Below are our analysts’ new updates on our fourteen current high conviction long and short ideas. Hedgeye CEO Keith McCullough’s updated levels for each ticker are below.

LEVELS

Trade :: Trend :: Tail Process - These are three durations over which we analyze investment ideas and themes. Hedgeye has created a process as a way of characterizing our investment ideas and their risk profiles, to fit the investing strategies and preferences of our subscribers.

- "Trade" is a duration of 3 weeks or less

- "Trend" is a duration of 3 months or more

- "Tail" is a duration of 3 years or less

IDEAS UPDATES

TLT | XLU | JNK

To view our analyst's original report on Junk Bonds click here and here for Utilities.

After a busy week of domestic data, you probably don’t need us to tell you that growth continues to slow. Despite the short-covering squeeze in energy stocks, Utilities (XLU) closed out January as the only sector in positive territory (+5%), other than Consumer Staples which eked out a +0.5% gain. It was an awful start to the year for the S&P 500 (-5%).

Don’t expect +10% of relative outperformance every month, but if you stuck with us on this trade, you’re in much better shape than most. Below is both absolute and relative sector performance for the S&P 500 for January:

Looking at our pair trade in credit markets, Long-Term Treasuries (TLT) continues to preserve capital against the slow-moving trainwreck in Junk Bonds (JNK). Week-over-week, 10-year bond yields crashed 13bps to 1.92%. That helped lift the best play on U.S. growth slowing (TLT) by 0.85% on the week as credit spreads continued to widen (JNK gained +0.76% on the week, underperforming TLT marginally on a relative basis).

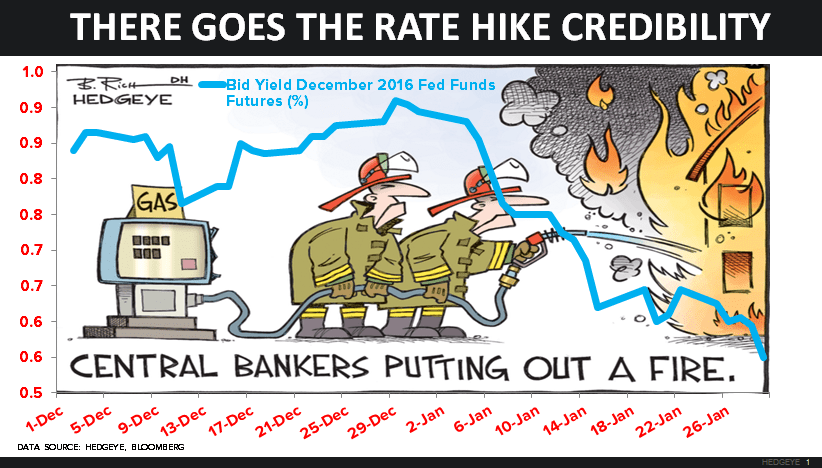

Meanwhile... the market didn’t believe the FOMC's steadfast forecast on Wednesday that there will be four rate hikes in 2016. The “0” in front of Q4 GDP confirmed that all is NOT well. The bid-yield of December 2016 Federal Funds Futures (rate hike expectations) agrees with our #GrowthSlowing call.

As the chart below shows, the market questions the credibility of the December rate hike, with December 2016 Fed funds futures crashing to new lows on Friday’s GDP report. Clearly, investors don't believe the economy is in any shape for tighter policy.

Getting past Old Wall storytelling, let's look at the increasingly deteriorating data. Here’s how things shook out through the end of this week:

- GDP: Q4 2015 GDP printed +0.7% taking the full year number to just over +2%. Ouch. (Note: Our full-year 2016 expectation for GDP is 1.5%. You know what that means... #GrowthSlowing)

- Durable Goods: Printed -5.1% M/M and -0.6% Y/Y for December) -- All the sub-aggregates that make up the number declined both sequentially and Y/Y. #IndustrialRecession

- Capital Expenditures (Capex): 11th consecutive month of negative Y/Y growth and worst number since 2009

- Capex Plans: Forward Capex plans as measured by the Fed Regional Surveys made another new low in January suggesting the negative trend in investment spending will continue

- Earnings Recession: Earnings growth and corporate profits across S&P500 companies have been negative Y/Y for two consecutive quarters as of 3Q15 and are tracking down 4.5% with ~40% of S&P 500 constituents having reported for 4Q15

MDRX

To view our analyst's original report on Allscripts Healthcare Solutions click here.

