The note below was written by the Hedgeye Financials team and distributed to clients earlier this morning. To the extent you're interested in the team's work, email for more information

----------

How The Economic Machine Works

For anyone interested in a simple and (moderately) entertaining primer on the role credit plays in economic growth, we recommend Ray Dalio's youtube video "How The Economic Machine Works". In a nutshell, he explains how credit is simply the pull forward of consumption, which is why the credit cycle drives the business cycle. With that in mind, the Senior Loan Officer Survey data out yesterday afternoon is indeed troubling.

Two of Three C&I Measures, CRE Standards, and Expectations are Negative

The Fed released its 1Q16 Senior Loan Officer Survey yesterday afternoon. The survey was conducted between December 29 and January 12 and covers lending standards and loan demand across business and consumer loan categories.

In the previous survey (4Q15) banks began tightening, on net, C&I and CRE lending standards. This quarter (1Q16) not only did the net percentages of lenders tightening standards for those categories increase, but demand for C&I loans declined. Additionally, the Fed's survey this quarter included special questions regarding forward expectations, and loan officers indicated that they expected a further tightening of standards, increasing of spreads, decreasing volumes, and deteriorating credit quality over the course of 2016.

A small silver lining is that consumer lending showed benign conditions; a net positive, albeit sequentially smaller, percentage of banks continued to report easing of consumer lending standards.

Here is the main takeaways this quarter:

