Below are our analysts’ updates on our thirteen current high conviction long and short ideas. If nothing material has changed in the past week which would affect a particular idea, our analyst has noted this.

Please note that we removed Federated Investors (FII) from the long side of Investing Ideas this week.

In case you missed it, click here to watch McCullough's "Macro Overlay" sent exclusively to subscribers on Friday where he covers the profit cycle and our U.S. Recession and Currency War Macro themes.

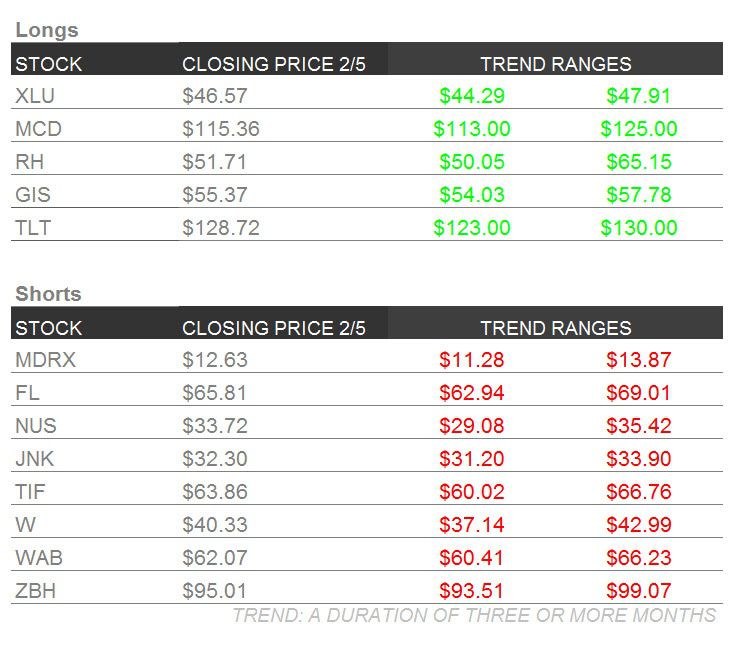

Updated levels for each ticker follow below.

LEVELS

Trade :: Trend :: Tail Process - These are three durations over which we analyze investment ideas and themes. Hedgeye has created a process as a way of characterizing our investment ideas and their risk profiles, to fit the investing strategies and preferences of our subscribers.

- "Trade" is a duration of 3 weeks or less

- "Trend" is a duration of 3 months or more

- "Tail" is a duration of 3 years or less

IDEAS UPDATES

TLT | XLU | JNK

To view our analyst's original report on Junk Bonds click here and here for Utilities.

Down go growth expectations and down goes the yield curve. That's the latest from Macro markets this week and it plays right into our long Long-Term Treasuries (TLT) and short Junk Bonds (JNK) Investing Ideas.

The U.S. 10-Year yield declined another -9bps this week which helped boost TLT +1.1% on the week. In a healthy environment, bonds as an asset class go up in tandem, but JNK lost -0.9% on the week despite a falling yield curve.

That’s because we’re NOT in an “all is good” environment. Credit spreads widen in turbulent times. This widening is the alpha-generating opportunity in long TLT, short JNK.

