Key Takeaway:

Last week was on course to look like the broader YTD trend (ground and pound), at least until Friday. Friday's rally suggests that we may have re-entered the bad news is good news twilight zone, as the zero handle (0.7%) on 4Q US GDP pushed out expectations for further Fed hikes in 2016 while the BOJ's annoncement of NIRP (negative interest rate policy) suggested that global central banks are collectively hitting the gas (or at least not tapping the brakes).

Call us skeptics, but we have zero interest in buying the dip here. Numerous economic indicators are flashing recessionary signals, GDP is trajecting towards zero and the Fed is still debating whether to raise rates.

Our heatmap below is still flashing mostly red across the short and long term while mixed on intermediate-term readings.

We have added the CDOR-OIS spread to the bottom of our monitor. It is the Canadian equivalent of the Euribor-OIS spread and measures the difference between the Canadian interbank lending rate and overnight indexed swaps. In other words, it measures counterparty risk in the Canadian banking system. The measure hitting a post-crisis high of 50 bps on January 15 prompted us to start tracking it. The spread has since tightened somewhat but rose week over week to 40 bps from 38 bps.

Current Ideas:

Financial Risk Monitor Summary

• Short-term(WoW): Negative / 2 of 13 improved / 4 out of 13 worsened / 7 of 13 unchanged

• Intermediate-term(WoW): Negative / 5 of 13 improved / 5 out of 13 worsened / 3 of 13 unchanged

• Long-term(WoW): Negative / 1 of 13 improved / 4 out of 13 worsened / 8 of 13 unchanged

1. U.S. Financial CDS – Swaps tightened for 10 out of 27 domestic financial institutions. With 4Q15 U.S. GDP coming in lower than expectations at 0.7%, the median financial swap widened from 75 to 77. At the bottom of our U.S. CDS table below, we have added indices on investment grade and high yield CDS, which tightened last week by -2 bps to 102 and by -17 bps to 508, respectively.

