“The risk that you end up bankrupt despite having the odds in your favor.”

-Lasse Heje Pedersen

For any of you who have studied statistics, the Gambler’s Ruin is a classic in risk management. It’s part of a general theory by Dutch math/physics genius (a real one), Christiaan Huygens and a critical lesson for fund managers – liquidity risk.

As Pedersen explains in a discussion about Liquidity Spirals, “investors hope to have an edge (alpha) but have limited capital (with leverage) that is subject to margin requirements. In investments, this risk is often referred to as funding liquidity risks. Whereas market liquidity risk is the risk that you cannot sell your securities without incurring large transaction costs, funding liquidity risk is the risk that you must sell them!” (Efficiently Inefficient, pg 81)

Being forced to sell because you aren’t allowed to buy more is one thing. If you gave them the capital, some of the super “smart” people in this profession would average down the whole way assuming that their edge is their own perceived genius. What happens when what they thought was “right” (in their favor) becomes dead wrong? Oh boy.

Back to the Global Macro Grind…

“A liquidity spiral is an adverse feedback loop that makes prices drop, liquidity dry up, and capital disappear as these events reinforce each other. The spiral starts when some kind of shock to the market causes leveraged traders to lose money.” -Lasse Heje Pedersen

Sound familiar?

The most important question about a liquidity spiral is what caused the “shock”? This is where the storytelling from the Old Wall and all of its conflicted compensation schemes begins. With the SP500 and Russell 2000 closing at fresh 2016 lows yesterday (down -14.1% and -26.4%, respectively, from their all-time #Bubble highs), I’ve heard everything at this point, including:

- China

- Oil

- The Weather

- “Risk Parity”

- Algos

And while it humors me to consider that none of these factors were blamed for all of the compensations we had during the bull market, it is nice to see that Jamie Dimon is putting some of that money back to work trying to be the causal factor in JPM’s stock.

Newsflash: no bear market ended (after it just started) with a guy buying his own stock.

I hear Dimon is a great guy (so is my Dad) but I completely disagree with him on the US economy right now. The real debate here is about two of the most basic causal factors in all of macro – GROWTH and INFLATION.

Dimon (a big time Democrat – and a much more big time man of the Old Wall than I’ll ever be) believes, like Barack Obama, that a non-partisan-independent-researcher like me is “peddling economic fiction.” Whereas I believe, like markets, that I’m telling the truth.

“So”, as Janet Yellen prefaced every answer during her confused testimony on Capitol Hill yesterday, what is the truth?

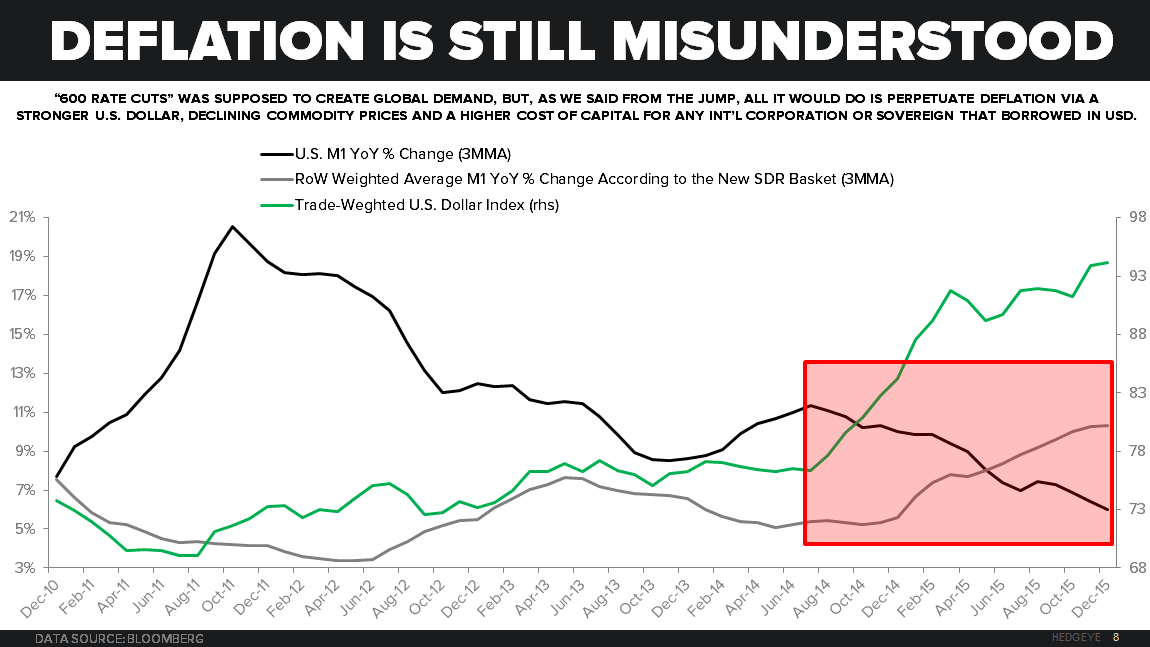

- On INFLATION: Is #Deflation Risk “transitory” or pervasive?

- On GROWTH: Is the US Economy accelerating or decelerating?

- On Liquidity & Leverage: is the risk on Dimon’s sell-side balance sheet or the buy-side’s?

I think anyone who runs money (different than running for office or running a bank) knows that the answers to these questions are becoming as obvious as negative bond yields have become.

When you boil down what Yellen had a very hard time distilling yesterday, the most basic market expectation implied by $7 TRILLION (and climbing) negative yielding sovereign bonds is called #Deflation.

If you haven’t understood the causal factor behind Global #Deflation all along (Bernanke devaluing the US Dollar to a 40 year low in 2011 – creating unprecedented mountains of supply and leverage on the premise that 0% rates = 0% risk), you need to meet with me.

Yes, Jamie. I want to meet with you (can someone forward this to him please).

I’ll humbly submit that I know the bear case for both growth and inflation as well as anyone else who has authored it. The risk here is the other side of my free-market-opinion.

That risk is really simple. The belief system that central-planners and bankers around the world can arrest economic gravity via currency devaluation and “easing” is seeing the odds fall out of its favor. You can end up bankrupt by being dead wrong on that too.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 1.58-1.81%

SPX 1

RUT 935-990

VIX 23.97-29.50

EUR/USD 1.07-1.14

Oil (WTI) 25.98-29.99

Gold 1170-1245

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer