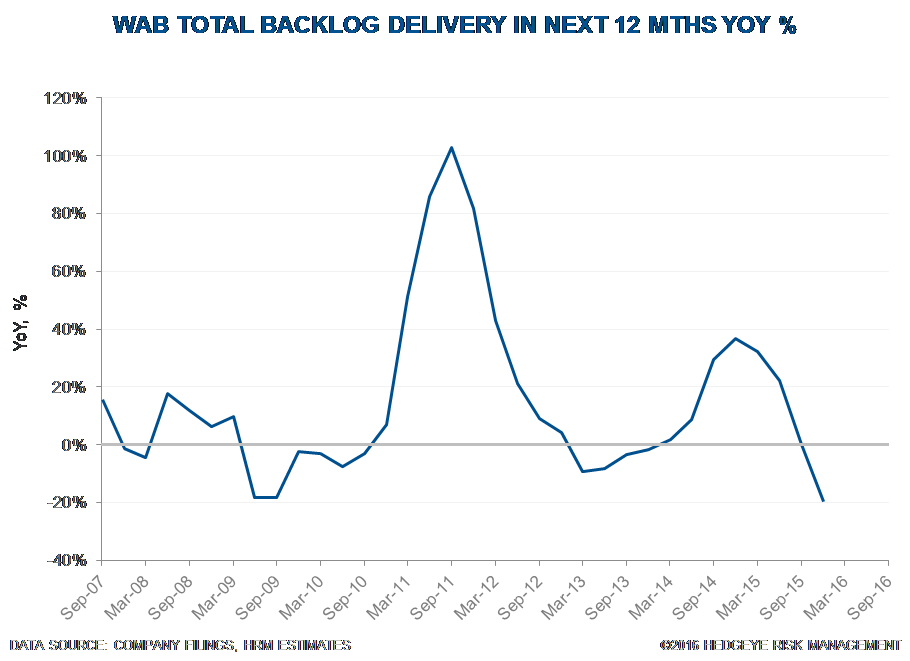

Freight Segment: The Freight book-to-bill came in just under 0.80, as backlog dropped meaningfully. That is not a positive indicator for forward revenue growth, and suggests that guidance for flat revenue in 2016 is likely to be too optimistic. That low book-to-bill is for 4Q 2015, before the anticipated 25% decline in freight car deliveries and 5% decline in locomotive deliveries. The next 12 month Freight backlog dropped 31% year-over-year, which also makes the expectation of flat 2016 Freight revenue unrealistic – at least on an organic basis.

Transit Segment: While the Transit book-to-bill was a healthy 1.21, it is much less relevant given the lower profitability of the segment. The Transit backlog is also getting further out, with both sequential and year-on-year declines in next 12 month backlogs. With some very long-term orders potentially skewing the Transit total backlog, we would view the next 12 month reading as more indicative of demand trends. With U.S. and Canada ridership down ~1% in 4Q 2015 despite peaking employment (lower gas prices?), usage trends do not seem robust.

Total Backlog: Total backlog for delivery in the next 12 months was down 19.6%, which also doesn’t point to a great topline for 2016.

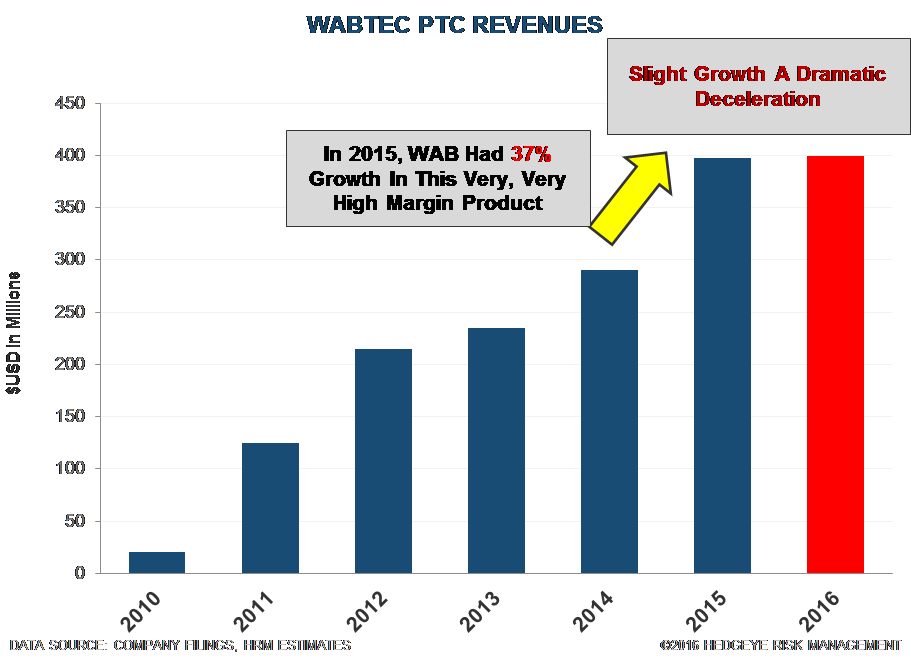

Aftermarket & PTC: Aftermarket sales were only specified for the year, but we calculate a 16% decline in fourth quarter aftermarket revenue ex-PTC sales (PTC is lumped in with aftermarket). In a very interesting disclosure on the call, management suggested that 75% of PTC revenue was to North American Freight, while only 15% was to Transit and 10% international. If accurate, that would spell big trouble for ultra-high margin PTC revenues as the 2018 deadline approaches…unless you believe the defensive speculation about PTC aftermarket opportunities. Further, management is guiding to “slight growth” for PTC sales in 2016. We estimate that PTC revenues are currently right around peak levels, and “slight growth” would represent a dramatic deceleration in PTC sales growth.

PTC has been a significant profit driver for WAB, and “slight growth” sounds like “peaking” to us.

Mix Negative: With the Transit segment taking the lead heading into 2016, we would expect negative mix to pressure margins. We see this as another reason to be skeptical of the 2016 EPS guidance.

Secular Change, Growth Holders In Trouble: From our perspective, this is the second earnings call with a negative tone; even when management was ‘excited’, they didn’t sound very excited. Management implied that the market was “on the way down”. Most importantly for growth holders, management said in prepared commentary that “headwinds could represent secular changes in our markets….” If you look at what WAB is doing - shifting capital allocation towards buybacks and larger public deals, for example – it would certainly seem that they are signaling that their market is past peak. If we had to guess, the large number of growth holders stuck in a deeply cyclical railroad equipment value trap will have a very difficult time finding the liquidity to sell. In the end, we’d bet they end up grateful for the elevated short interest.