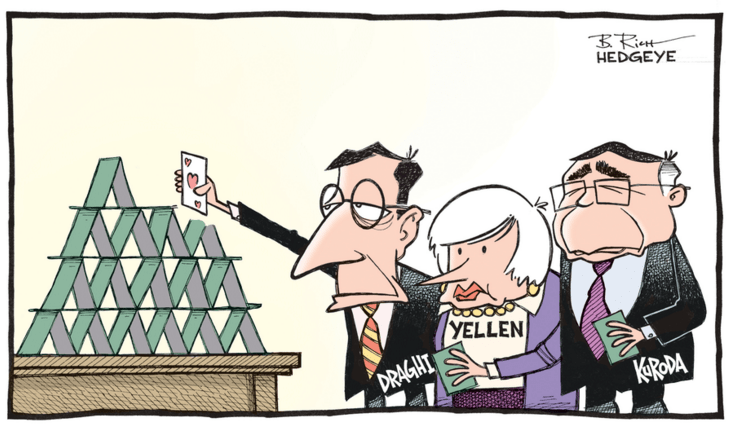

Do central planners worldwide have any credibility anymore?

This past Wednesday's Fed's FOMC announcement amounted to little more than a shoulder shrug. Apparently, the members will be...

"... monitoring global economic and financial developments and is assessing their implications for the labor market and inflation, and for the balance of risks to the outlook."

Thanks for coming out.

To be clear, today's U.S. GDP report was unequivocally awful. We're holding our breath in anticipation wondering what Yellen & Co. will have to say about it. Unfortunately, we'll likely have to wait until at least February 10th when Yellen testifies on Capitol Hill.

Meanwhile... outside these fifty states, central planners abroad are doing their best to screw things up too. Here's analysis from our Macro team on Japan in a note sent to subscribers this morning on the BOJ's decision to pursue a negative interest rate policy.

"News of the morning = Japan goes NIRP – and the Yen goes >120, 10Y JGB’s trade down to 0.09% (as in “nine” basis points) and along with the balance of global yields, U.S. 10Y treasury yields followed suite and are trading down -6bps to 1.91% as the yield curve (10’s-2’s) compresses to another new low.

Together with yesterday’s durable goods disaster, this morning’s slowing GDP report and more rumors of stimulus out of China the global #GrowthSlowing data remains conspicuous. Resurgent central bank interventionism is not a function of improving macro fundamentals. "

Heading over to Europe...

"The ECB’s Jens Weidmann (also President of the Bundesbank) warned fellow policy makers that the ECB should not go too far with the QE program, but will President Mario Draghi listen? We doubt it! Weidmann rightly points out that the ECB needs to lower its inflation forecast for 2016. A 2% target is after all a pipedream!"

Watch Hedgeye CEO Keith McCullough discuss central banking in the video below.

... So back to our original question, "Do central planners have any credibility?"