No investable turn yet

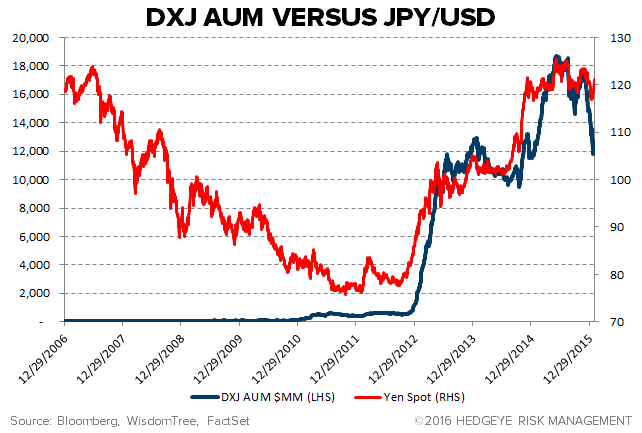

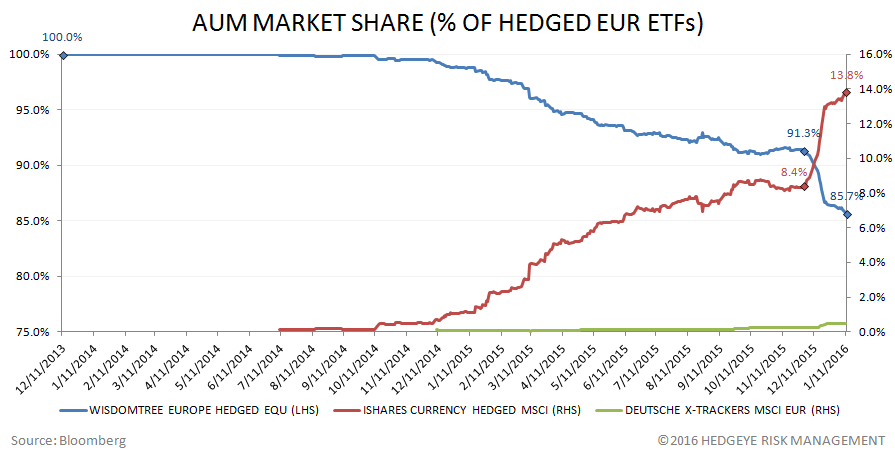

While a single day doesn't make a trend, the Bank of Japan's move to negative overnight lending rates last week was hardly a stop gap in the ongoing slippery slope in fund flows at WisdomTree's Japan Hedged equity fund (DXJ). The +$19 million inflow last Friday into the DXJ following that BoJ announcement failed to markedly improve trends and the WisdomTree product still put in the worst month in its history losing -$967 million in the first month of '16 following the -$887 million outflow in December. Zooming out, these redemptions have resulted in DXJ's AUM falling from a high of $18.7 billion on June 8th, 2015 to $12.7 billion as of last week with competing hedged products continuing to pick up share. The DXJ lost another 2 points of market share through the end of the first month of 2016 with the 87% share from the beginning of December 2015 receding to 85% at the end of January 2016 (with iShares continuing to pick up incremental AUM).

MEANWHILE IN EUROPE...SLIGHTLY BETTER SLEDDING

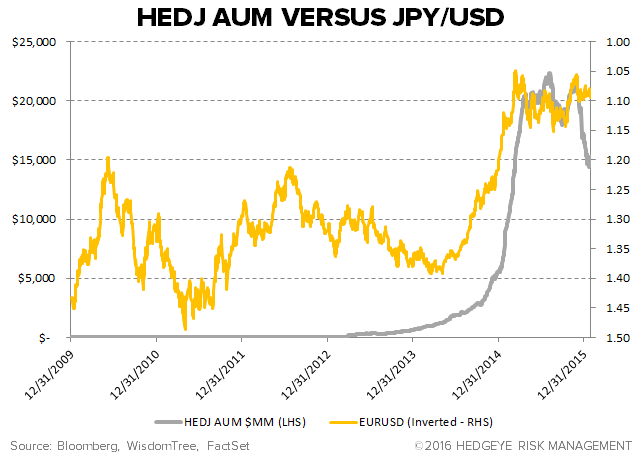

Meanwhile the rate of change in fund flows at WisdomTree's hedged Euro product, the HEDJ, bounced off of December lows. While January still resulted in redemptions of -$814 million following December's 2015 loss of -$1.9 billion, total AUM is still headed in the wrong direction. The past several months have brought HEDJ’s AUM down to $15.3 billion from its August 5, 2015 high of $22.3 billion. Similar to its Japanese counterpart, HEDJ is losing share on the margin to competitors, with iShares and Deutsche Bank now totaling 14% of the market at the end of January 2016.

Less bad for now but we need more evidence

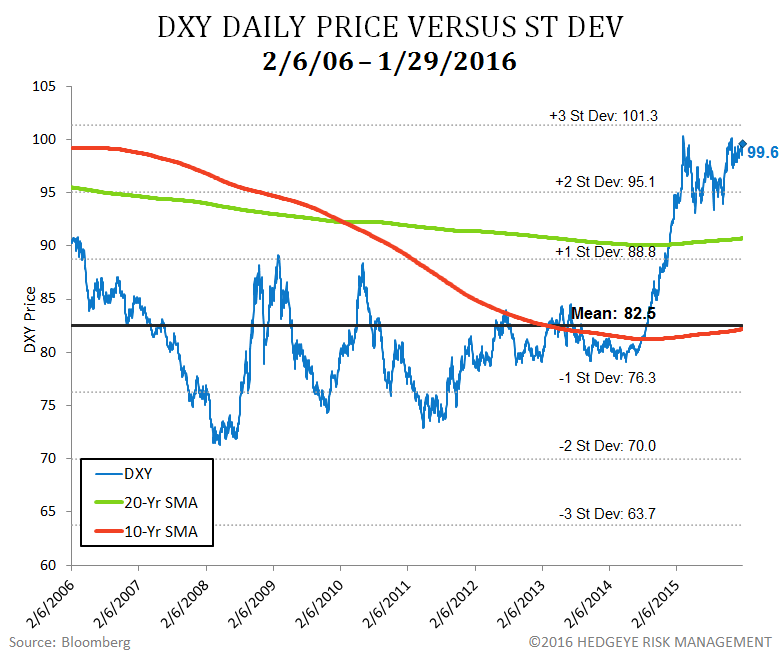

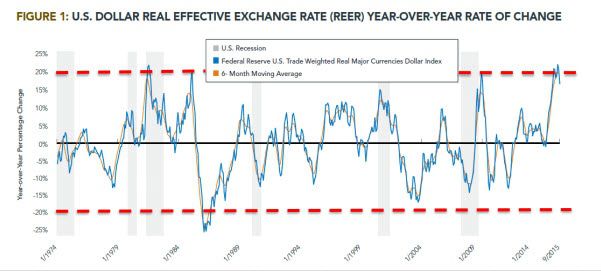

Bigger picture, our research shows that industry hedged equity products are dependent on substantial dollar strength to provide value, and with only a marginal rise year-to-date, the U.S. dollar's ascent is stalling from several perspectives (namely a 3 sigma move on a 10 year timeframe and also at its historical +20% year-over-year real rate of change). In addition, the U.S. dollar in all but one instance has historically declined after initial Fed Fund rate increases (with the sole exception being the move in 1988).

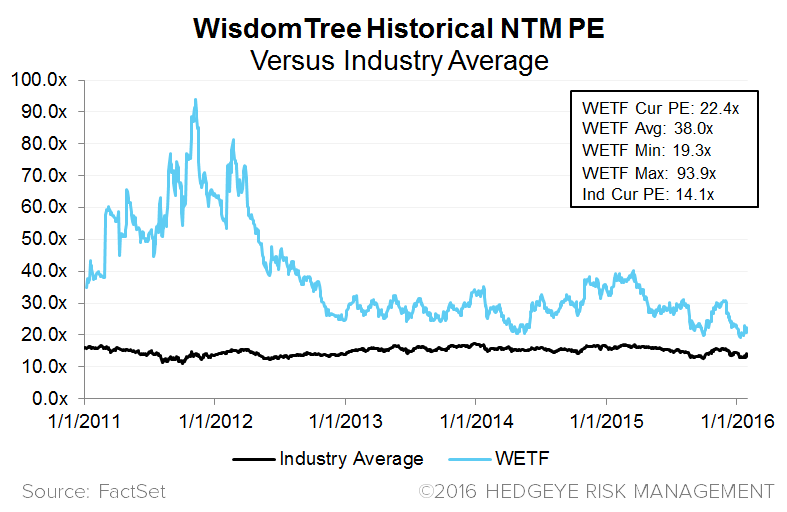

The DXJ and HEDJ outflows contributed to overall firm redemptions of -$1.7 billion in January 2016, off of December lows but a far cry from +$4.0 billion in January last year. While the stock has discounted these current trends having dropped substantially from year-end, shares are far from any relative value yet. WETF still sports a 22.4x forward 12-month multiple on Street estimates of $0.54 per share. The asset management group trades currently at 14.1x '16 numbers which means that either WETF trends have to substantially improve or the stock still has meaningful downside. The stock remains on our Best Ideas list as a Short.

WisdomTree (WETF) - More Questions Than Answers - We Remain Short

WisdomTree (WETF) Black Book Presentation - Not So Smart Beta

Please let us know of questions,

Jonathan Casteleyn, CFA, CMT