Editor's Note: Below is a brief excerpt and chart from today's Early Look written by Hedgeye CEO Keith McCullough. Click here to learn more.

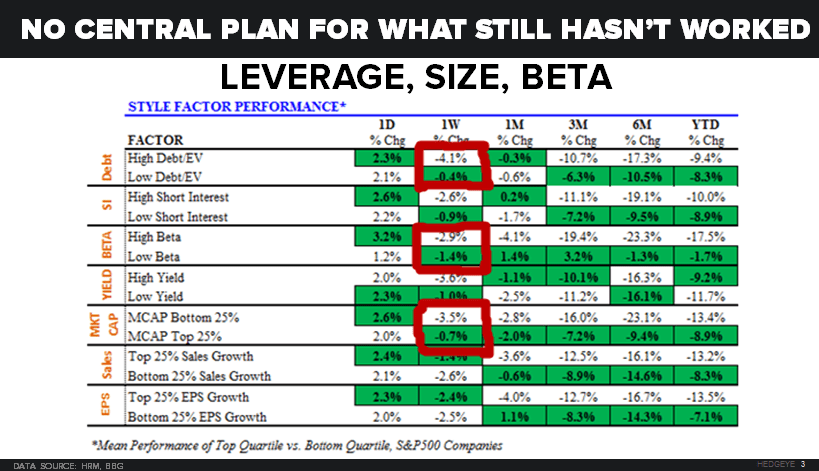

"... Other than Oil deflating another -4.7% last week (-22.9% for the YTD alone) and Bond Yields continuing to crash (UST 10yr Yield down another -9 basis points on the week to 1.75%) what other US Equity Style Factor messages were in the market last week?

- LEVERAGE: High Debt (to EV) Stocks led losers down another -4.1% on the week to -9.4% YTD

- SIZE: Small Cap Stocks were down another -3.5% on the week to -13.4% YTD

- BETA: High Beta Stocks underperformed beta (SP500) again, -2.9% on the week to -17.5% YTD

*Mean performance of Top Quintile vs. Bottom Quintile (SP500 Companies)"