Tightened the most WoW: GS, WFC, MS

Widened the most WoW: BAC, MMC, AIG

Widened the least/ tightened the most WoW: CB, AON, GNW

Widened the most MoM: AIG, AXP, BAC

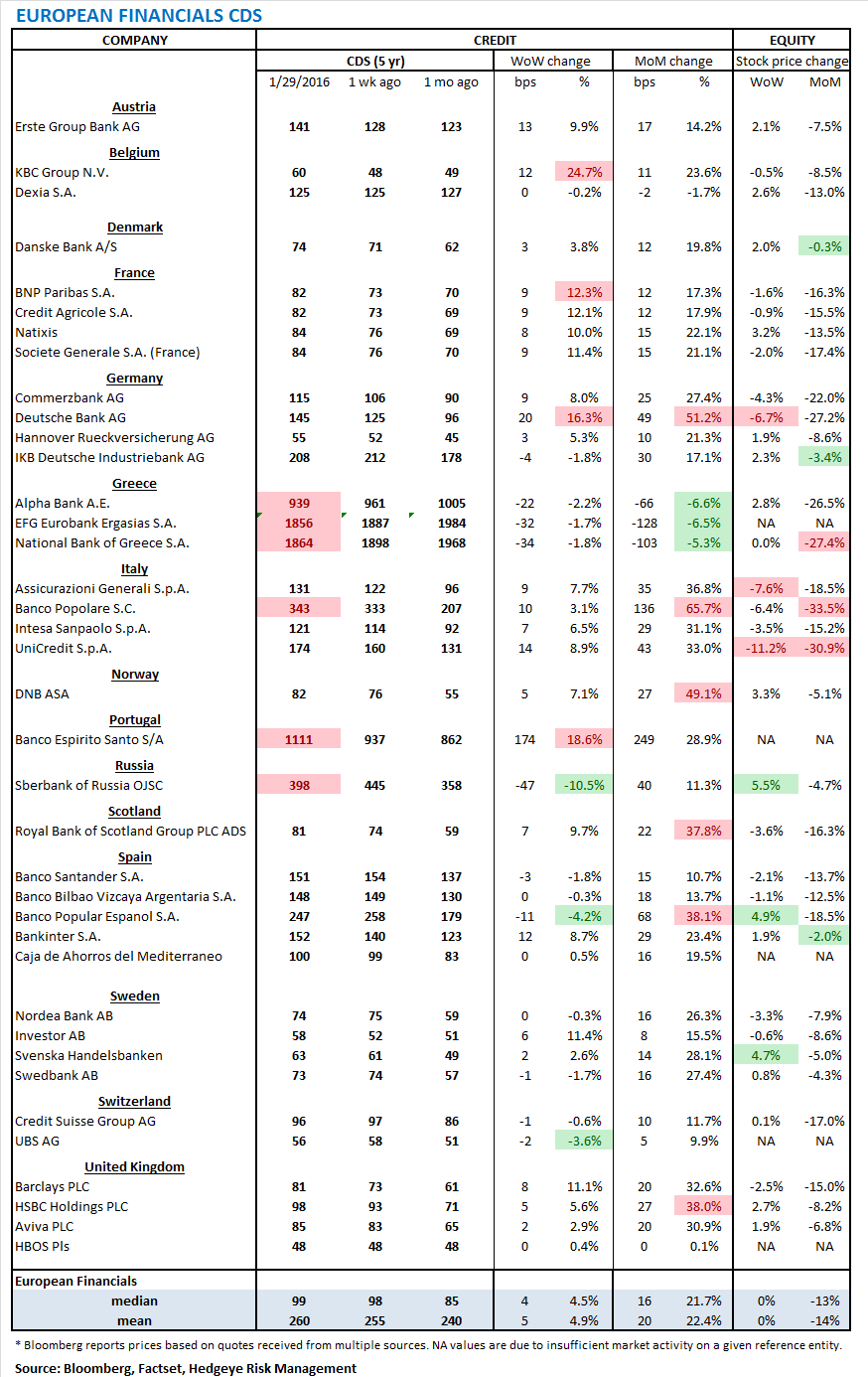

2. European Financial CDS – Swaps mostly widened in Europe last week. Portugal's Banco Espirito Santo was an outlier with CDS widening by 174 bps to 1111. Meanwhile Russia's Sberbank CDS tightened by -47 bps to 398 as oil prices rose.

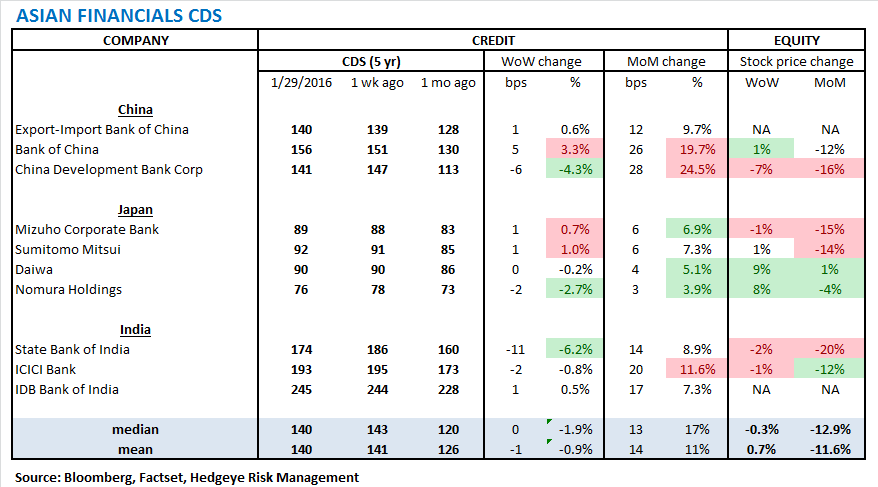

3. Asian Financial CDS – Swaps were mixed among Asian financials last week. The State Bank of India's CDS stood out with a -11 bps tightening to 174.