All evidence suggests that attrition continues to be an underappreciated risk by Allscripts Healthcare Solutions (MDRX) investors. The latest data point came from MidMichigan Health, who announced earlier this week that they signed a $55 million contract with Epic for a system-wide, integrated EHR. The expected go-live date is April 2017.

MidMichigan is affiliated with the University of Michigan Health System (Epic Shop), and operates 4 hospitals with approximately 500 providers. MidMichigan currently uses Cerner in the hospitals and Allscripts Touchworks in the medical practices (approximately 200 employed physicians).

Allscripts also had an arrangement whereby MidMichigan would subsidize the cost of the EHR to affiliated, independent physicians with referring privileges to the hospital. As a result, the loss likely extends beyond that of the employed physicians and is consistent with our 'reverse network effect' view.

NUS

To view our analyst's original report on Nu Skin click here.

NUS IS A BROKEN BUSINESS MODEL

Nu Skin (NUS) is down roughly -16.5% YTD, leaving people asking how much lower can it go? We think the name has significant downside from here.

Some of the bear case is dependent on government action and predicated on the allegation that they are deceiving consumers and performing fraudulent acts.

However, even if you're willing to take the other side of that trade and say they are completely ethical and not doing anything illegal, their business is still in a secular decline, boasting minuscule market share in the category.

Other issues? The implications of slowing distributor growth will be a serious problem for them, and attempting to sell high-end, over-priced products in the cold calling, direct selling environment will prove fruitless in the long run.

Bottom line: Even after the recent selloff, we see an additional 30-50% of downside.

FII

To view our analyst's original report on Federated Investors click here.

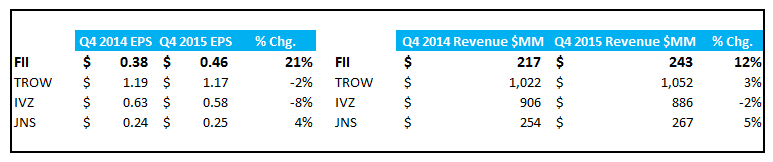

The deluge of asset management earnings that hit during the week is always an exercise of parsing words and figuring out the many machinations affecting the industry. The basic premise of the sector’s results however were quite clear and, as a result, Federated Investors (FII) is starting to outperform.

Money market fund balances are starting to improve as investors rush back into cash. Also, on the recent Fed rate hike, there was marginal improvement in the profitability of money funds.

FII on both a top line revenue and bottom line earnings perspective handily trounced the rest of the group with +21% year-over-year earnings growth on +12% top line revenue growth. FII will continue this outperformance into the 1H of 2016.

WAB

To view our analyst's original report on Wabtec click here.

With speeds picking back up, we expect that equipment to be pushed back out. More speed results in less equipment in service. If speeds continue higher, freight railroads may find themselves with ample excess equipment and reduced aftermarket needs amid slow volume growth – a negative combination for Wabtec (WAB).

We believe freight rail equipment spending is just starting to enter a multi-year downturn. It’s a cyclical market, and WAB shares remain priced for growth. As for WAB and any cyclical company, peak margins aren’t a great sign for longs.

TIF

To view our analyst's original report on Tiffany click here.

Late last week Tiffany's (TIF) board approved an expanded share repurchase program. We're not concerned about being short TIF into the company re-upping its share repo authorization. Here's why:

- We're only talking about $500mm, which is about 6% of the current market cap. This program is a drop in the bucket.

- Next, just because a company announces a repo does not mean it will actually execute on it.

- Lastly and most importantly, history does not lie. Over the past decade, TIF spent $1.1bn on share repo, and yet the share count only came down by 6.6mm, or 4.8%. The implied repo price per share comes out to $170, and yet the stock only poked its head above $100 fewer than a dozen times, and never broke $110. But the average implied repo price was $170?

