Below are our analysts’ new updates on our thirteen current high conviction long and short ideas. As a reminder, if nothing material has changed in the past week which would affect a particular idea, our analyst has noted this. Hedgeye CEO Keith McCullough’s updated levels for each ticker are below.

LEVELS

Trade :: Trend :: Tail Process - These are three durations over which we analyze investment ideas and themes. Hedgeye has created a process as a way of characterizing our investment ideas and their risk profiles, to fit the investing strategies and preferences of our subscribers.

- "Trade" is a duration of 3 weeks or less

- "Trend" is a duration of 3 months or more

- "Tail" is a duration of 3 years or less

IDEAS UPDATES

TLT | XLU | JNK

To view our analyst's original report on Junk Bonds click here and here for Utilities.

What a week it was! After significant declines early in the week, Friday rallied hard. In terms of our Investing Ideas, our long position in Long-Term Treasuries (TLT) that rose +4% and our short position in Junk Bonds (JNK) that fell -1%. Utilities (XLU) worked against us for a -2% loss on the week, but remain an outperforming sector YTD.

For yet another week, investors were confronted with our signal of #GrowthSlowing in the U.S. and globally. Even the White House came out to reduce 2016 U.S. inflation assumption to 1.5% from prior expectations of 1.9%!

New scares in the form of increased risk from the financial sector emerged this week. On Monday, Deutsche Bank made headlines over liquidity concerns that tied into CEO Keith McCullough's favorite S&P Sector short, the Financials. That call is based on our uber bullish view on Long Bonds and Financials being the most over-owned group relative to its rate risk – XLF is now -14% vs. Utilities (XLU) +5.3% YTD.

Clearly, a drag on the Financials sector will remain the compression in the yield curve. We’ve called for yield compression alongside our signal of growth slowing and our expectation that global investors will continue to pile into US Treasuries as a “safe haven” liquid play. On the week, the US 10 year fell 13bps to 1.736%.

Looking ahead, be aware of the thick Central Bank calendar in March that’s like to increase pin action across global currencies.

- 3/9: Bank of Canada rate decision

- 3/10: ECB rate decision

- 3/14: BoJ rate decision

- 3/16: Fed rate decision

- 3/17: Bank of England and Swiss National Bank rate decision

As the #CurrencyWars persist, recent signals suggest to us that expectations for multiple hikes from the Federal Reserve have been muted (as growth and data indicators slow) and it appears highly likely that Mario Draghi’s ECB is set to expand QE in response to:

- The Bank’s inability to hit its 2.0% inflation target and;

- To stoke investors to chase the stock market higher.

In March, the ECB’s staff will release updated growth and inflation forecasts. This could be a catalyst for the Bank to announce an increase in its QE program.

Continue with our go-to macro market calls of long TLT and short JNK, and things don’t have to be so doom and gloom.

MDRX

To view our analyst's original report on Allscripts Healthcare Solutions click here.

Allscripts (MDRX) is scheduled to report earnings next week on 2/18. Management already pre-announced record 4Q15 bookings and gave EPS guidance for 2016 of 20-30% YoY at JPMorgan in January so the big catalyst for the stock will be revenue guidance for 2016.

We are expecting sales growth of +4.5% YoY compared to consensus of +5.6% YoY. The stock is down -7% since we added to Investing Ideas in January, versus -3% for the S&P 500. Therefore, the sentiment hurdle is lower heading into the print.

What will continue to drive the stock lower over the course of 2016 will be slower bookings growth after a record 2015 year due to a McKesson replacement opportunity that is largely dried up and services contract expansion with a large client that is one-time in nature. Further limiting bookings growth is that Allscripts has zero mindshare among large health systems in what is a saturated market for EHR systems.

NUS

To view our analyst's original report on Nu Skin click here. Below is a brief excerpt from a recent institutional research note written by Hedgeye Managing Director Howard Penney. NUS is on our Hedgeye Consumer Staples Best Ideas list as a SHORT.

NUS | “LAID AN EGG”

This was a terrible print, they missed consensus and internal expectations for the quarter, and provided down guidance for 2016.

Coming out of the investor day on December 4, 2015, in which management reiterated Q4 guidance, we remained skeptical of the underlying business trends, and unconvinced that the LTO’s would bolster the company enough to overcome that.

VitaMeal donations were down -22% YoY and down -13% sequentially from 3Q15. The exact profitability of this product is unknown, but, the large miss in the quarter could partially be explained by the steep decline in this product.

We remain very bearish on the fundamentals of the business, and skeptical on their ability to attract distributors in the future.

Management expects 1Q16 revenue to be between $450 million and $470 million, versus previous consensus estimate of $537.9 million. EPS is now expected to be $0.35 to $0.38, versus previous consensus estimate of $0.73.

Bottom line: We still see 25-50% of downside in the stock purely based on the fundamentals of the business.

WAB

To view our analyst's original report on Wabtec click here.

Wabtec's (WAB) repurchase seems to reflect anxiety about its sagging share price. Perhaps the Faiveley family is getting antsy about their discount to public holders. For long-term holders who liked the old Wabtec strategy, we do not see how a change in capital allocation as a positive signal. Stay short.

TIF

To view our analyst's original report on Tiffany click here.

Tiffany (TIF) short interest has pulled back from the recent peak in early December. Short interest has yet to match its 5 year highs of about 8.5% that TIF saw back in mid-2012 with the stock around $50.

We think this short still has room to fall. The risk of recession is rising and in the last recession TIF saw two consecutive years of low teens earnings declines. We don’t see why earnings would grow this year in this macro environment. Street expectations for 2016 are too high, and until they reset to a more reasonable levels we remain short TIF.

W

To view our analyst's original report on Wayfair click here.