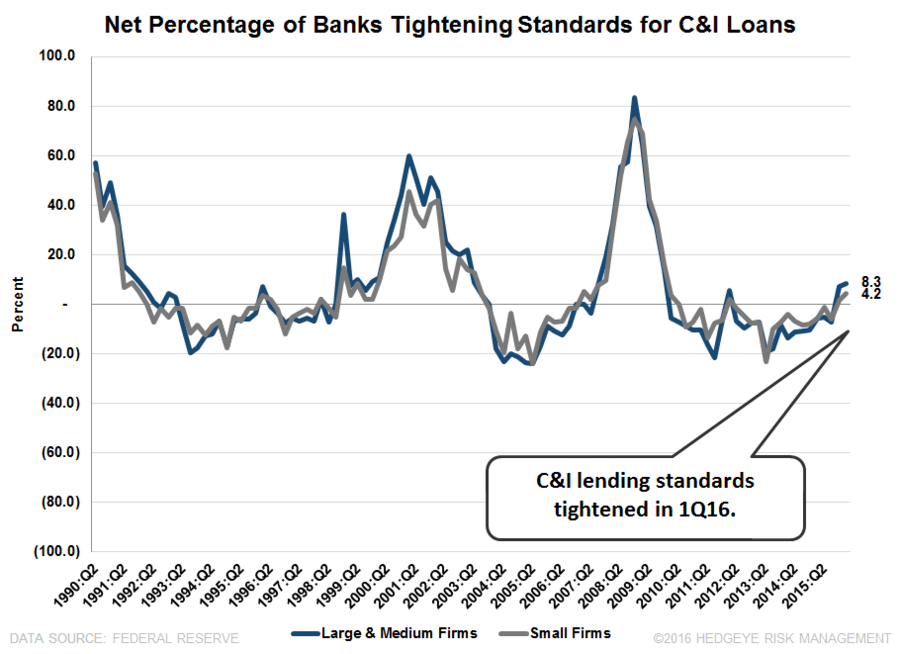

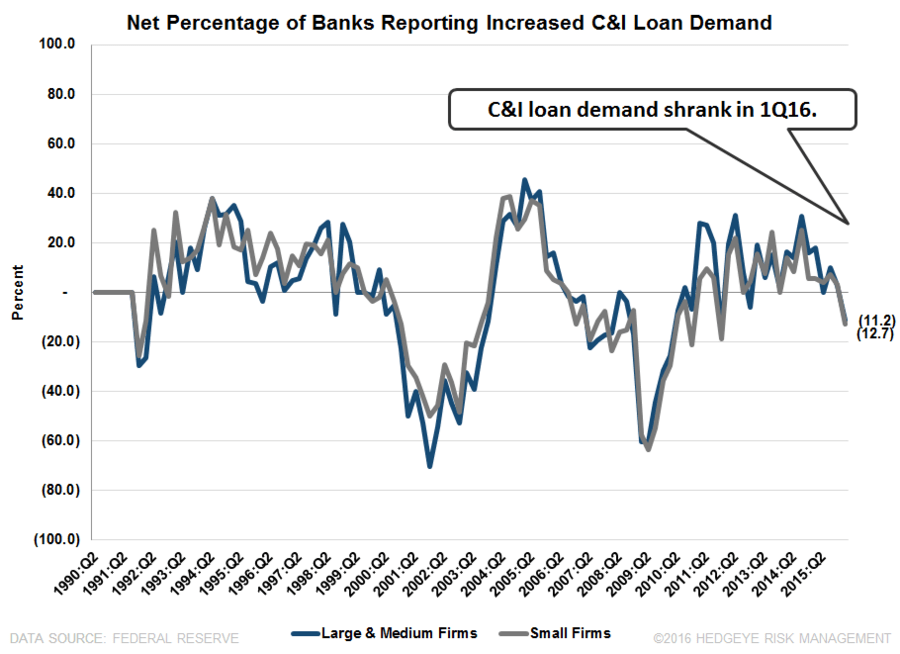

1. A net percentage of banks tightened C&I lending standards for the second quarter in a row. Moreover, demand for C&I loans inflected into negative territory this quarter. 11% of banks saw C&I loan demand decrease from large and medium firms (13% saw it decrease from small firms), signaling that borrowers expect a decreased need for capital.

Here's why this matters. We've gone back historically and looked at the Senior Loan Officer Survey many different ways in an effort to discern its usefulness as a forward indicator. After much trial and error, our biggest takeaway is that when two of the three C&I questions have turned negative historically, it has portended a recession in the near future. This isn't coincident, it's causal. Banks tightening the screws, increasing the price of money or reporting reduced demand for money all portend a slowing of econimc activity. The problem is that the cyclical activity tends to autocorrelate, or self-reinforce. In other words, banks tighten credit => consumption/investment decline => workers are laid off => delinquencies rise => banks further tighten credit => and so on and so forth. Below is a chart showing the three questions in the C&I survey back to 1990. To be clear, we've inverted the primary y-axis and we've also reversed the demand question so that all three categories are directionally consistent, i.e. when credit is constricting/price is rising/demand is falling, the survey measures on this chart fall, and vice versa.

Perhaps of equal interest is the fact that the Fed has historically had an enormous policy cushion in response to recessions. The table below shows that since 1969, the Fed has eased by an average of 750 bps in response to every recession. The last two cycles have seen the Fed ease by 560 bps and 520 bps. The challenge this time around is that the Fed's current policy cushion is 36 bps.

To summarize, credit conditions are tightening, which has historically ushered in a recession, and the Fed's short by around 5 percentage points on its ability to soften the blow.

The Data: The percentage of banks tightening C&I lending standards for large and medium firms increased to 8.3% in 1Q16. This is the only instance since the last recession that a net positive percentage of banks tightened standards two quarters in a row. The chart below illustrates.

Here's the Second Most Important Takeaway This Quarter:

2. CRE Tightening. Commercial real estate lending also saw continued tightening this quarter across all three categories: C&D, Nonfarm Nonresidential and Multifamily. Unfortunately, the survey format changed with the 4Q13 survey when the Fed replaced the single category of CRE loans with the three aforementioned subcategories. As such, it's not possible to compare apples to apples historically. That said, in the 10 quarters since the new format began, this marks the third (and third consecutive) quarter in which standards have tightened on C&D loans. It marks the second (and second consecutive) quarter in which Nonfarm Nonresidential loans have seen standards tighten. The Multifamily category has been bouncing between easing and tightening over the last two years, but it has never reached as high as the 22.6% of banks tightening this quarter.

And Here's the Third:

