"We need to suck every last perma bull into believing that the 'bottom is in,' then kaboom," Hedgeye CEO Keith McCullough wrote earlier this morning.

McCullough has now advised subscribers to short eleven different stocks in Real-Time Alerts, up from two at last week's lows.

This bounce has a suspicious air about it.

... And all today proves is that there are a lot of investors out there who have not learned this ultimate lesson... yet.

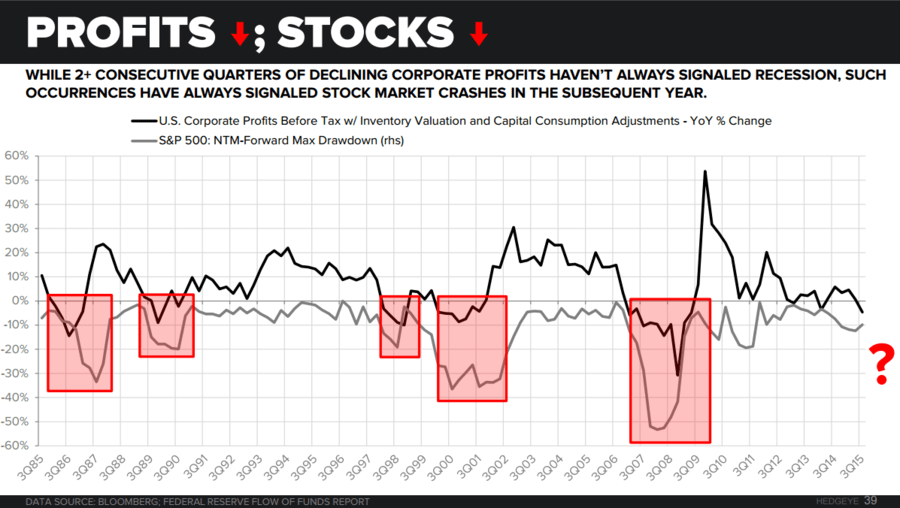

Here's another reason not to be long equities. Below is a chart from our 73-page quarterly Macro themes deck which shows when S&P 500 earnings decline for two consecutive quarters stocks fall -20% or more.

Take two minutes to watch the video below with key risk management insights from McCullough in which he concludes, "Are you bearish enough?"

Here's what our subscribers are saying about us: