“Going negative is daring but appropriate monetary policy”

-Narayana Kocherlakota

We don’t operate in a silo @Hedegeye and we don’t claim to have a monopoly on good ideas.

As proof, sometime circa 2010, we introduced our proprietary Hedgeye Orb rating scale.

Back then – and before we got all stuffy and corporate - the blue orb was our calling card of sorts and we used the scale to infrequently rate non-Hedgeye generated analysis, central banker prowess, effective use of South Park and 90’s hip hop references, cheesy Canada jokes and so on.

If you’re unfamiliar, a 1-orb rating conveys inaccuracy, unoriginality, negative alpha and/or overall lameness. In contrast, the coveted & rarified 4-orb rating is issued for the conveyance of thoughtfulness, originality, &/or general non-consensus ballsiness.

With central bankers back-tracking, equities on the brink and credit & Fx markets balking, let’s bring back the truth serum orb for a guest appearance:

- $7T in negatively yielding debt globally: 1-orb, totally lame

- Central Banks, globally, announcing (again) more or what hasn’t worked ….. on groundhog day: 1.5 orbs (+0.5 orbs for amusingly ironic timing)

- Gundlach’s use of the “mission accomplished” banner as a metaphor for the fed rate hike (the allusion being to George W. Bush on the Aircraft carrier and the pre-mature and retrospectively misguided victory lap): Original & Accurate: 3-orbs

Back to the Global Negative Rate Grind …..

Kocherlakota – outgoing Minneapolis Fed President/FOMC member and widely suspected owner of the infamous negative blue dot in the Fed’s September Dot Plot – has been chirping Team Janet from the bleachers from the minute he left the field.

Now with …

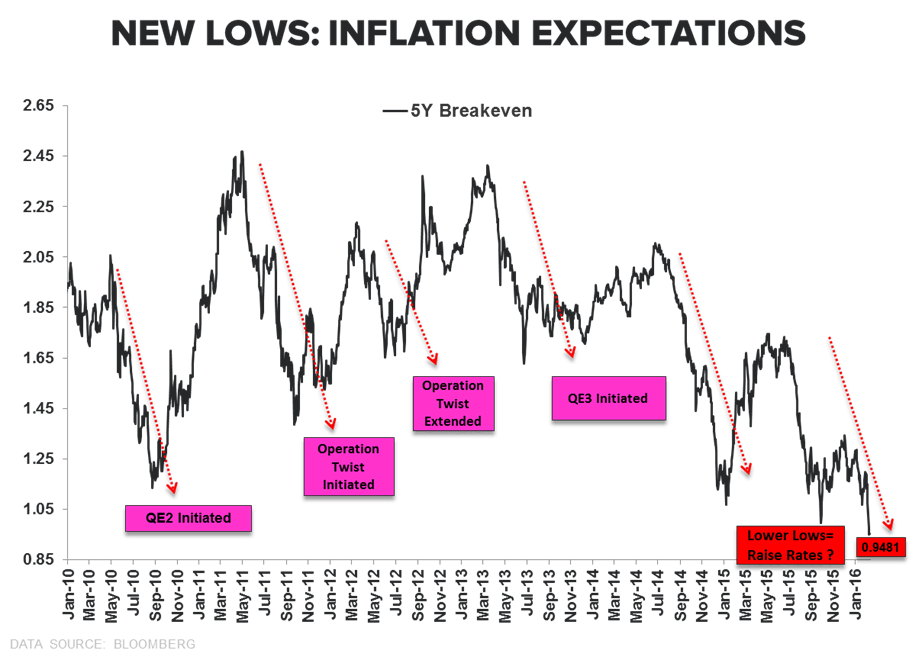

- Inflation expectations making lower lows (5Y Breakevens = 0.94% last, lowest since May 2009) … and the trend similar across the major sovereigns

- 10Y Yields: Down another -5pbs this morning to 1.61% (lowest since the 2012 all-time lows)

- Yield Spread (10’s-2’s): 98bps last and breaching 1.0% to the downside for the 1st time since 2007

