KEY POINTS

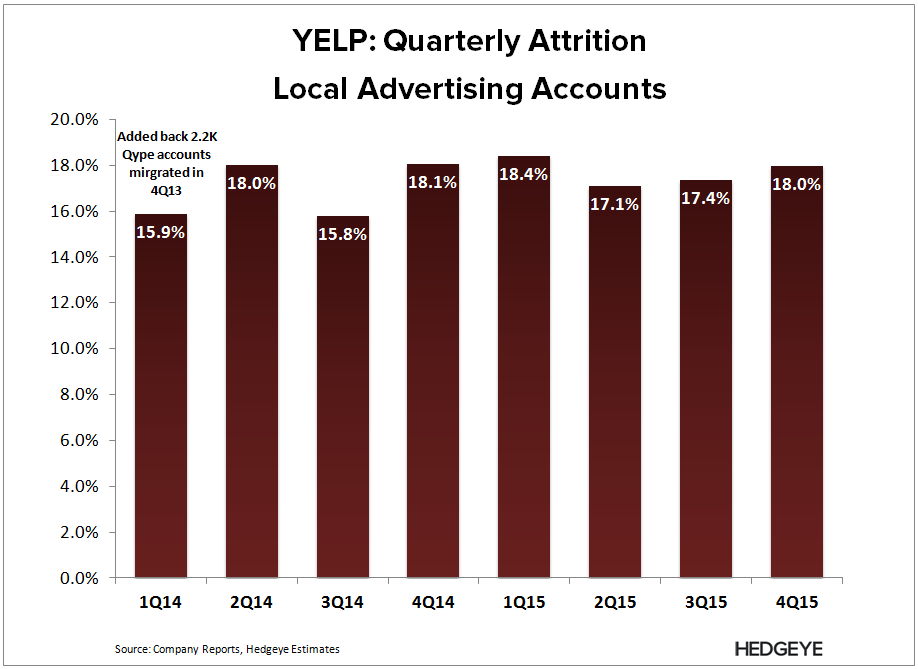

- 4Q15 = LOCAL DETERIORATING: This is now YELP's fourth consecutive miss on Local Advertising revenue. YELP produced decelerating new account growth of 22%, which is lower than the rate that it has onboarded sales reps in any quarter in 2015. Further, YELP’s attrition rate accelerated again in 4Q15, which suggests that its CPC ad product isn’t really improving its client’s ROI. Note that YELP has been selling CPC for well over a year and is now over 60% of revenue, so if CPC had the ROI that mgmt claimed, then we would have noticed it by now. The one bright spot from the quarter was accelerating revenue growth in its Eat24 business, but the transactions segment is almost too small to matter (10% of revenue).

- GOOD LUCK GUYS: YELP issued 2016 revenue guidance slightly above consensus at the midpoint ($693M vs. $688M), which translates to ~34% revenue growth (net Brand Ad revenues). YELP didn’t provide segment-specific guidance, so we’re not sure how mgmt plans to get there, or if it has an idea, but it’s more than a tall order. Post 4Q results, YELP now needs accelerating new account growth on historically low attrition rates to hit consensus Local Ad revenue estimates. That is also assuming accelerating salesforce productivity since its guided revenue growth is exceeding its saleforce growth target (20%-30%). The wildcard is its Google AdSense ads; we're waiting for the 10-K for additional color.

- SCAPEGOAT: YELP announced that its CFO, Rob Krolik, will be leaving the company after it finds a replacement, or by year end. We’re not sure if YELP is trying to use Krolik as the scapecoat, or if he’s jumping off the bus before the wheels fall off, but a new CFO won’t change much. The problem is the business model, which can’t be fixed unless mgmt is willing to take a hard landing (down revenues). YELP’s attrition can be attributed to poor ROI (note below); the easiest way to fix that is by introducing lower-tiered ad packages. But the risk there is that it would need that many more brand new customers to offset its attrition (e.g. at half the price, it needs twice as much new account growth).

Let us know if you have questions, or would like to discuss in more detail.

Hesham Shaaban, CFA

@HedgeyeInternet

YELP: Grand Tales of ROI

02/13/15 01:34 PM EST

[click here]