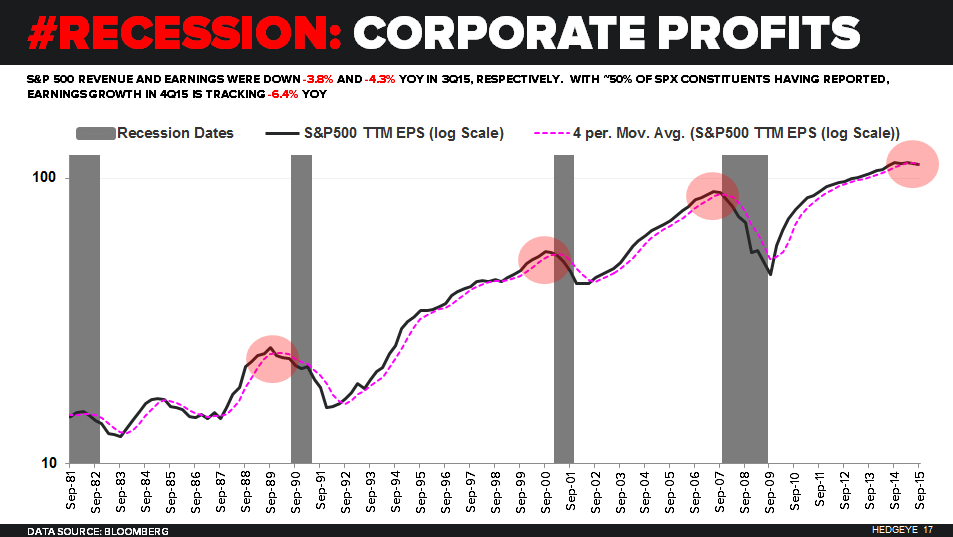

In our view, it’s not whether things are “good” or “bad” that matters ... it’s whether things are getting better or worse on the margin. Checking in on earnings season thus far (308 of 500 S&P 500 companies had reported at the time of publishing the chart below), earnings have gone from bad in Q3 2015, to worse in Q4 2015:

- SALES: down -4.7% Y/Y so far this earnings season

- EPS: down -6.4%

- NEGATIVE EARNINGS GROWTH SECTORS: Energy, Materials, Industrials, Consumer Staples, Financials, Info. Technology, Utilities

- POSITIVE EARNINGS GROWTH SECTORS: Consumer Discretionary, Healthcare, and Telecom

... And here's what happens when earnings peak and start to roll over. It's just one more chart, among many other indicators that paint the #GrowthSlowing picture.

On the Jobs Report front, labor market data is one of those indicators that also paints the #GrowthSlowing picture. Looking at Friday’s bomb of an NFP report, the point we can’t emphasize enough is that whatever the number could have been (and it was awful on the surface), the year-over-year rate of change in the data series has peaked and is now declining.

Here's the reality of the U.S. labor cycle:

- Non-Farm Payrolls (NFP) peaked at +2.34% year-over-year growth in FEB of 2015

- Friday’s NFP report (January) slowed to +1.8% year-over-year growth

- Most employment data is the most lagging of #LateCycle economic data you can measure anyway

As mentioned above, the bond market understands #GrowthSlowing. So do Utilities (XLU), which is why XLU is leading S&P sub-sector performance in 2016. XLU is up +7.6% versus down -8.0% for the S&P 500. Stick with it on the long side.

MDRX

To view our analyst's original report on Allscripts Healthcare Solutions click here.

Summa Health System, one of the largest integrated health systems in Ohio, made the decision to move to Epic in 2014. Summa operates 5 hospitals, with 2,000+ beds and a physician organization of 400+ providers. The Epic implementation began with the physician offices in the middle of 2015, with the hospitals slated for transition in 2016/2017. On the ambulatory side, this was a sizeable loss for eClinicalWorks, who had been the main EHR vendor for their physician organization. On the acute care side, Allscripts, Quadramed, CPSI, Medhost and McKesson will all be replaced with Epic.

The importance of this example is that Allscripts Healthcare Solutions (MDRX) has publically announced six new domestic Sunrise Clinical EHR contracts over the last 2-years, for a total of approximately 1,020 beds. Allscripts will lose 979 beds from two hospitals in 2017, as a result of a decision made by one health system. If we add the loss of Monroe Regional (238 beds), a Sunrise Client we identified as switching to Epic this year, then total bed losses climb to 1,217.

While Allscripts has gained traction internationally during this period, over the long-term, we don't believe it will be enough to offset the domestic decline, which represents more than 90% of revenue.

NUS

To view our analyst's original report on Nu Skin click here.

Nu Skin (NUS) is set to report 4Q15 earnings after the close on February 11. We will send subscribers an update on our thinking next week.

To be clear, we do not expect any change to our core short thesis.

WAB

To view our analyst's original report on Wabtec click here.

With earnings coming up on February 18, the market is set to get incremental information into Wabtec's (WAB) operations. Of particular interest will be an update on the acquisition of Faiveley. WAB’s now lower share price may make the deal less attractive to the controlling family.

On the broader short thesis, typically, in its more profitable US freight operations, WAB only gets a short lead time to new demand. While we expect demand to decline significantly in 2016, the company is likely to lack visibility.

Bottom line is we continue to see WAB as caught in a long-term downswing in rail-related capital spending.

TIF

To view our analyst's original report on Tiffany click here.

The street's EPS expectations for Tiffany have come down to $3.87 for FY 2016, 24% below where they were a year ago. Given the recent slowdown in sales and the increasing likelihood of a recession, these numbers still look optimistic.

Unlike department stores and clothing retailers, TIF can't try to blame the record warm weather for weak 4th quarter sales in the US. That's why we’re still 5% below the street in 2016.

W

To view our analyst's original report on Wayfair click here.