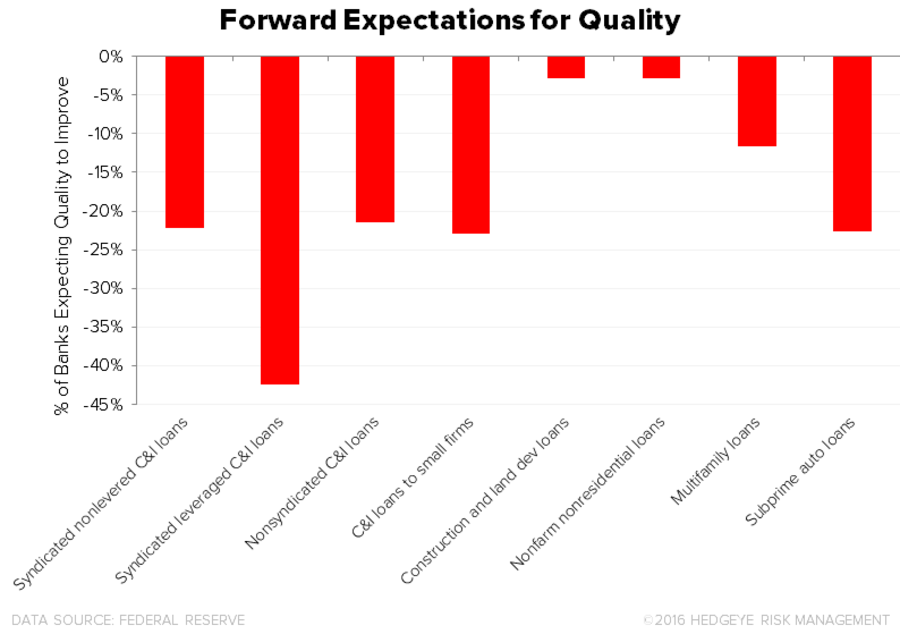

3. Banks expect things to get worse throughout 2016. This quarter's survey included special questions on lenders' forward expectations for standards, spreads, volumes, and quality, and the results are not inspiring. The first chart below shows that banks expect standards to tighten in all commercial and industrial categories in 2016. They also expect to increase spreads across all surveyed loan categories. Also, while banks expect increasing C&I volumes, a significant percentage of banks expect CRE, multifamily, and GSE-eligible residential mortgage volumes to decrease over 2016. Finally, the second chart below shows a sea of red in expectations for credit quality. There is not a single category in which banks expect improvement in credit quality. To put it simply, a net positive percentage of senior loan officers believe that we have reached and moved past the inflection point of deteriorating credit conditions.

Given the increased number of negative responses and the negative forward expectations, we appear to have reached the inflection point signaling that Financial equity prices are past their peak. Unlike the prior positive tick in 1Q12, this time the economic cycle is showing many signs of being late stage, and the survey has deteriorated further quarter over quarter.

The chart below looks at the historical C&I lending standards (LHS) juxtaposed against the S&P 500 Financials Index (RHS). C&I lending standards have historically begun tightening coincident with or ahead of peaks in Financial equity prices. We've highlighted in green the periods during which Financials stocks have risen. In the 1990s it was clear that lending standards were tightening by late 1999, suggesting the roll was near. In the 2003-2007 period standards began to tighten in 2007.

A Quick Review of the Senior Loan Officer Survey by Category:

C&I: The Canary In the Coal Mine

C&I loans continue again signaled the credit cycle peak with standards tightening for two quarters in a row now. The net percentage of banks tightening standards for loans to large firms moved from +7.3% in 4Q15 to 8.3% in 1Q16. Additionally, +4.2% of banks tightened standards for C&I loans to small firms.

CRE: Tightening Across the Board

Banks continued to tightening standards for all three CRE categories in 1Q16. Additionally, the percentage tightening standards for multifamily loans, which had previously swung back and forth from negative (good) to positive (bad), is definitively positive (bad) at +22.6% in 1Q16. This inflection in CRE standards adds to our concern over the inflection in C&I standards.

Meanwhile, demand for all three categories of CRE loans increased, albeit at sequentially lower percentages, in the first quarter.

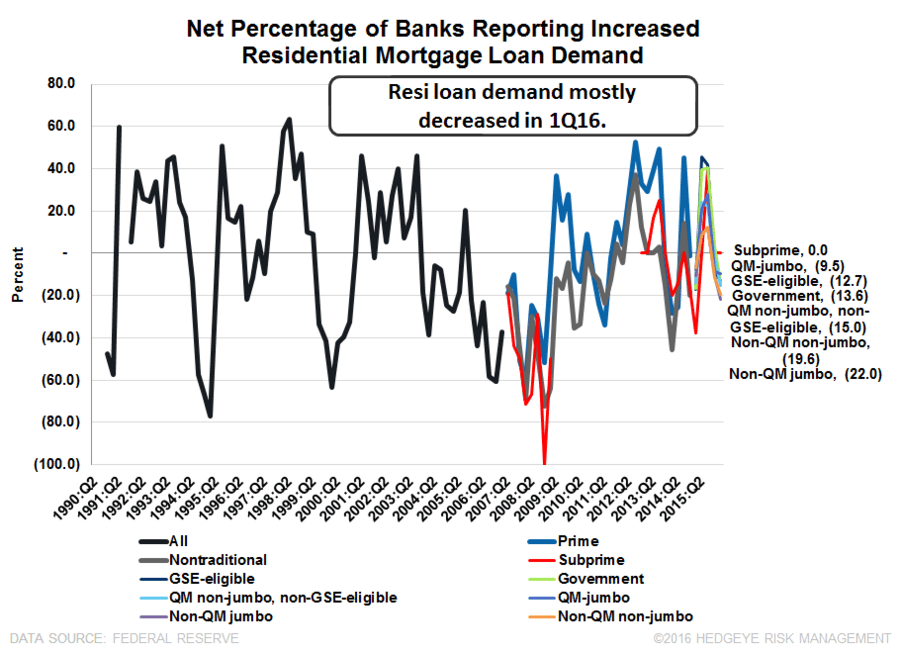

Residential Mortgage: Mixed

Starting in 1Q15, the Federal Reserve broke the survey's residential Prime and Nontraditional categories into six new categories and kept the Subprime category for a total of seven different categories. The six new categories include: (GSE-Eligible, Government, QM non-jumbo/non-GSE eligible, QM jumbo, Non-QM jumbo, and Non-QM/non-jumbo). The categories we're most interested in are the GSE-Eligible (Fannie/Freddie) and Government categories (FHA/VA) since these two categories account for ~90% of all origination volume. The GSE-Eligible category showed 14.3% of banks, net, eased standards Q/Q in 1Q16. Government standards were unchanged. Standards for Subprime auto were also unchanged, an improvement from the 20% tightening in 4Q15. All four other categories eased.