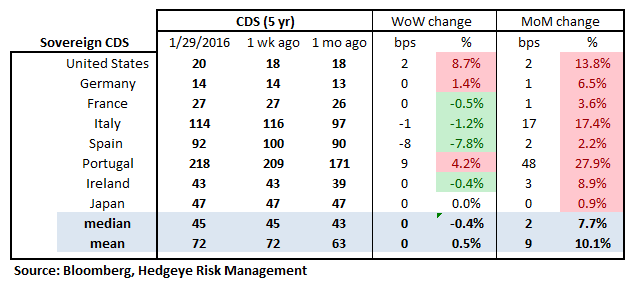

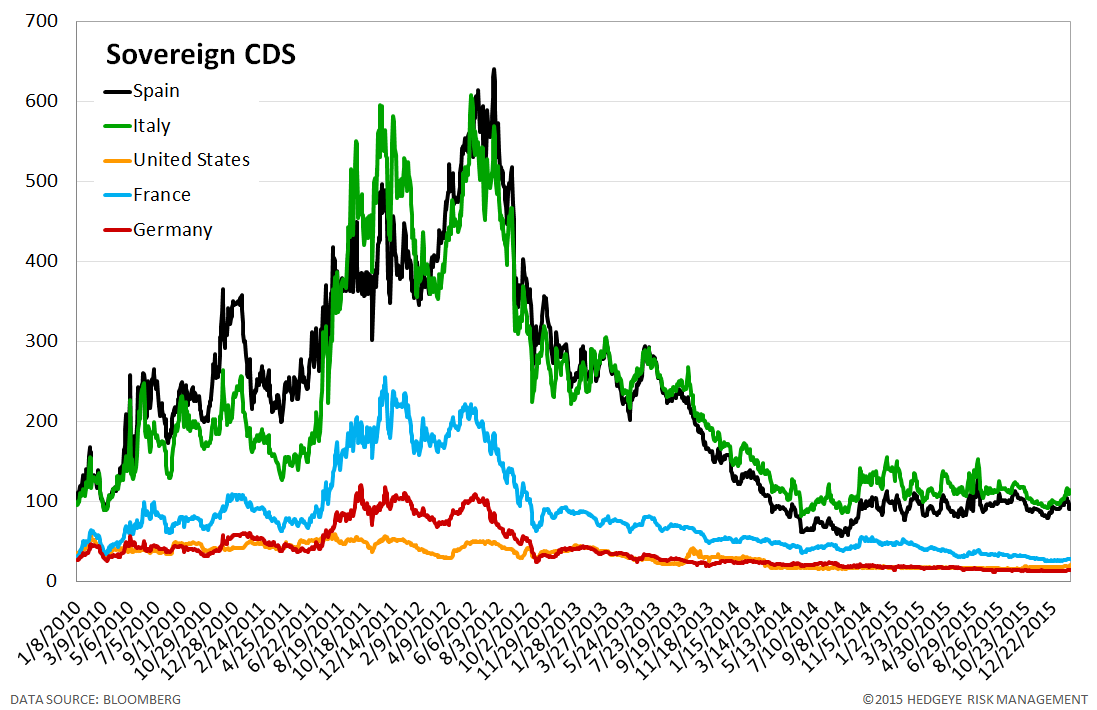

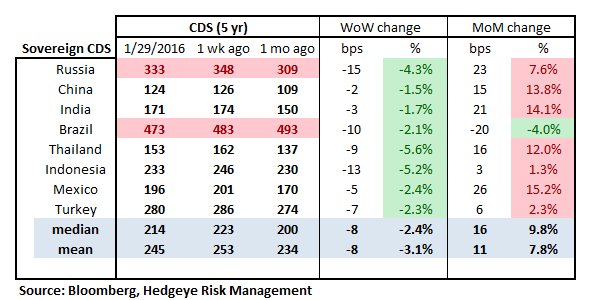

4. Sovereign CDS – Sovereign swaps were mixed last week. Spanish sovereign swaps stood out, tightening by -8 bps to 92.

5. Emerging Market Sovereign CDS – Commodity dependent emerging markets saw swaps tighten with oil and commodity prices rising over last week. Given the rise in oil, Russian swaps tightened the most, by -15 bps to 333.

6. High Yield (YTM) Monitor – High Yield rates fell 25 bps last week, ending the week at 8.73% versus 8.98% the prior week.