Wayfair (W) sold off 25% over 3 days from last Friday to Tuesday of this past week. It has since bounced back a bit, recovering 8% on Wednesday while the CFO presented at a conference.

The stock was impacted by market commentators highlighting the weakness of Wayfair's business model. We are not the only ones who feel the model is flawed. We actually think the model is terminal and ultimately this stock is on its way to $0.

We continue to believe that the company will not be able to operate profitably at scale, and that all of the investments being made for a large addressable market will prove costly when the sales never materialize.

RH

To view our analyst's original report on Restoration Hardware click here.

Restoration Hardware (RH) announced this week that its COO is resigning on Feb 19th. The fact that COO Ken Dunaj is leaving RH bugs us, but only because of the ammo it gives the Street around the ‘Don’t Like Management’ argument against the stock. It’s not that Ken is/was on his own a major force behind driving growth and profitability.

This will probably introduce a ‘revolving door’ component to investor’s concerns about management. As for the issues around Gary being eccentric – those we can handle, and can easily refute. But the facts are stacking up about management leaving in a way that people will universally question RH’s ability to retain talent. They’ll look at the following…

- Carlos Alberini, Co-CEO who left to become CEO of Lucky in Dec 2013 (yes, people will revive ‘the Carlos argument’)

- Doug Diemoz, Chief Development Officer, left RH last summer after 15 months in order to be CEO of Crate & Barrel (not a big deal, RH has not missed a beat).

- Richard Harvey, head of Kitchens & Tablewear, who quietly left late 2015 after being hired to meaningfully grow the Kitchens business. (RH shifted gears and saw several opportunities to pursue ahead of kitchens. He left on his own accord).

- And now Dunaj, COO

In the meantime, RH is trading at 12x current year numbers and a long term earnings growth rate of 40% (both of which no one believes). In other words, it’s trading in-line with KSS, and 25% BELOW zero square footage growth retailers with peak margins (like FL, GPS). In the end, we think the risk for RH is isolated to the multiple, not the earnings, and that’s what matters most at these valuations.

ZBH

To view our analyst's original report on Zimmer Biomet click here.

LPNT reported a weak quarterly result and held their conference call this morning. While flu was weak in the quarter and impacted admissions, same store inpatient surgeries were also weak. They did not call out any specific specialties, such as orthopedics, but given that orthopedic surgery is the single largest revenue item for a hospital at 17%, we’d expect there was some pressure.

Growth did improve sequentially, albeit against an easier comparison from 4Q14, but if HCA is any indication, the national picture does not look good for 2016. HCA started to recover in 2013 and did even better in 2014 and 2015, peaking out when the impact of the ACA did in early 2015.

We’re seeing plenty of signs of weakness, from healthcare job openings, temporary healthcare openings, and reductions in consensus estimates for 2016 and 2017 to suggest the street is catching up to our view.

Zimmer Biomet (ZBH) should have continued issues in Europe and worsening conditions in the US as we progress through the year. The stock price definitely incorporates some of the weakness, but as of yet, not enough.

MCD

To view our analyst's original report on McDonald's click here.

No new update on McDonald's (MCD) this week, but the company remains one of analyst Howard Penney's top Long ideas in the Restaurants space. As we have continued to say, it boasts style factors ideal in turbulent times; high market cap, low beta and liquidity. While MCD is down (modestly) year-to-date, it's trounced the broader stock market. Since adding it to Investing Ideas in August, MCD shares are up 18% versus down -11% for the S&P 500.

Click the image below to watch a brief (60 second) video for a recap and key takeaways from McDonald's most recent earnings:

FL

To view our analyst's original report on Foot Locker click here.

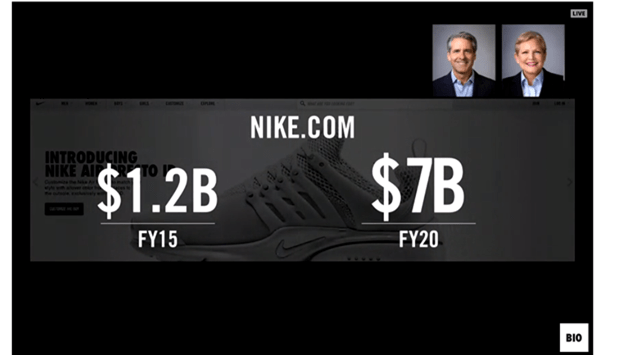

Two announcements came out of Nike this week that reiterate the company's commitment to e-commerce growth and direct distribution of its product. This movement will be a problem for the traditional wholesale channel as Nike DTC will be consuming a large portion of future growth in the Brand.

- Nike announced SNKRS Express, a touring brand experience for Nike + members that will be hitting select cities this weekend. This is another demonstration of the content owner, upstaging its traditional wholesale partners when connecting with consumers.

- NKE hired in Adam Sussman to lead the new digital platform. The company's investor day numbers imply digital will account for 30% of the incremental $20bn in dollar growth from FY15-FY20. We think the number is closer to 50% of incremental growth.

For the record, we think that Nike’s stated e-commerce goal of $7bn is low by 50% -- we’re looking for Nike to deliver $11bn by FY20

For Foot Locker (FL), we think that emerging competition from its top vendor, Nike (=80% of sales), will stifle growth. The company is likely to earn about $4.20 this year, which we think will prove to be the high water mark in this economic cycle.

GIS

Walmart is still having an effect on General Mills (GIS), but it isn’t any more or less severe than previously guided by management. They will begin to lap some of the effects caused by the retailer at the beginning of their 4Q16 (starting in March). Five years ago they dealt with a similar clean store policy implemented by Walmart. Coming out of that they seemed to have gotten more than their fair share of upside, specifically in cereal and fruit snacks, now they are seeing a little more than their fair share on the downside.