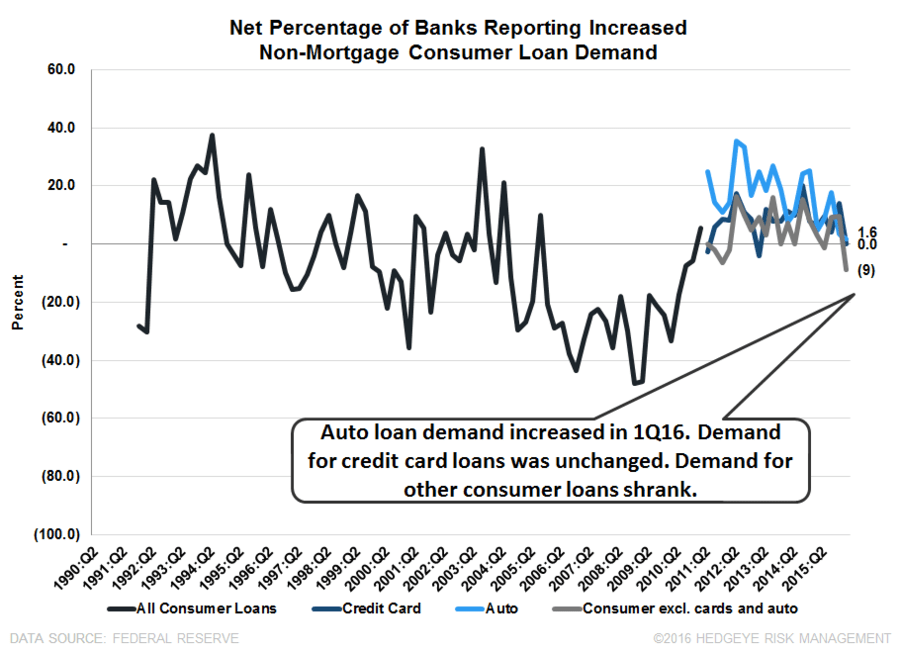

We pay little attention to the demand component of the Fed's Survey because it reflects shifting refi demand and isn't a good barometer for purchase activity. Nevertheless, we include both charts below.

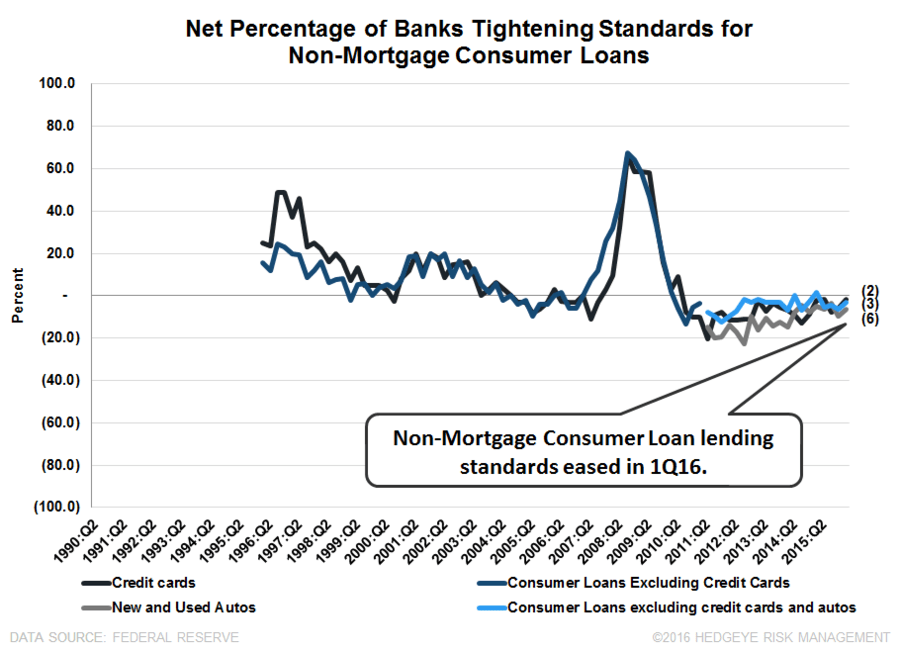

Consumer Loans: Easing

Standards for credit cards, auto loans, and consumer loans ex-cards and autos all eased in the third quarter.