I’ve participated in roughly 70 Ralph Lauren conference calls over the years. This one was the worst. Seriously…it’s not even close. It was even worse than the one in 2013 when Jackie Nemerov discussed RL’s initiative to host a fashion show for dogs.

The reaction in the stock is nothing short of violent. But quite frankly, it’s probably deserved. Why, you ask? We heard one thing repeatedly – very clearly – throughout the call. And that’s that this company will almost certainly go through another major restructuring. Yes, that’s restructuring #3. It will likely be announced in either May or August, and it will probably take 1-2 years. That was really the only message we took away, and is also the only one that really matters. Unless you’re really patient, this story is arguably uninvestable for another 12-18 months at a minimum.

So…what else did we hear on the call? On one hand, we heard new CEO Stefan Larsson (who is actually quite good – and could be impactful if given enough runway) talk about how he loves the brand and is learning the organization. Ok – not sure what to do with that. On the other hand we heard Chris Petersen, who on some level is probably wondering why he is not CEO, discuss his effort to ‘P&G’ Ralph Lauren (that’s our term, not his). Basically, it is the initiative to turn the one RL silo into six separate operating groups, and align in a way to accelerate growth globally. We’re a fan of this. But it takes a looong time to be impactful.

But who we didn’t hear, as usual, was Mr. Lauren, who is the one really calling the shots anyway. On Macy’s latest call, when it had to deliver a tough message to the Street about real estate plans (or lack thereof), CEO Terry Lundgren got on the call for the first time in eight years to ease concerns and show accountability. Mr. Lauren controls 81% of the voting stock at RL…do you think that just maybe he has a vested interest in helping out with the messaging? I know this sounds petty, and an unsolicited jab. But given the $3.8bn in equity value destroyed over the past 90 days, and the $7.7bn that vanished since the start of last year, we think it’s a fair expectation for Mr. Lauren to grace us with his presence for an hour. If he does not think it’s necessary, then it shows a disturbing lack of respect for his fellow shareholders.

Though there are a lot of moving parts with the financials, we heard two things as it relates to the quarter that struck us as especially noteworthy.

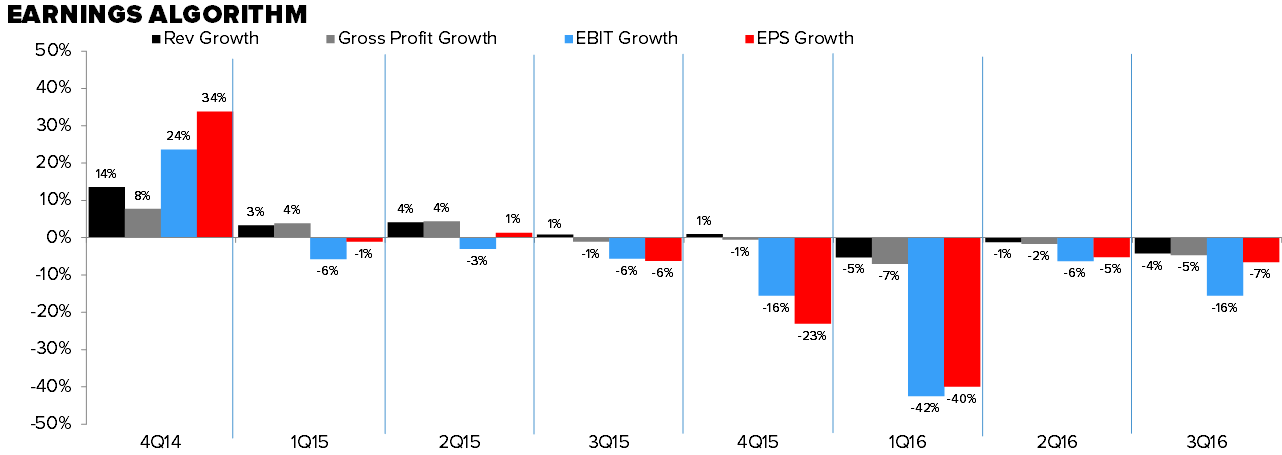

- Comps Tell A Huge Story. We don’t care a ton about a single quarter of comp. This is retail, and it’s a volatile place to be. But RL has comped down in each of the past five quarters (i.e. it comped down against a negative number last year). More importantly, it’s been 11 quarters since RL ceased to be a story based on taking back and consolidating licenses. During those 11 quarters, the company only surprised on the upside once. When it was taking back licenses, the comp trend was the exact opposite. Could we be talking late cycle now vs early cycle then? Perhaps. But it’s tough to argue that this company still has not figured out how to grow organically. The chart below tells a clear story.

- Markdown Money. Peterson mentioned ‘increased markdown money’ to wholesale accounts (department stores) in order to clear excess inventory headed into Spring. Let’s be clear – RL absolutely NEVER discusses ‘markdown money.’ This brand has always been above that. Clearly, it pays for markdowns behind the scenes, but to a far less degree than its competitors. Search back as far as you want – the last time the words ‘markdown’ and ‘money’ were uttered in a RL call, it is when I asked them about it in 2008. In any other print, this might have been a non-event. But with the management/culture/operational changes we’re seeing with RL and are likely to continue to see for the next two years (not to mention investor concerns about the Brand), we think this matters.