- U.S. High Yield Yields and Spreads making higher highs

- Investment grade spreads making higher highs

- High Yield Energy Debt making higher highs (yielding 20.21% as of yesterday’s higher high)

- Lending Standards tightening and domestic Loan Demand falling (latest Senior Loan Officer Survey)

- Eurodollar futures are now pricing the probability of negative rates in the U.S. by 2017 at 17% (up from 2% at the start of the year)

And with futures red and global equity & energy commodity markets continuing in crash mode overnight, the carnage score is currently (% chg off of 52wk high):

- Brazil: -31.1%

- China: -46.6%

- France: -25.5%

- Germany: -28.9%

- Greece: -54.9%

- India: -23.6%

- Italy: -33.9%

- Japan: -25%

- Russia: -38.6%

- Spain: -33.7%

- USA (Russell 2k): -25.7%

…. Collectively, the active policy maker contingent, is now getting Koch’d up:

- Fischer: “[Negative Rates] its been better than we thought … working more than I can say I expected”

- Bernanke: “it’s a go to” …“I think negative rates are something the Fed will and probably should consider if the situation arises,”

- Dudley: “if the economy were to unexpectedly weaken dramatically, and we decided that we needed to use a full array of monetary policy tools to provide stimulus, it’s something that we would contemplate as a potential action,"

- Fed (2016 Bank Stress test): “include negative yields on short-term rates in your stress test” (1st time including this) and …. "This scenario does not represent a forecast of the Federal Reserve,"

- Yellen (yesterday): “We will look at it, and should look at it”

Conventional thinking has held that 0% on nominal rates represented the lower bound, mostly because nominal returns on cash aren’t <0%. Theoretically true …. until you add the costs to store institutional sized levels of cash, insure it, protect it ,etc.

You don’t have $7T in negative yielding debt because everything is awesome and you don’t field a chorus of “will you go negative?” questions when the data is conspicuously supporting a hawkish lean.

Janet held the policy normalization line in her testimony yesterday but for a Fed pre-occupied with ‘communication tooling’ and pro-actively leading markets via carefully crafted rhetorical gradualism, that seems like a lot of verbal table setting

Switching gears, Initial Jobless Claims and Retail Sales (Jan data) will round out this week’s domestic macro data flow.

Jobless Claims: At 285K, rolling initial claims are at their highest point since April of last year and we’re coming up on the anniversary of the trough level in claims recorded last year - meaning that the best they can do going forward is not get any worse. Think of it as if it was a company at full earnings power/potential and the best it could do is not see earnings decline going forward. What would that be worth … or what macro multiple would you put on that setup?

Retail Sales: The further decline in gas prices in January will weigh on the headline (recall, Retail Sales represents spending on Goods and are reported in nominal dollars) while the +1.4% MoM rise in auto sales (autos = ~21% of total) will serve as a positive offset. Further, base effects (i.e. a positive comp setup) stemming from the severe weather in the Dec-Feb period last year will provide a modest support to reported growth. More broadly, the trend in Retail Sales growth remains one of deceleration. In fact, growth has been slowing steadily since 2011 as demographics, urbanization, “collaborative” and “conspicuous” consumption and the end of the LT interest rate cycle have all driven spending towards services and experience (a topic for another Early Look).

In short, this week’s fundamental data will not be the #GrowthSlowing foil the Fed is stalking.

Yesterday, my 5-yr old son won a jiu-jitsu tournament as the youngest kid in his class - then, an hour later, his 3-yr old sister made him tear-up and tap out: 4-orbs

Economic gravity has markets and policy makers in an arm-bar. With volatility in bullish formation, risk ranges open on the downside and confidence in central planning breaking down, the capitulatory tap-out probably hasn’t been realized yet.

As the saying goes, “Everyone has a plan until they get punched in the face...”

Our (7-month old) plan = Don’t get punched in the face ... Long Bonds and bond proxies remains the rope-a-dope strategy

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 1.57-1.85%

SPX 1

RUT 940-995

Nikkei 159

VIX 23.02-28.98

EUR/USD 1.07-1.14

Oil (WTI) 25.83-30.27

Good luck out there today.

Christian B. Drake

U.S. Macro Analyst