KEY POINTS

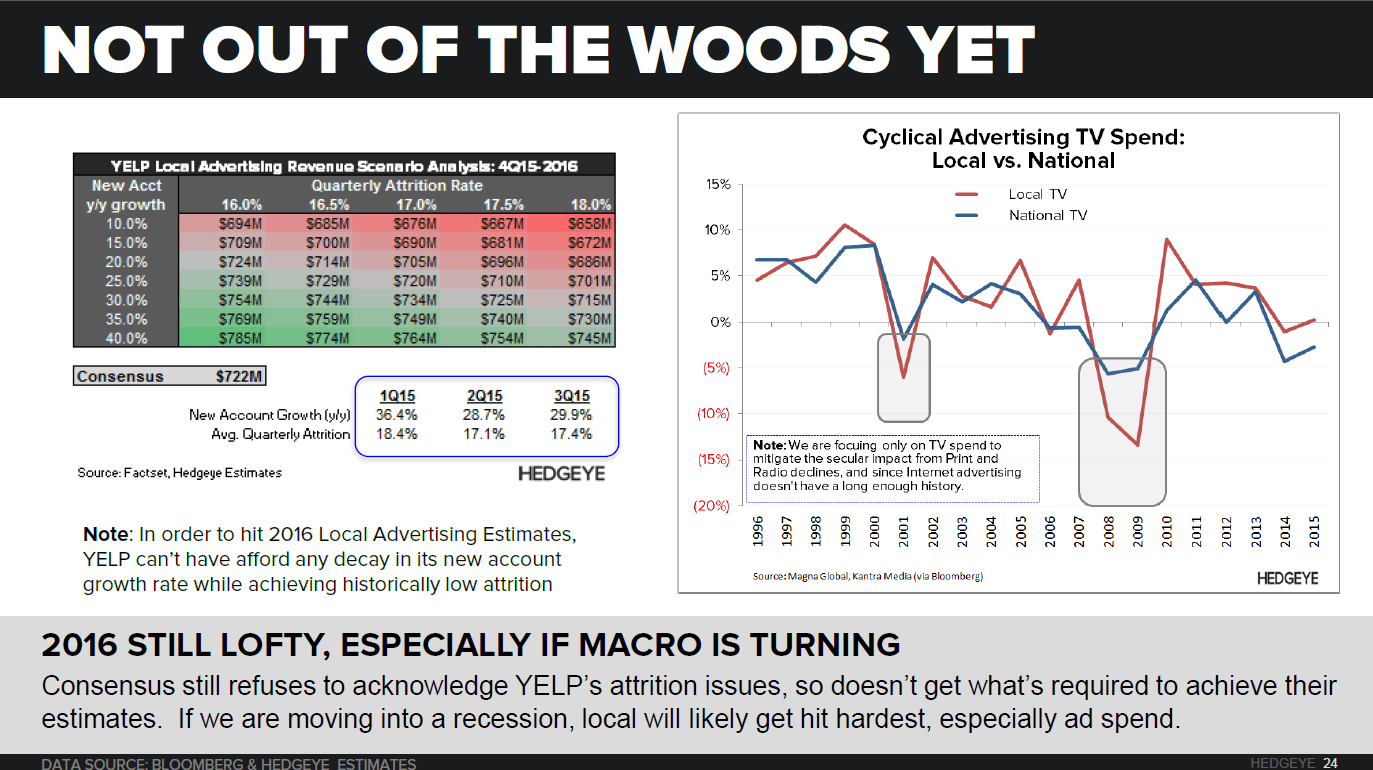

- 2016 IS UNATTAINABLE: Consensus is still not factoring attrition into its estimates, so it doesn’t understand the burden of new account growth necessary to hit those numbers. In short, YELP needs to maintain its current new account growth rate every quarter from now through the end of 2016, and that’s assuming historically low attrition rates. That’s highly improbable unless it accelerates its sales rep hires in excess of revenue growth guidance, and that alone might be a major red flag for the street.

- MACRO COULD MAKE IT WORSE: Remember that YELP caters to a relatively fragile customer base that doesn’t have economies of scale and is hostage to its local economics. If we are moving into a recession as our Macro team suggests, it’s going to be that much tougher to sell into that environment, especially since Local Advertising spend typically declines in excess of national spend in a recessionary environment (see notes in first slide below), and would likely exacerbate its account churn.

- WHAT’S UP YOUR SLEEVE? Just because YELP can’t hit 2016 estimates doesn’t mean it won’t guide to them. We saw that last year when YELP guided to 53% revenue growth (Eat24 included), then subsequentally cut its growth forecast to 44% two quarters later. This time around, there’s no telling what mgmt will do here, especially since it has a history of doing whatever it can to disguise the issues at its core. Either way, we suspect YELP really needs to show something on this release to drive its stock materially higher from here. We’re staying short till mgmt guides to something more reasonable than what consensus is asking of them.

Let us know if you have any questions or would like to discuss in more detail.