7. Leveraged Loan Index Monitor – The Leveraged Loan Index rose 3.0 points last week, ending at 1796.

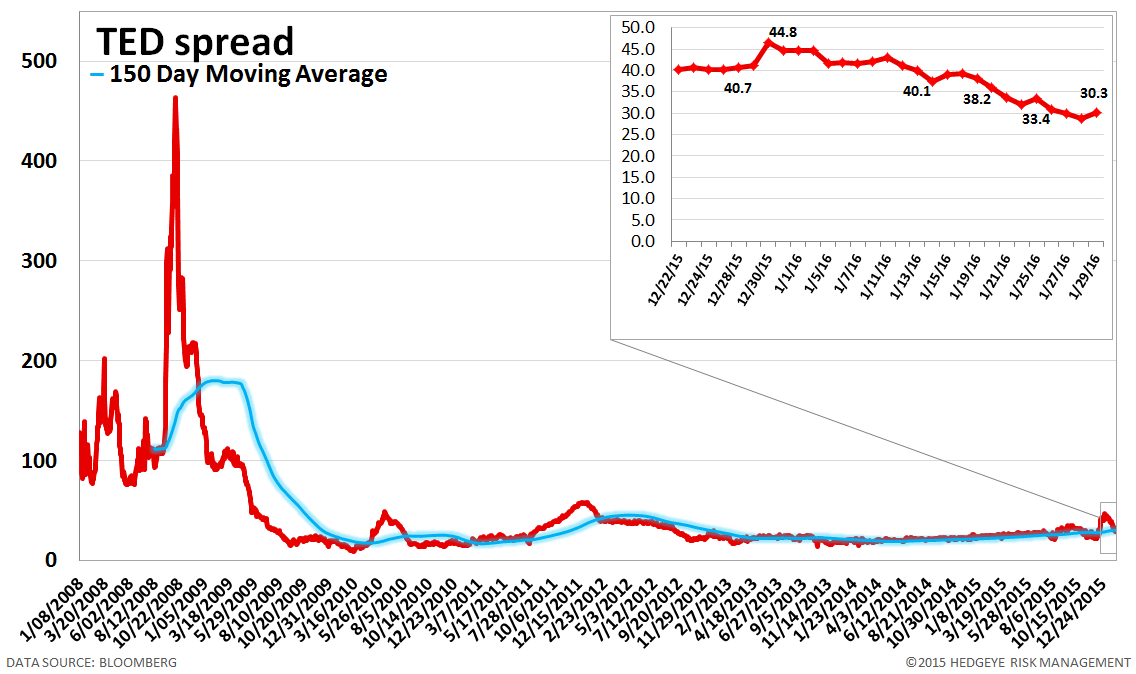

8. TED Spread Monitor – The TED spread fell 2 basis points last week, ending the week at 30 bps this week versus last week’s print of 32 bps.

9. CRB Commodity Price Index – The CRB index rose 6.7%, ending the week at 167 versus 156 the prior week. As compared with the prior month, commodity prices have decreased -5.4%. We generally regard changes in commodity prices on the margin as having meaningful consumption implications.

10. Euribor-OIS Spread – The Euribor-OIS spread (the difference between the euro interbank lending rate and overnight indexed swaps) measures bank counterparty risk in the Eurozone. The OIS is analogous to the effective Fed Funds rate in the United States. Banks lending at the OIS do not swap principal, so counterparty risk in the OIS is minimal. By contrast, the Euribor rate is the rate offered for unsecured interbank lending. Thus, the spread between the two isolates counterparty risk. The Euribor-OIS spread widened by 1 bps to 14 bps.

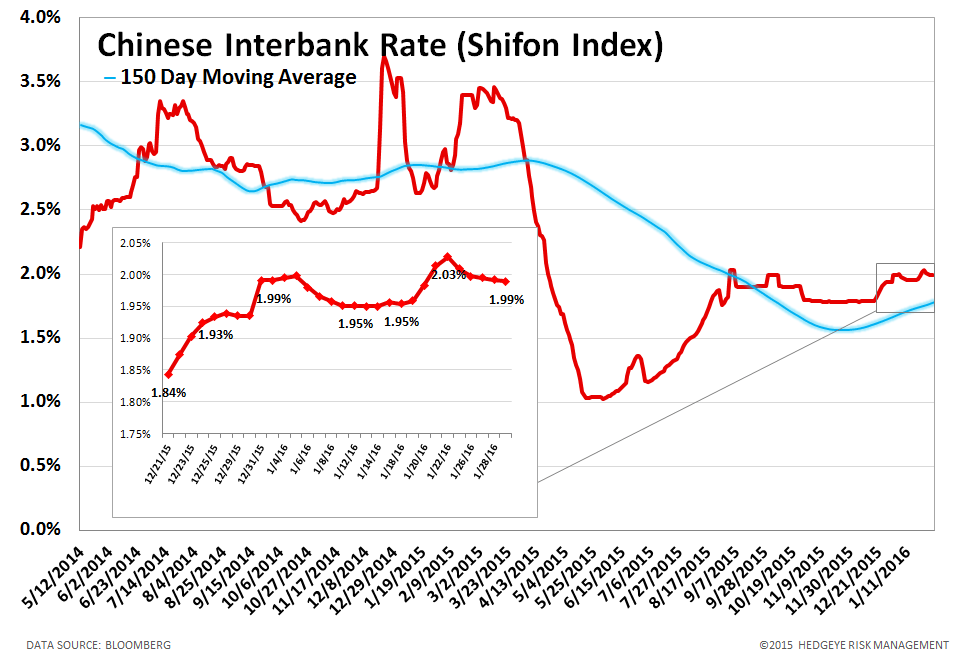

11. Chinese Interbank Rate (Shifon Index) – The Shifon Index fell 4 basis points last week, ending the week at 1.99% versus last week’s print of 2.03%. The Shifon Index measures banks’ overnight lending rates to one another, a gauge of systemic stress in the Chinese banking system.

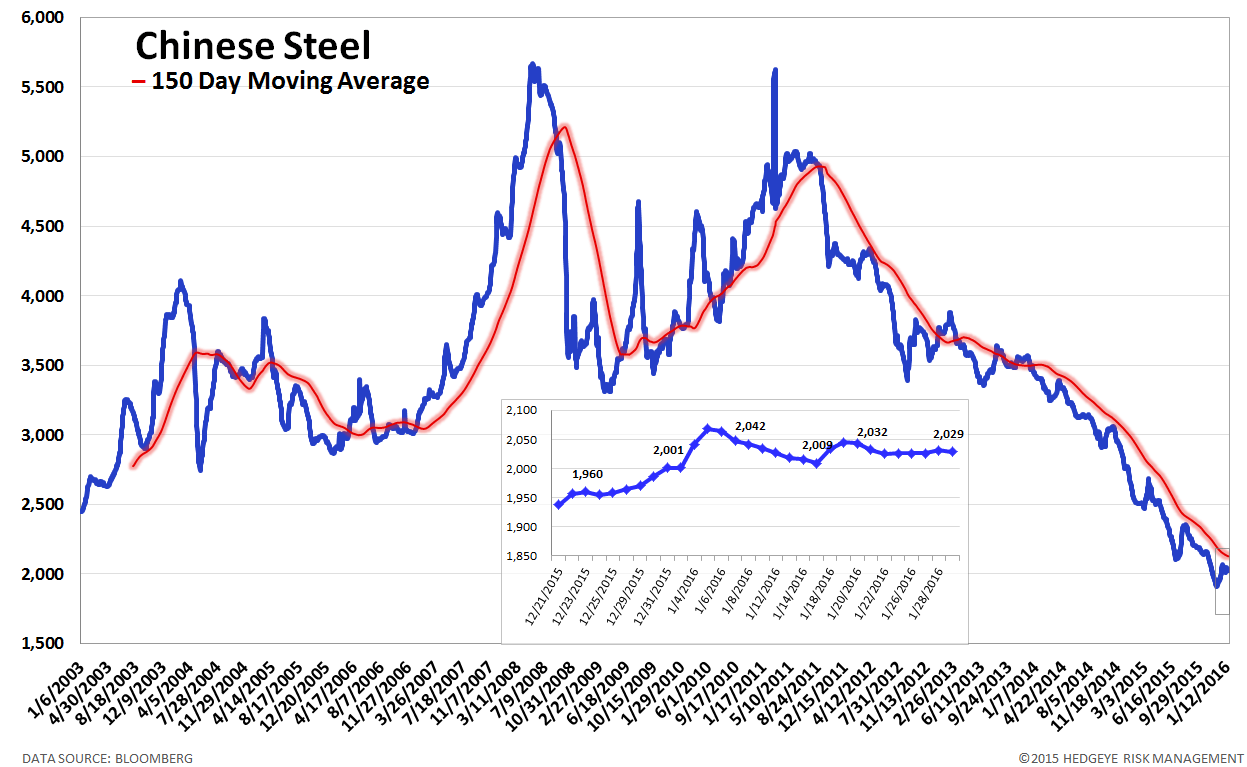

12. Chinese Steel – Steel prices in China rose 0.2% last week, or 4 yuan/ton, to 2029 yuan/ton. We use Chinese steel rebar prices to gauge Chinese construction activity and, by extension, the health of the Chinese economy.

13. 2-10 Spread – Last week the 2-10 spread tightened to 115 bps, -4 bps tighter than a week ago. We track the 2-10 spread as an indicator of bank margin pressure.

14. CDOR-OIS Spread – The CDOR-OIS spread is the Canadian equivalent of the Euribor-OIS spread. It is the difference between the Canadian interbank lending rate and overnight indexed swaps, and it measures bank counterparty risk in Canada. The CDOR-OIS spread widened by 2 bps to 40 bps.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT