RH - RH Secures Lease on Historic Landmark Building at San Francisco’s Pier 70

(http://www.businesswire.com/news/home/20160208005257/en/)

Typical RH maneuver in its backyard of SF. Taking a Flagship spot in a new redevelopment, while being one of the first retailers to sign on the dotted line. Leads to below market rents, in an up and coming retail space. That allows the landlords to attract the right type of cotenants around RH as the anchor.

KATE - Running Flash Sale. Same Time As Last Year.

Promotional cadence planned flat in 2016 after 2015 quality of sale initiatives at both wholly owned and wholesale distribution in the US. One of the many tailwinds for the brand as we enter FY16.

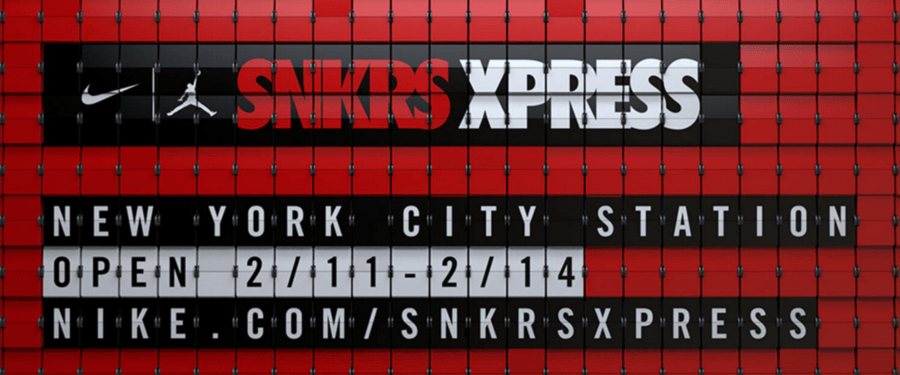

NKE - Nike hosting All-Star sneaker events in 4 cities this year where it promises new releases and surprise drops

Another demonstration of the content owner, upstaging its traditional wholesale partners when connecting with consumers.

(http://news.nike.com/news/nike-jordan-all-star-experience)

NKE/FL - The footwear business could be entirely software-based in 15-20 years

(http://vampfootwear.com/preparing-for-a-3-d-printed-footwear-industry/)

AMZN - AWS announces Cross-Platform 3D Game Engine Integrated with AWS cloud &Twitch

(http://www.businesswire.com/news/home/20160209005740/en/)

KORS - Marc Jacobs announces new accessory strategy and price restructuring -- moving leather towards 70% of sales, exceeding Michael Kors' 68.4%

ULTA - Jessica Alba's Honest Beauty line teams up with Ulta to expand nationwide distribution

SKX - Sketchers to extend contract with US marathoner Meb Keflezighi

Burberry - Fashion shows becoming marketing tool as Burberry will move to a see-now/buy-now collection model -- will no longer unveil clothes six months before they are available in stores

FL - FL trying to create buzz with 2016 World Sneaker Championship partnership -- will sell winning design in stores later this year

LULU - Athletic apparel retailer Yogasmoga, a fast-growing LULU rival, to open first NYC location

(http://www.chainstoreage.com/article/fast-growing-lululemon-rival-open-its-first-nyc-store)

SBH - Sally Beauty Holdings has big ambitions for more stores and new services as it hits 5,000-store milestone

(http://www.retailingtoday.com/article/one-watch-sally-beauty-becomes-real-looker)