Newmont reported disappointing results that were in line with our December Black Book. We provide a summary of the results below and highlight three noteworthy items. While it is buried in a greatly expanded 10-K, NEM continues to capitalize stockpile & ore on leach pad costs using a $1,300 gold price, even though it lowered its reserve price assumption to $1,200. A long-term copper price assumption of $3.00/lb. to capitalize stockpile & ore on leach pads and $2.75 for valuing reserves is even more optimistic in our view. We expect NEM to continue to struggle with production costs, and forecast higher than expected gold mine output growth. For background, please ping us for our Gold & NEM Black Book and EQM model & datasets.

1. Wrong Way, Higher Costs & Cash Burn Threaten Bull Thesis: We see NEM’s gold production cost reductions as unsustainable and partly non-economic. In the fourth quarter release, AISC moved up to $999/oz, amazingly just $1 below the sub-$1000 guidance. That compares with $927/oz in 4Q 2014 and an average of $898/oz for all of 2015. For longs, this is a meaningful piece of disconfirming evidence on NEM’s ability to adapt to a lower gold price environment. Only about $26/oz of the year-over-year increase was from higher ‘sustaining capital’, a dubious concept at best. The bulk of the year-on-year cost increase in the AISC framework was from Costs Applicable to Sales (a bit under $50/oz), which is harder for management to explain away. While only a single quarter, it is worth noting that free cash flow was -$185 million in 4Q 2015; the bull story of NEM being a “most improved”, “adapting to low price environment”, and “cash generating” miner seems at risk.

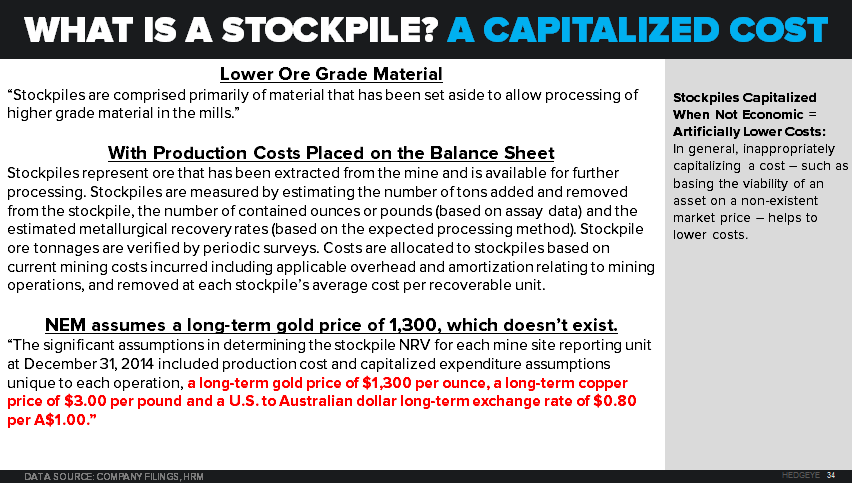

2. Pick-A-Gold Price Assumption, Capitalizing Expenses: The most surprising aspect of the 10-K for us was the continued use of a long-term $1,300 gold price assumption for stockpiles & ore on leach pads. NEM dropped its 2015 long-term gold price assumption for Reserves to $1,200/oz from $1,300 last year. How does it make sense to use two different gold prices for similar assets? It doesn’t, as we see it. An above market gold price does allow for capitalizing of costs related to stockpiles that would be expensed at lower gold price assumptions. We believe that NEM is capitalizing an expense by using inconsistent long-term gold price assumptions, presenting an unsustainable cost profile at current gold prices.

3. 2016 Costs Expectations Likely To Increase: While 2016 guidance did not change except for a small drop in capital expenditures, higher fourth quarter costs may shift expectations to higher in the AISC range. As it stands, the midpoint of guidance puts AISC costs up about 3.5% from 2015, which would seem the wrong direction. The cost guidance is also likely back-end loaded, with the Merian mine launch and cost improvements at Carlin offering year-on-year improvement. We would be quite interested to hear what 2016 AISC would look like with a $1,200 gold price assumption, and hope the question gets asked on the earnings call this morning.

Key Data and Notes on Earnings Report (Q4 2015 vs. Q4 2014)

- Missed top-line, EBITDA, bottom line and FCF estimates

- Reported Copper AISC and CAS each declined 37% (seems absurd). Gold AISC and CAS both increased +8% Y/Y

- For the full year, stockpiles and ore on leach pads increased +$230MM to $896MM as of 12/31

- Big jump in reclamation and remediation expense ($192MM in Q4 15’ vs. $93MM in Q4 14’)

- Impairments long-lived assets sizable: $50MM vs. $8MM Q4 14’

- For the full-year, impairments of investments, impairments of long-lived assets, and deferred income taxes added up to a $488MM in non-cash reconciliations for FCF bump over 2014 ($744MM vs. $328MM in 2015)

- Large jump in production from Batu Hijau in Indonesia in Q4 (especially in copper). Considering their copper price assumptions for carrying value of inventories (NRV), need to watch this closely. Copper sold in Q4 was 40K tonnes and copper produced at Batu Hijau alone was 51K tonnes. Spot copper prices are 31% below NEM’s long-term copper price assumption.

Q4 2015 vs. Q4 2014 in $MM (All reported numbers vs. BBG consensus estimates):

- Sales ($MM): $1,816 vs. $1,817 est. ($2,017 2014)

- Gold Costs Applicable to Sales (CAS): $680/Oz. (+8% Y/Y)

- Gold Reported AISC: $999/Oz. (+8% Y/Y)

- EBITDA (Adj.): $466 vs. $546 est. ($)

- Free Cash Flow: -$188 vs. -$54 est. ($)

- Net Income (Adj.): $20 vs. $61.9 est. ($86MM 2014)

OPERATING

Gold:

- Attributable Gold Sales (thousand Oz.): 1,237 oz. vs. 1,243 oz. Q4 14’

- Attributable Gold Production: 1,247 oz. vs. 1,261 oz. Q4 14’

- Consolidated Production: 1,406 oz. vs. 1,389 oz. Q4 14’

- AISC: $999 (+8% Y/Y)

- CAS: $680 (+% Y/Y)

Copper:

- Attributable Copper Sales (thousand tonnes): 40 vs. 34 in Q4 14’

- Attributable Copper Production: 39 vs. 29 in Q4 2014

- Consolidated Production:

- AISC: $1.51 (-37% Y/Y)

- CAS: $1.18 (-37% Y/Y)

2016 FULL-YEAR GUIDANCE

Gold

- Attributable Gold Production: 4,825-5,295

- Consolidated Gold Production: 5,

- AISC: $900-960

- CAS: $650-700

Copper

- Attributable Copper Production: 120-160

- Consolidated Copper Production: 210-250

- AISC: $1.50-1.70

- CAS: $1.20-1.40

Please feel free to reach out with any comments or questions. For access to our December blackbook or previous work in the sector, ping us directly at