Editor's Note: Below is a brief excerpt from Potomac Research Group Senior Analyst JT Taylor's Morning Bullets sent to institutional clients each morning.

MARCO MISSED:

NH voters have had a full day to process Saturday night's debate and it's not good for Marco Rubio. Govs Christie, Bush and Kasich have all climbed in a number of polls conducted since the debate and are showing new life. Rubio had a chance to capitalize on real momentum coming out of Iowa and he blew it. The race for second is now a free-for-all. The absence of a convincing win for Rubio benefits current NH frontrunner Donald Trump as well as Ted Cruz, who is better-positioned for the SC primary. The longer there's no clear winner in the Rubio/Christie/Bush/Kasich fight to make it a three-way race, the better for Trump. With so much volatility in the race, why would anyone considering dropping out?

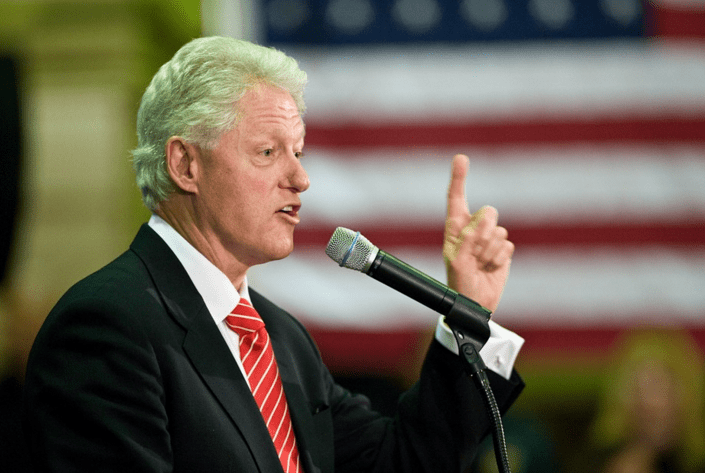

BIG DOG BARKS:

We're wondering why it took so long for Bill Clinton to step in and attack Bernie Sanders -- we know he's been chomping at the bit for weeks. Clinton took Sanders to task for being "hermetically sealed" outside reality, and exhorted his supporters to come to their senses as Hillary has been closing the gap on Sanders in the Granite State. Do you think they're reading the sequel to the Comeback Kid?