Wayfair will be presenting at an internet and tech conference next week. In its time as a public company, W has hit the conference circuit pretty hard, as it should. CEO Niraj Shah tells the Wayfair story pretty convincingly. Last year, W did 8 conferences and next week's will be number 2 in 2016. Most retail companies do 2-4 in a year, if any.

We’ll likely hear more of the same from W next week, mostly likely that the TAM (total addressable market) for W will approach $90bil. Our work shows it will be less than half of that. The problem is that the company is investing today to capture a slice of the market that we don’t think will materialize.

RH

To view our analyst's original report on Restoration Hardware click here.

We expect Restoration Hardware to continue to play offense. That includes continuing to execute on its real estate strategy as it expands its real estate presence in key markets across the US. Here’s a look at a few of the new markets, not yet announced, but that we have uncovered by scouring the Internet.

Three stores: Kansas City, Palm Beach, and Corte Madera, together make up ~165,000 square feet of retail space. That’s good for 16% growth over the current square footage.

RH is the only retailer in this space looking to upsize its current sq. ft. footprint, giving it favorable deals in the current retail real estate market. New store openings to date have met or exceeded expectations. The beauty of RH’s real estate play, is that rent per square foot on the new space is about 25% what it was in the legacy stores. That allows for big time leverage on a sales base 3x a legacy store.

In the old stores, RH could only show 10% of its assortment, while in the newer format stores, the company is showcasing better than 75%. Our work suggests that consumers are much more reluctant to purchase what they can’t see.

ZBH

To view our analyst's original report on Zimmer Biomet click here.

Healthcare analyst Tom Tobin has no update on Zimmer Biomet this week but reiterates his short call. The core thesis remains still firmly intact:

- "Employment growth slowing and fears of a recession will certainly dampen investor appetite for what is viewed as an elective procedure."

- "Our team's long-term view calls for slowing/declining unit volume and deteriorating pricing. The impact to gross margins should be significant with very little spending flexibility within the organization."

MCD

To view our analyst's original report on McDonald's click here.

WHAT WILL PROPEL THE NEXT LEG OF GROWTH?

Many investors are already asking this question. The fact that we are only two quarters into the turnaround, reveals the negative bias still surrounding McDonald's (MCD).

In addition to their current slate of initiatives – All Day Breakfast, McPick 2 and Menu simplification – management has a pipeline of initiatives that will drive the business forward.

The Mobile app seems like it could be a strong contributor to growth; so much so, management built incremental sales into their model based on sales expectations driven by their digital platform. In just three months since MCD launched the app, there have already been 7 million downloads. At the moment, they are merely testing response rates with low price offers with plans to greatly expand the capabilities over time.

Experience the Future and continued modernization of the portfolio will be a key aspect of the turnaround. Bringing their system into the current generation from a look and functionality standpoint will be very beneficial to performance.

Experience the Future is in about 130 restaurants and five markets in the U.S. Throughout 2016 and 2017, they plan to further penetrate two to three of those markets with the concept to further test its effectiveness. Other modernization/improvement initiatives that will drive growth include; remodels, digital menu boards, dual lane drive-thru’s and self-order kiosks.

While MCD had a rough trading day on Friday, we continue to like it long term given the style factors that we continuously remind you of: big-cap, low-beta and liquidity.

FL

To view our analyst's original report on Foot Locker click here.

The online data we track from a number of sources shows a continued slowdown in Foot Locker's online business since the end of the third quarter. This is not just an industry thing, or a category thing. We’re seeing Nike’s web traffic (along with Under Armour and Adidas) explode to the upside on a relative basis to FL, suggesting that the share shift from traditional retailers to the Brands is taking hold.

While the data looks quite ugly for FL, we want to reiterate that this is a fat-tailed transition. In other words, it won’t play out entirely in a single quarter. But, the negative online trends for FL that reared its head in 3Q seems to be carrying into 4Q.

GIS

No new update on General Mills this week, but the company remains one of analyst Howard Penney's top Long ideas in the Consumer Staples space. As we have continued to say, it boasts style factors ideal in turbulent times; high market cap, low beta and liquidity. While GIS is down year-to-date, it's held up very well against the broader stock market. GIS is down -4% versus down -8% for the S&P 500 in 2016.

As we have noted in previous updates, GIS has been picking up steam, as the company is working to improve merchandising and advertising on core business. One of the initiatives is making a distinct effort to delve deeper into the natural and organic category. That will certainly help them a lot in the long run. More to come.