Our cartoonist Bob Rich captures the tenor on Wall Street every weekday in Hedgeye's widely-acclaimed Cartoon of the Day. Below are his five latest cartoons. We hope you enjoy his humor and wit as filtered through Hedgeye's market insights. (Click here to receive our daily cartoon for free.)

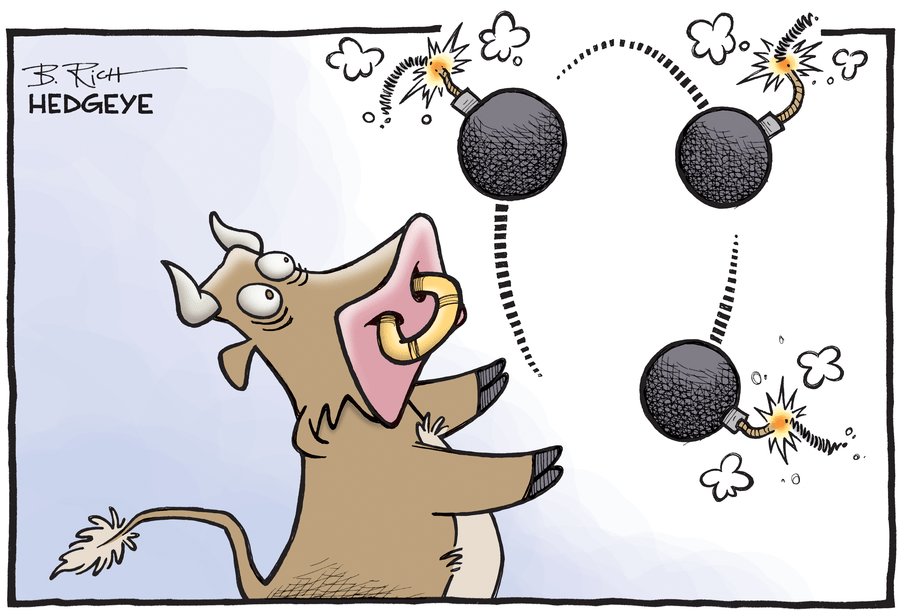

1. Juggling Bull (2/19/2016)

"We need to suck every last permabull into believing that the "bottom is in", then kaboom," Hedgeye CEO Keith McCullough wrote earlier this week.

2. Crash Test Dummies (2/18/2016)

The stock market is headed for a crash.

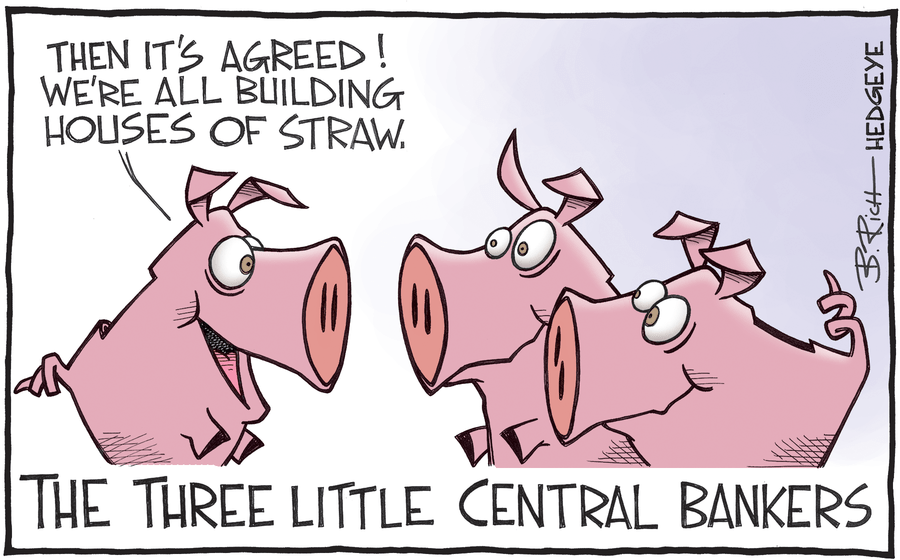

3. The Three Little Pigs (2/17/2016)

Central bankers have become concerned about recent tumult in financial markets. They should be. Macro markets continue to signal economic growth is slowing.

4. The Dying Cartel (2/16/2016)

News of OPEC's death might not be an exaggeration.