We're not psychologists here at Hedgeye. But one thing seems increasingly clear to us following yesterday's FOMC statement. It appears the Fed is grieving the loss of economic momentum, but denying the reality of unfolding economic data.

The likelihood is rising that we enter a full-blown recession in Q2 or Q3 of this year. That's been our Macro call and we're sticking with it.

Back to Kübler-Ross...

First, the Fed will be forced to reconcile that everything they have predicted in the past year is wrong. It's a tough pill to swallow. As Hedgeye CEO Keith McCullough writes in today's Early Look:

"... the Reputational Bubble that is popping is that of an un-elected and un-accountable bureaucracy called The Federal Reserve. Until Bernanke’s legacy of linear forecasters embrace the non-linearity of it all, one of the most obvious risks remains their forecast."

It will take some time for the Fed to accept economic reality. But they'll eventually have to. We've got the charts below to help nudge them along the road to Acceptance.

Five economic data series that are already in #Recession:

1. industrial production

Following the industrial production print a few weeks ago, McCullough wrote: "Industrial Production down -1.8% y/y accelerating to downside and 1st negative prints since 2009."

2. exports

The latest exports reading was the worst since November 2009...

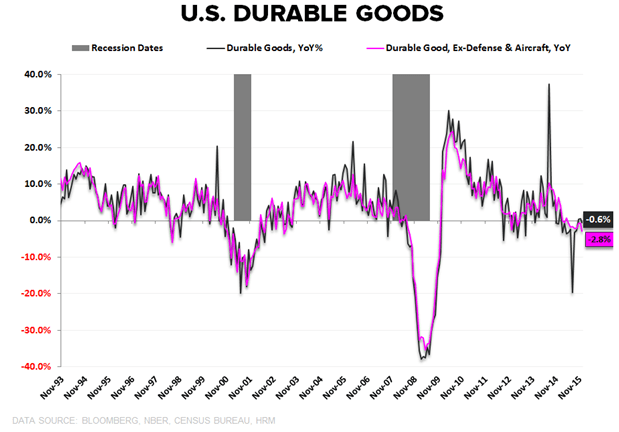

3. Durable goods

"Durable Goods Slowing like this = one of the many predictors of recession risk rising (grey bar coming)," McCullough wrote earlier today.

4. Capex

"Please ignore all red dots and grey (recession) bars," McCullough wrote today.

5. producer prices

Analysis from a recent Investing Ideas newsletter:

"More on the depressed state of the producer. Deflationary PPI continued its march downhill with December reported numbers:

- Headline PPI declined -1.0% Y/Y

- PPI Final Demand declined -3.9% Y/Y

- PPI Final Demand Services increased +0.4% Y/Y

- PPI Energy declined -3.4% Y/Y"

Do you still agree with the Fed's economic forecast?

We don't.