The fact is that some companies, like GPS (which we also don't like) use repurchases as an offensive weapon – cutting its share count in half over a decade. TIF is not one of those companies – as it basically uses the repo program as a way to offset dilution from options and other non-cash compensation.

W

To view our analyst's original report on Wayfair click here.

This week Wayfair (W) put out a press release regarding a new search engine platform it is implementing in Europe. The company continues to invest in infrastructure both domestically and abroad, while the business model has yet to prove it can be profitable at scale.

We think the company is massively overestimating its addressable market when it notes a $90bn and 60mm household opportunity in the United States. Our math suggests a number less than a third of that. We suspect management is overestimating the international opportunity as well.

RH

To view our analyst's original report on Restoration Hardware click here.

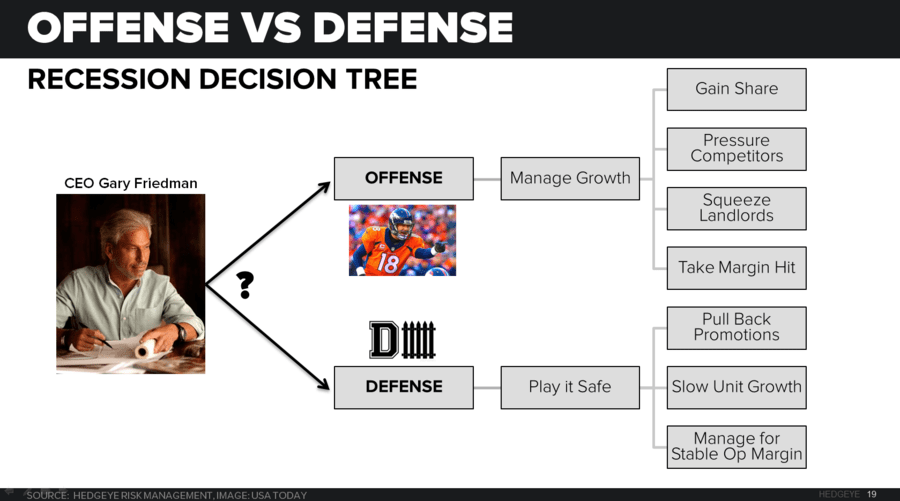

Here are the key takeaways from a call our Retail team hosted this Wednesday titled: RH | In a Recession…

Restoration Hardware (RH) will absolutely play offense:

Recession or not, we think management will run the company like it’s in one. That means RH is likely to be more aggressive on price to gain share. RH does not like playing defense, and we think it’s comfortable taking an offensive margin hit to gain share. That said, it has some defendable financial levers that were 100% absent in past downturns. We think the limited earnings downside in a recession will surprise most people.

LT Risk reward skewed grossly to the upside:

Even in a Great Recession 2.0, RH is likely to grow revenue by 5-10%, which is huge given the rest of the category would be down 20-30%. That bifurcation is likely not recognized by the market. Realistically, in a ‘normal’ recession (whatever that is) revenue is up double digits, and earnings temporarily bottom out at $2.65. Could we see 18x that number? That’s $48, or $13 down. Upside in a year in a normal economy is about $120 – or roughly 2x today’s price.

MCD

To view our analyst's original report on McDonald's click here.

If you weren’t yet convinced that Steve Easterbrook is leading the turnaround of the McDonald’s business, it is time to start believing. Since Steve stepped into his current role as CEO 12 months ago, McDonald's (MCD) has orchestrated an historic turnaround of their global business. The success they are now seeing is built up by dozens of relatively minor improvements across the system, as well as bigger initiatives that changed MCD’s offerings and the way they conduct their business.

Coming out of this quarter we are very encouraged by the progress they are making across all markets, most notably in the United States. In 4Q15 the U.S. segment comp store sales increased +5.7% versus consensus estimates of +2.7%, a 300 bps beat. These results were primarily driven by strong consumer demand for All Day Breakfast and mild weather compared to last year. These factors brought in traffic, while the changes MCD made to its restaurants (improved food and better customer experience) will keep these customers coming back.

The job is not done yet, and Steve was quick to share this same sentiment.

“While we are pleased with the recent positive momentum in the U.S., it will take at least six more months of positive comparable sales and guest count growth to progress through sustained and prolonged growth phases of our turnaround.”

We have seen two quarters of strong growth, but the team at MCD must continue to stay focused on further refinements and innovation to propel continued growth for the future.

Looking out into 2016, MCD has strong tailwinds; three more quarters before they lap the All Day Breakfast launch in the U.S., a full year of McPick 2, their mobile app is gaining steam, and they continue to improve their domestic system, with goals to perform 400 to 500 reimages in 2016 (about half of the system is modernized in the U.S. currently, MCD has set a global goal of having 90% of restaurants modernized by the end of 2018). For all these reasons and more, MCD continues to be our top LONG idea in the restaurant space.

In closing Steve provided positive commentary for the outlook of 2016:

“I am confident in our ability to sustain our positive momentum as we continue to execute our turnaround plans into 2016. And I’m excited about our longer-term opportunities to strengthen our business and reassert McDonald’s as the global leader we know we are.”

FL

To view our analyst's original report on Foot Locker click here.

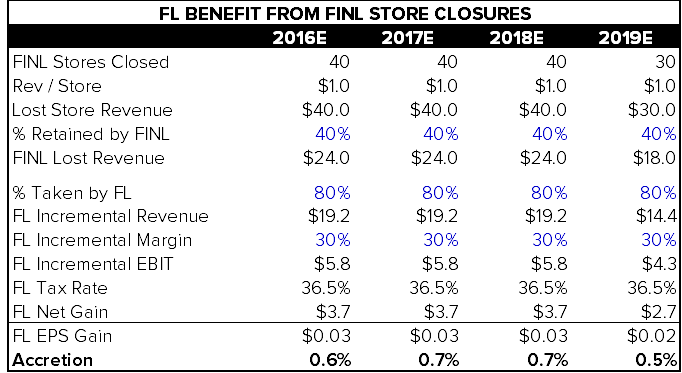

Earlier this month The Finish Line (FINL) announced that it would be closing 25% of its existing fleet over a 4 year time period. That’s gross closures, as the company will be working on the quality of its real estate portfolio to increase its penetration in better quality malls, i.e. more overlap with Foot Locker (FL) in better markets.

What we know – each of the 150 stores earmarked for closure are doing about 1mm bucks per store, about 50% below the company average of $2mm. 65% of those sales are attributed to FINL loyalty members.

If we look at the store footprint overlap by mall between Foot Locker (banner) and Finish Line it’s only 67% (chart below). And our sense is, there is more overlap on the top end of the spectrum compared to the bottom end where FINL will be closing locations. That’s because FL has been extremely prudent over the past 5 years as it stripped capital out of the model by rationalizing its store footprint.

All in we get to a $0.03 benefit to FL’s bottom line, and $20mm to the top line per year through FY19 from the door closures assuming a high overlap ratio between the store locations. That's less than 1% accretion per year. To get there we assume that FINL recaptures 40% of the lost sales, and 80% of the forfeited share shifts over to FL. We assume a 30% margin for dollars transferred, as FL won’t have to spend up dramatically to win that money.

Worst case, assuming FINL recaptures 0% of the dollars lost, and FL gets 100% (ain’t going to happen as NKE pushes its direct-to-consumer agenda), we could see a $40mm benefit to the top line and $0.06 on the bottom about 1.5% of earnings growth.

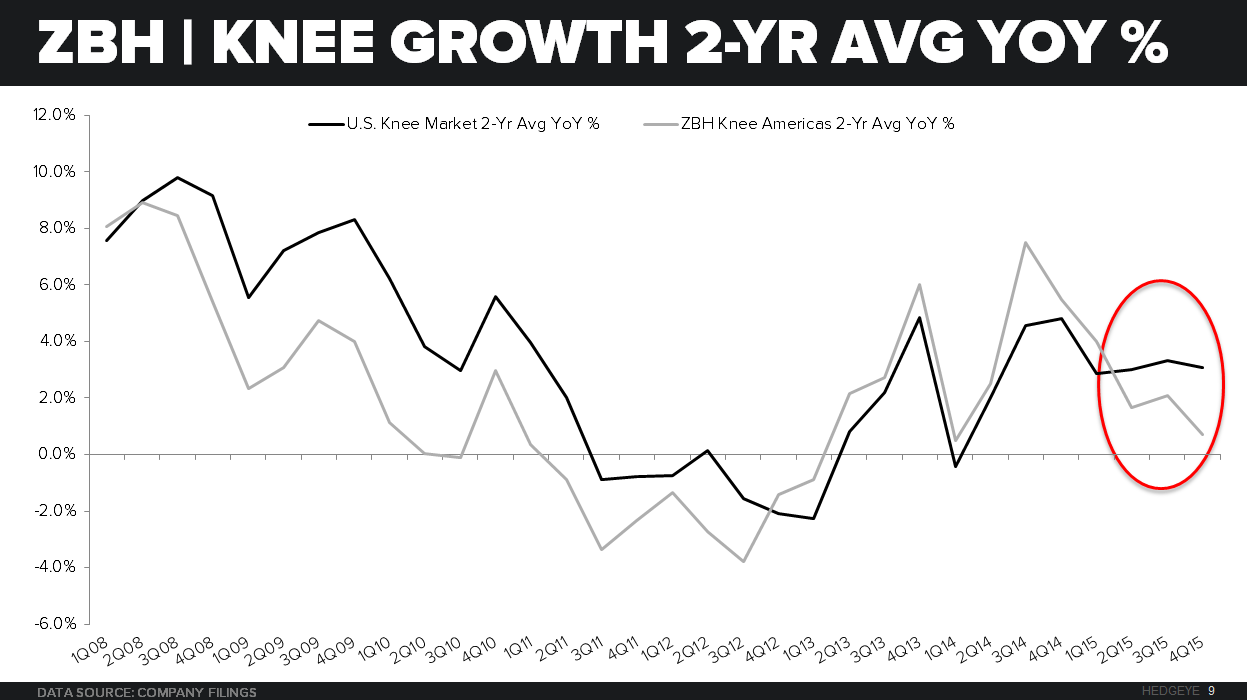

ZBH

To view our analyst's original report on Zimmer Biomet click here.

Pricing may be getting less worse on a reported basis, but share loss, Medicare mix, and a slowing market continue to be bigger and largely unanticipated risks going forward. Zimmer Biomet's (ZBH) Q415 earnings release and call revealed as much.

The market (and us) were looking for a better result on the topline, but it appears demand slowed modestly in the fourth quarter overall, while both SYK and JNJ outperformed ZBH. ZBH cited dealer issues in Europe as well as southern European and Emerging Market growth problems, the latter echoed by other med tech earnings releases, both of which will take some time to resolve.

The next couple of weeks will be informative as we get both Healthcare employment and job openings in Healthcare from the BLS. Today CMS updated Medicaid enrollment through November.

Altogether we will have a complete update for our #ACATaper theme which has so far slowly been panning out, but that we expect to accelerate to the downside in the next 2 months, and bring with it some additional pressure on ZBH’s already modest topline expectations.

Click here to watch a video of our Healthcare team's latest updates on Hospital Corporation of America (HCA), Hologic (HOLX) and Zimmer-Biomet (ZBH).

GIS

General Mills (GIS) remains one of our top Long ideas in the consumer staples space. As we have continued to say it boasts style factors that are ideal in turbulent times; high market cap, low beta and liquidity.

Recently, General Mills has been attacked by Chobani commercials, claiming that Yoplait yogurt contains the same ingredients used in pesticide. GIS filed a false advertising lawsuit against Chobani demanding that they stop showing that commercial because it could be detrimental to sales. GIS just got word that a federal judge has barred Chobani from continuing the ad campaign.

This is a win for GIS, but it is unclear right now if there was any damage done to the brand. At this time we do not believe it had any serious impact on the company. We will keep you informed of any material information regarding this lawsuit as it moves forward.